The Fed, Economy, And Markets: Which Is The Horse And Which Is The Cart?

by: Gene Balas, CFA

.

Summary

- Markets have tumbled recently as Fed Chair Janet Yellen has discussed cautious outlook, citing risks to the economy from financial market conditions, yet still sees gradual pace of rate hikes.

- In the past, Fed actions often dictated market reactions. Now, the Fed is watching market conditions, which have begun to influence Fed policy.

- Financial market conditions - including a rising dollar, flattening yield curve, plunging stock market, and rising yield spreads - also influence the economy.

- In the past, Fed actions often dictated market reactions. Now, the Fed is watching market conditions, which have begun to influence Fed policy.

- Financial market conditions - including a rising dollar, flattening yield curve, plunging stock market, and rising yield spreads - also influence the economy.

For many decades, the old adage on Wall Street was "Don't fight the Fed." Certainly, I remember that familiar refrain since I began in the industry in the 1980s. And for the most part, the markets have been driven by the Fed's actions and words. Now, however, Fed Chair Janet Yellen has introduced language in her semi-annual congressional testimony suggesting that, in fact, market conditions may influence Fed policy, a bit of reversal from the usual cause-and-effect. The transmission mechanism is through the effects of financial conditions on the economy. With the market's volatility continuing (at the time of writing, it's February 11), it is a timely topic.

The Views of the Fed

In her speech before Congress February 10 and 11, Yellen observed:

Financial conditions in the United States have recently become less supportive of growth, with declines in broad measures of equity prices, higher borrowing rates for riskier borrowers, and a further appreciation of the dollar. These developments, if they prove persistent, could weigh on the outlook for economic activity and the labor market, although declines in longer-term interest rates and oil prices provide some offset.

On balance, her testimony was cautious, perhaps even a bit downbeat, especially when one considers just how much of her speech was dominated by concerns about risks. In the segment about current conditions and the outlook, Yellen devoted at least 300 words to discussing risks and softer economic growth, while her positive views consisted of simply stating,

Of course, economic growth could also exceed our projections for a number of reasons, including the possibility that low oil prices will boost U.S. economic growth more than we expect.

