Fiat Money Versus Gold: Is It Showdown Time?

by: Katy Delay

Historically the Fed has failed to call the market; quite the contrary, it has almost always intervened in the wrong direction at the wrong time.

The Fed's reliance on statistical analysis has not proven to be an effective forecasting tool.

In keeping with its historical record, the Fed attempted in December to reverse its low-interest-rate policy just as the economy is beginning to show signs of malaise.

The Fed will have to retreat on its promises and has now managed to paint itself into an extricable corner.

No ordinary investments are truly safe in this context, hence the advisability of owning gold as a safe haven and as the only real store of value we have left.

The Fed's reliance on statistical analysis has not proven to be an effective forecasting tool.

In keeping with its historical record, the Fed attempted in December to reverse its low-interest-rate policy just as the economy is beginning to show signs of malaise.

The Fed will have to retreat on its promises and has now managed to paint itself into an extricable corner.

No ordinary investments are truly safe in this context, hence the advisability of owning gold as a safe haven and as the only real store of value we have left.

Without attempting to rub it in, I can't help but observe that the Fed has failed miserably at the art of curing, or even of predicting, business cycle downturns, perhaps with only one exception: Paul Volcker's courageous actions in the early 1980's.

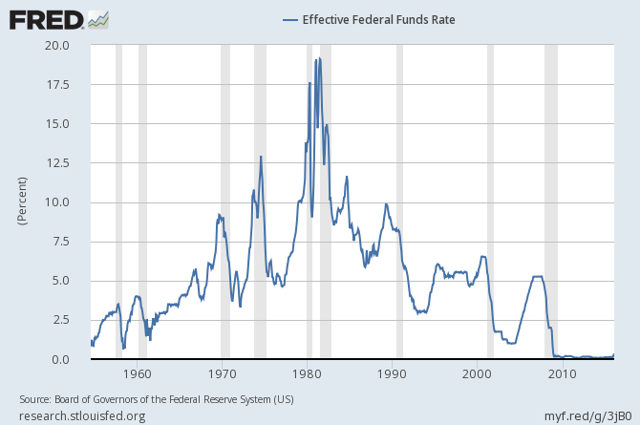

One has only to look at the following chart to see that before every other recession, the Fed has come to its senses and raised the fed funds rate sharply, only to realize after the fact that their actions were too-drastic because too-late.

This becomes all the more apparent when one lays the above graph over the following one that illustrates expansions and contractions.

{kind=link}

Putting the two together, one could conjecture that the Fed probably had at least a proximate causal relationship with the booms that preceded the busts, i.e. that it may have lowered the fed funds rate too much thereby encouraging over-expansion, and that its subsequent tardy raising of rates was not timely or effective as a cure of the disease, quite the contrary.

Our current business cycle expansion seems to be the most precarious of any of the previous ones seen in the above charts. Why? For five reasons. First of all, it's an exceptionally long one.

Secondly, the Fed has demonstrated its ineffectiveness having tried unsuccessfully on three occasions to increase price inflation. Instead, it has inflated its own balance sheet to unsustainable proportions without any credible plan for unwinding it.

And it is not alone. See the chart in this article that gives us similar news about the other major central banks of the world.

Third, some of the imbalances that contributed to the Great Recession are still in play.

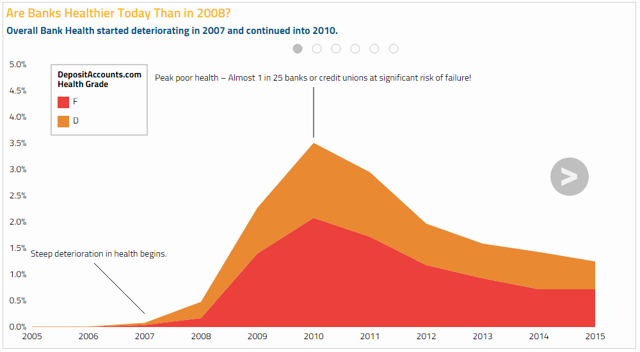

Fourth, banks are not in good shape, even after all this time.

