Buttonwood

The crazy world of credit

Where negative yields and worries about default coincide

.

THERE was much talk at Davos, the global elite’s annual get-together in Switzerland, of wealth inequality: the gap between the haves and the have-nots. The corporate-bond market is currently displaying a similar divide—between the have-yields and the yield-nots.

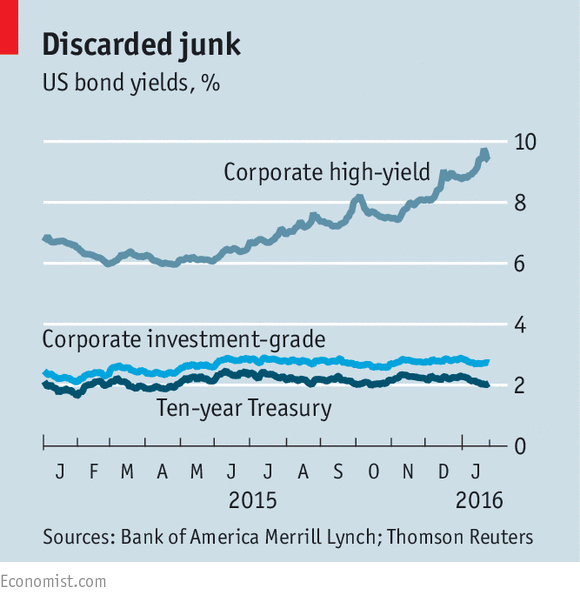

According to Bank of America Merrill Lynch (BAML), around €65 billion ($71 billion) of European corporate bonds are trading on negative yields; in other words, investors lose money by holding them. Yet the rates paid by issuers of low-quality or junk bonds have been soaring.

The spread (the interest premium over government borrowing rates) paid by junk-bond issuers has risen by nearly three-and-a-half percentage points since March last year (see chart). The gap is now nearly as great as it was during the euro crisis of 2011, although it is less than half as wide as it was after Lehman Brothers collapsed in 2008.

Odd though it may seem, these market movements are part of the same trend. As January’s stockmarket wobbles have shown, investors are very nervous and are looking for safety.

Certain corporate-bond issuers, such as Nestlé, a Swiss foods group, are perceived to be very safe. Since the yields on Swiss government bonds (even those with a ten-year maturity) are also negative, it is no great surprise that Nestlé bonds fall into the same camp.

Similarly, investors are willing to accept negative yields on German and Dutch government bonds with maturities of two and five years. Better to suffer a small loss from owning them than risk a big loss by buying a junk bond, which might default. Historically, the average recovery rate on unsecured bonds that default has been just 40 cents on the dollar. Given that risk, investors are demanding a much higher yield from junk bonds.

The proportion of junk bonds deemed “distressed” (defined as having a yield ten percentage points higher than Treasury bonds) is 29.6%, up from 13.5% a year ago. That is the highest ratio since 2009, according to S&P. Unsurprisingly, given the fall in energy prices, the oil and gas sector accounts for the biggest share of issuers in distress, at 30% of the total. The default rate, at 2.77%, has virtually doubled from the low of 2014 (although it is still below the historical average of 4.3%).

Matt King, a credit strategist at Citigroup, thinks the reason for the turmoil is the reduced support that central banks are offering financial markets. For several years the Federal Reserve and the Bank of England used quantitative easing (or QE, the creation of money to buy assets) to drive down yields on government bonds and thus encourage investors to buy riskier assets, both equities and corporate bonds. Both have now stopped using QE (although they have yet to sell their piles of acquired assets); the Fed has also raised interest rates.

Although the European Central Bank and the Bank of Japan are still buying bonds, their efforts are being offset at the global level by sales by emerging-market central banks, including China. Net asset purchases by global central banks dipped last summer (coinciding with another market downturn) and recent data show they have done so again.

Given this backdrop, investors are sensitive to bad news. The fall in commodity prices and the slowdown in emerging markets are two adverse developments; those sectors were “where the growth was”, as Mr King points out. Corporate-bond investors have also noticed that profit forecasts have been revised lower in recent months in every industry in America. In short, Mr King concludes: “When monetary stimulus’s effect on markets fails to be matched by a corresponding improvement in the real economy, we are inevitably vulnerable to a correction.”

The big issue for the corporate-bond markets is whether the sell-off is self-perpetuating.

According to BAML, investors in high-yield bonds globally have withdrawn $4.9 billion in the past seven weeks, equivalent to 5% of their assets under management. Those withdrawals force fund managers to sell bonds, creating bigger losses for the remaining investors and encouraging more withdrawals. The impact is exacerbated by the poor liquidity of corporate-bond markets.

Banks have reduced their market-making activities in the wake of regulations imposed after the financial crisis of 2007-08.

The sell-off will be stopped if yields rise to a level where long-term investors (pension funds and insurance companies, for example) think the bonds are a bargain. But those investors probably need a dose of good news to persuade them to open their wallets.

0 comments:

Publicar un comentario