Financial Conditions

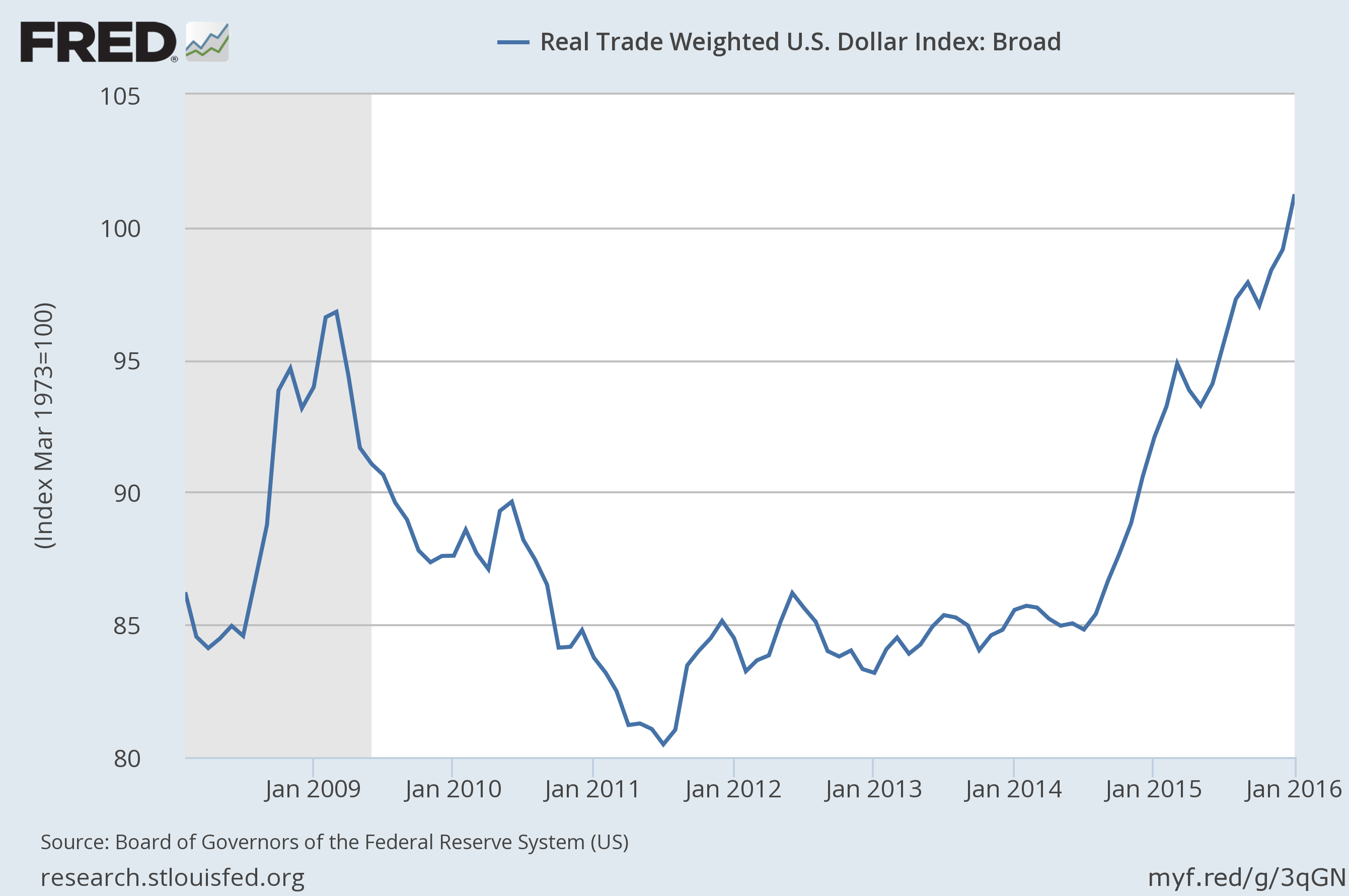

Before we delve further into Yellen's comments and what they mean, let's take a look at some indications of those financial conditions Yellen references. First and foremost, the S&P 500 is down about 15% in price returns, in data from Bloomberg, since its nearby peak in May 2015. The yield on the ten-year Treasury is down nearly 90 basis points since June 2015. And the dollar is up about 19% since mid-2014, using the broadest measure against 26 currencies, including a number of emerging markets, as published by the Federal Reserve. But there's more, so let's discuss each of the metrics Yellen mentioned in her quote above.