Fifth, since January we have all noticed that the global economy is hiccupping. (Global Stockmarkets Panicking)

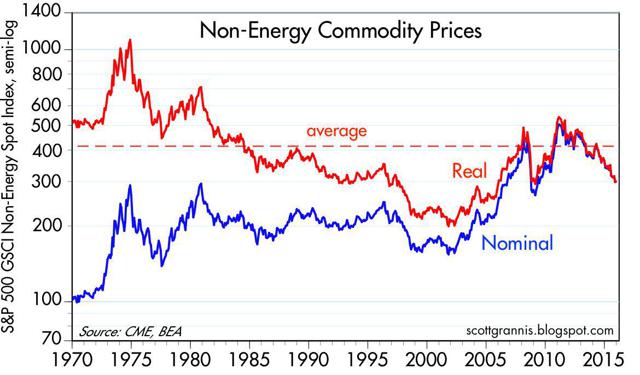

In reality this has been coming for the past three years, which we would have seen if we had been paying attention to commodity prices that have been falling steadily.

{kind=link}

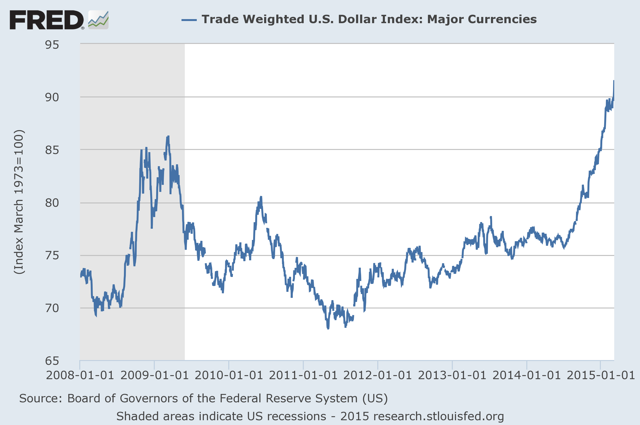

And the caboose: the dollar's rise relative to other currencies is not helping our exporters, nor is it making life any easier for those countries whose debts are in dollars. It's hard to know whether the expanding US economy and/or expected Fed actions are doing this, or whether it's the other countries doing their best to devalue their own currency to save their own economies (even if it won't work).

{kind=link}

In the face of all of this, what about Fed policy? Has it been effective in getting the US out of our Great Recession slump? Some would argue that, on the contrary, the Fed has kept us from climbing out of that slump by ignoring some of the hard realities of economics, e.g., the pricing mechanism.

Prices are a measuring instrument. They are signals. They signify something (or they should, anyway) about the value to buyers of whatever it is they want to purchase. When someone fiddles with prices, they can no longer fulfill their function as communicators. They begin instead to communicate something other than the value to buyer of things to be purchased.

For example, why have prices not increased with the increased supply of credit? Well, they have, but not in the usual places. Some real estate sectors, for example, are exploding, and so are the stock markets, or at least they were up until December of 2015. Apparently, the marketplace has figured out that the new credit is not for use by the "ordinary" marketplace but is instead meant to gravitate to the speculative marketplace. And it has. (And by the way who profits from that? Not your ordinary middle class American who can't even make a decent return on his savings-condoned embezzlement if you ask me, and not on the part of the banks, rather on that of the Fed's messing with prices! Income redistribution at its worst.)

When and how will things return to normal? In my opinion, they cannot without first a tremendous upheaval as soon as the world realizes that the central banks do not really control price inflation, GDP, interest rates, or anything much at all. Professor Bernanke had us all convinced the Fed could raise interest rates at will, that the central bank is all powerful and can affect any market it pleases. But the Fed's many-month hesitancy to change course and its recent about-face concerning raising rates have begun to crack the facade.

Will a flight from the dollar ever occur? Who knows? Maybe the puppeteers can spread the BS for a while longer. Meantime, a few commentators are making really good sense when it comes to evaluating our current situation-for example, James Grant, who is interviewed by Kitco in a recent New York Sun article.

Grant is bullish gold, and he is skeptical of the Fed's power to do anything other than let rates go negative in the coming months.

Meanwhile, Mrs. Yellen blames Europe and Asia. But as the Sun puts it: "Someone needs to say what a sorry spectacle it is for Mrs. Yellen to make a move on interest rates in December and blame the rest of the world in February."

I'm with Mr. Grant. Gold just may soon rediscover its real purpose in life as a store of value, especially if world governments and central banks are left powerless in the face of "irrational" market fears. In fact, those fears seem quite rational to me, especially given the past forty years of unfounded and irresponsible experimentation with fiat, i.e. bureaucracy-set, monetary policy.

0 comments:

Publicar un comentario