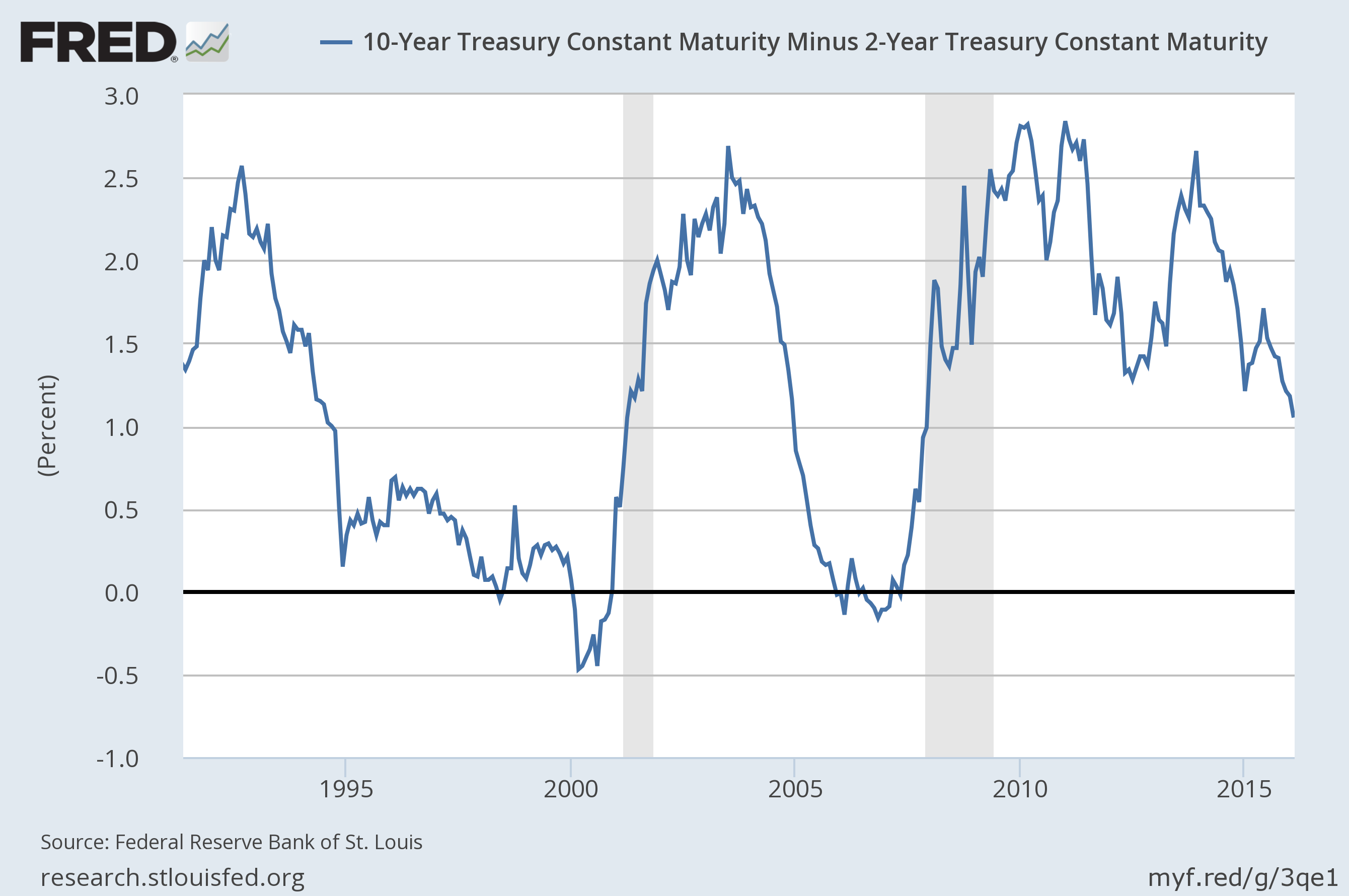

The Impact of a Flattening Yield Curve

The yield curve has been flattening as yields have fallen across the longer end of the yield curve, compressing the difference between the yield on the 10-year Treasury and the 2-year Treasury. While a seemingly arcane measure, this representation of how steep (or flat) the yield curve is, actually has important ramifications for the economy, and banks in particular.

Banks lend at usually longer term rates and borrow at short-term rates, such as from depositors and short-term financing. As a consequence, they profit from the difference between short and long term rates. When this difference narrows, banks become less profitable. And ergo, bank stocks plunged recently as the yield curve flattened. The difference between 10-year Treasuries and 2-year Treasuries is now just 95 basis points, the lowest since December 2007. This has second-round effects on the economy, as less profitable banks can mean layoffs in the banking sector and possibly more restrictive lending conditions. This can hamper economic growth.

A flattening yield curve has important signaling properties as well. During most recessions going back decades, the yield curve has inverted before each of them, in data from the Federal Reserve. Since short-term rates are kept extremely low by current Fed policy, it is unlikely the 10-year Treasury yield, currently at 1.58%, would fall below the 2-year Treasury yield of 0.63%. However, a flattening yield curve anticipates that the Fed would likely cut interest rates, or at least not raise them and instead, keep them lower for longer.

Rising High-Yield Bond Spreads

Spreads on high-yield debt relative to Treasuries have gone the other way. Rising high-yield spreads indicate greater risk aversion by the markets, and this also raises the funding costs for businesses who must issue new bonds to finance current operations or future growth. Like a flattening yield curve, rising high-yield spreads have often presaged periods of slower economic growth, and sometimes, recessions.

Lately, of course, they have been influenced by the energy and commodities sectors, which makes up just 4% of GDP, according to the Bureau of Economic Analysis, and roughly 1.5% of private sector employment, according to the Bureau of Labor Statistics - but 17% of the high-yield market, according to J.P. Morgan.

A Surging Dollar

A third point Yellen mentioned was the rising dollar (which has recently reversed in recent weeks). As we noted earlier, the dollar has surged by 19% since mid-2014. A rising dollar dampens inflation by making imports cheaper. More importantly, an overly-strong dollar can slow the economy by reducing exports, which become more expensive to foreign consumers, and by hurting U.S. based multinationals with operations abroad, which face both lower repatriated profits when translating foreign earnings and revenues into dollars and by increasing competition from imports.

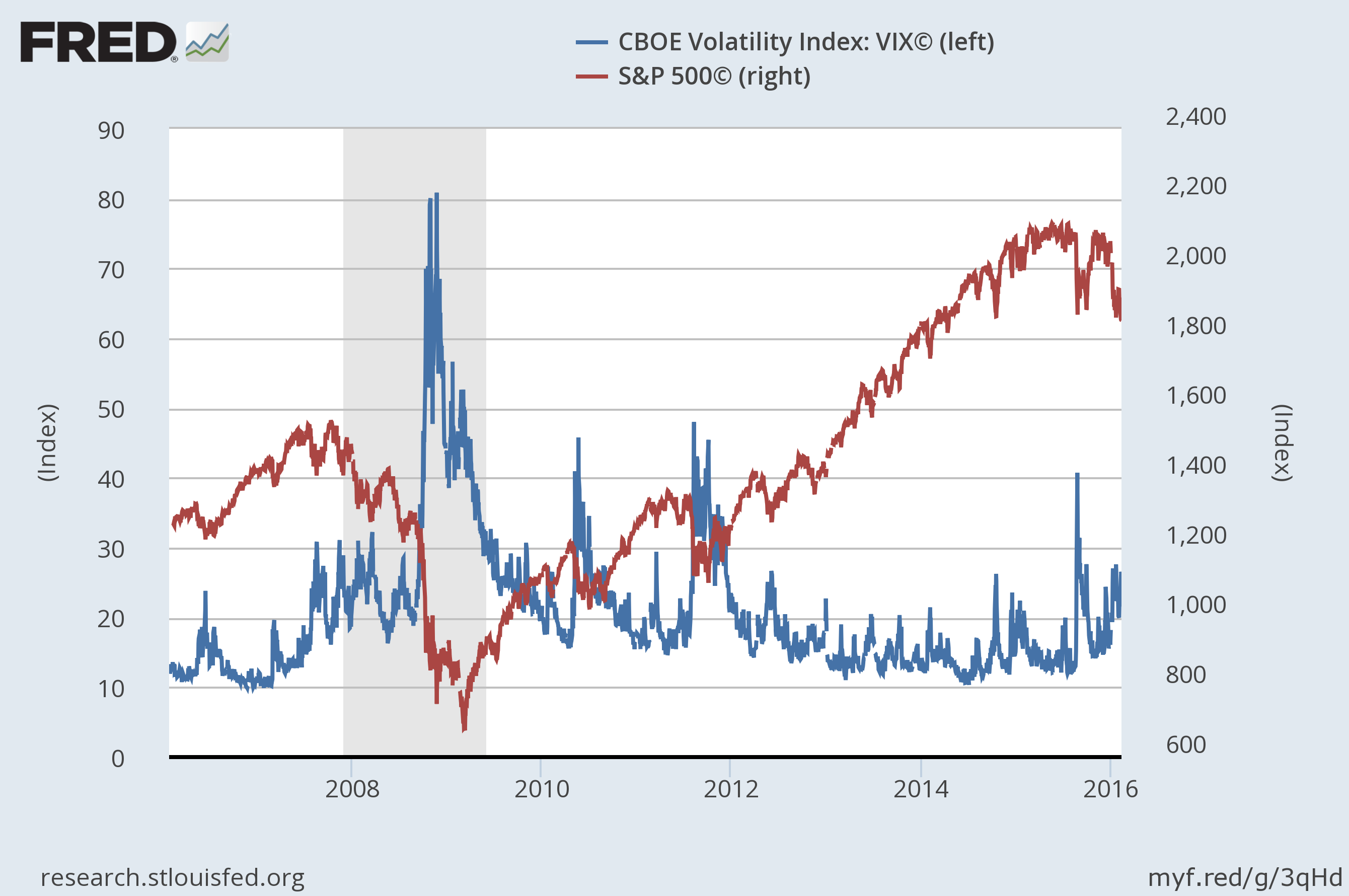

Rising Stock Market Volatility and Falling Share Prices

As to the ramifications for investors, all of this has translated into more volatility. The Chicago Board Options Exchange (CBOE) measure of expected volatility in the stock market, the popular VIX index (perhaps better known as the market's "fear gauge") recently has been surging higher as stock prices have fallen. There is a direct, inverse correlation to the VIX and equity prices, which do indeed suggest investors have become more nervous.

How Does the Stock Market Affect the Economy?

That, in turn, has translated into a bit of nervousness at the Fed as well. That leads us into our main question, does the equity market predict soft economic growth, or does it cause it, with consumers becoming more reluctant to spend and businesses more cautious about hiring and investing? Bloomberg recently reported that about $3 trillion has been trimmed from American shares since the start of the year, including stocks held globally by both institutions and individuals. Americans have about 35.5% of their assets invested in common stocks representing $17.1 trillion in assets, according to Federal Reserve data compiled by Ned Davis Research. Meanwhile, the initial public offering market has been badly hit by the stock market rout - January was the slowest month for IPOs since December 2008, according to Bloomberg - limiting the ability of new companies to raise capital.

Conclusión

So, given these linkages between financial markets and the economy - which in turn dictate Fed policy - we can see why Yellen is taking a more cautious tone when discussing the outlook for both the economy and Fed policy. However, Yellen did not predict a recession, and instead said she believes growth "will expand at a moderate pace" and "pick up over time."

Remember that previous decades have been littered by false signals. If you examine the graphs above, we saw earlier warning signs, such as in 2011 and 2012, of weakness that never materialized. The Eurozone debt crisis never prompted a U.S. recession, and nor did the 1998 currency crisis, even though both episodes were marked by heightened risk aversion. Even the 1987 crash failed to produce a recession.

Recession risks may be rising, but as with many situations, one must be careful to avoid "false positives" when making investment decisions. Time will tell, but in the meantime, volatility prevails.

0 comments:

Publicar un comentario