Cutting The Gordian Knot

by: Kevin Wilson

Greek legend tells of Alexander the Great demonstrating "thinking outside the box" by cutting the famous Gordian knot with his sword, thereby winning for himself an entire kingdom.

Economists have shown that there are five ways to deal with a debt crisis: austerity, increased private savings, economic reforms, currency devaluation, and default.

A McKinsey Global Institute study a few years ago showed that 75% of debt crises have been resolved by austerity, and the remaining 25% by hyper-inflation, devaluation, or default.

Unrealistic attitudes on the part of politicians delay decisions until only the worst case scenario remains as an option - but they would do better to cut the Gordian Knot.

Economists have shown that there are five ways to deal with a debt crisis: austerity, increased private savings, economic reforms, currency devaluation, and default.

A McKinsey Global Institute study a few years ago showed that 75% of debt crises have been resolved by austerity, and the remaining 25% by hyper-inflation, devaluation, or default.

Unrealistic attitudes on the part of politicians delay decisions until only the worst case scenario remains as an option - but they would do better to cut the Gordian Knot.

In Greek legend the challenge faced by Alexander the Great in 333 BC was to untie the famous Gordian Knot, which tied a mystical ox-cart to a post for many years in the kingdom of Phrygia, a vassal state of the Persian Empire. Alexander conquered the Kingdom of Phrygia that year, and decided to try his luck with the legendary knot. Anyone who successfully disentangled the knot would by tradition become king of Phrygia, one of the many titles Alexander sought. One legend has it that Alexander, when unable to untie the knot on his first try, simply pulled out his sword and sliced through it.

Ever since then, "cutting the Gordian Knot" has served as a metaphor for solving an intractable problem (i.e., disentangling an impossible knot) by "thinking outside the box." This metaphor comes in handy when we start to consider how to resolve the global debt crisis, which lingers on now seven years after the Lehman Brothers collapse brought the world financial system to its knees.

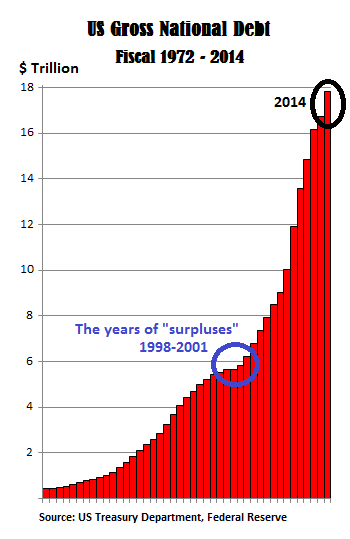

In fact, as I've stated elsewhere, global debt has increased by $57 trillion since 2008, and the debt/GDP ratio has soared almost everywhere on the planet. This is a sign of the complete lack of seriousness that world leaders have applied in dealing with one of the fundamental causes of the Great Financial Crisis (GFC): monstrous, unsustainable levels of debt. This is also the primary driver of all other Balance Sheet Recessions (BSRs), e.g., France in the 1719 Mississippi Bubble, the US in 1929, Japan in 1989, etc. But whether our modern leaders are indifferent, or just incompetent, hardly matters. In the end we will be forced by circumstances to deal with the global debt overhang.

.

Famous economist and analyst Lacy Hunt, and others, have shown that the historically tested solutions to debt crises include: 1) government austerity plans; 2) massively increased private sector savings; 3) structural economic reforms; 4) currency devaluations; and 5) default.

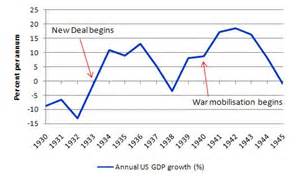

For example, the real reason the high debt levels of the Great Depression were able to be substantially cut, allowing growth to resume in the mid-1940s, was not FDR's New Deal programs or huge war spending, as is popularly believed. On the contrary, what happened was that there was a huge surge in private sector savings to 26% of GDP in 1942-45 as a result of the strict rationing programs during World War II. The increased income from exports during and after the war also added to the surge in savings. Since the savings and income surges allowed debt service to be reduced sharply, the economy was able to recover rapidly.

,

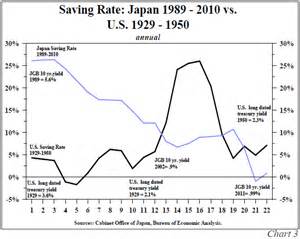

Now compare this to what happened in Japan over the last 2 years. The Japanese savings rate plummeted from a famous high of 25% in 1989 to a current low of 1%, leaving nothing to pay off the overhanging massive debts accrued during the real estate bubble of the 1980s, or the Keynesian stimulus programs that followed. Japanese GDP completely stagnated at the same time, as a result of a massive BSR that kicked off a debt-deflation cycle, freezing real wages for most workers more or less permanently.

Meanwhile, as mentioned above, government spending soared as Keynesian stimulus was applied a total of more than 20 times. Since the stimulus didn't really work, Japan has never fully recovered, although it has been drifting more or less in a state of stable disequilibrium for years.

The government debt/GDP ratio in Japan has soared to an estimated 225%, and the BOJ has applied Quantitative Easing (QE) at least 11 times now, setting the world standard for blowing out a central bank's balance sheet. And yet Japan faces still another recession.

.

A study by the McKinsey Global Institute a few years ago showed that 75% of the 32 global debt crises that have occurred since the 1930s have been resolved by austerity. The remaining 25% of these historical crises were resolved by hyper-inflation waves and/or currency devaluation/default episodes, but all of these cases were emerging market economies with weak central banks. In other words, governments in general have imposed austerity to resolve debt crises, or paid the price later with default and/or devaluation.

It would seem that not making a choice is the same as making the worst one possible. This is where the Gordian Knot metaphor comes into play. Why don't governments do what must be done before doom descends on their economies? It is human nature, and the political process that makes this so difficult. People were enraged when (ironically with respect to our metaphor) the Greeks were forced into tough austerity programs by the EU, the ECB, and the IMF. But the only alternatives were devaluation (not available in the Eurozone) or default, which they eventually did. The Greek people were subjected to a depression as a result of their delay in facing facts.

A collective sort of Pan-European currency devaluation is now occurring in the Eurozone. In spite of a weak central bank structure, the ECB has nevertheless already "printed" vast sums of money (>$3.0 trillion) under its ESM, LTRO and other bond-buying regimes, and has just promised to do even more. The EU currency has as a result already fallen some 22% from its recent high in March of 2014, relative to the dollar. In effect the ECB has recognized that Germany, with its government debt/GDP ratio already above 80% (and with commitments to at least $837 billion of bailout spending), simply cannot be expected to continue bailing out all of southern Europe. Certainly German politicians themselves have been deeply concerned about bailouts getting out of hand.

.

The ECB's new QE program was a tacit admission of this limitation. The solution for Europe thus appears to resemble a typical emerging market-type solution, involving in this case a hodgepodge of austerity in some places, default in a few places, and devaluation of the euro everywhere.

Unfortunately the euro, because it is a currency union, cannot be devalued in one country at a time to deal with a crisis. So the recent Pan-European devaluation has not been sufficient to pull Greece or Italy or Ireland out of the swamp of debt they have fallen into. The Germans have pushed for ever more austerity in light of this problem. Thus Mrs. Merkel (Chancellor of Germany) may have had it mostly right, with perhaps too much emphasis on austerity and not enough on reform, with weak euro currency devaluation along for the ride.

On the other hand, the EU periphery's big spenders may have it mostly wrong, with not really enough emphasis on austerity or structural reform, and no access to national currency devaluation as a tool unless they leave the Union (via "Grexit").

.

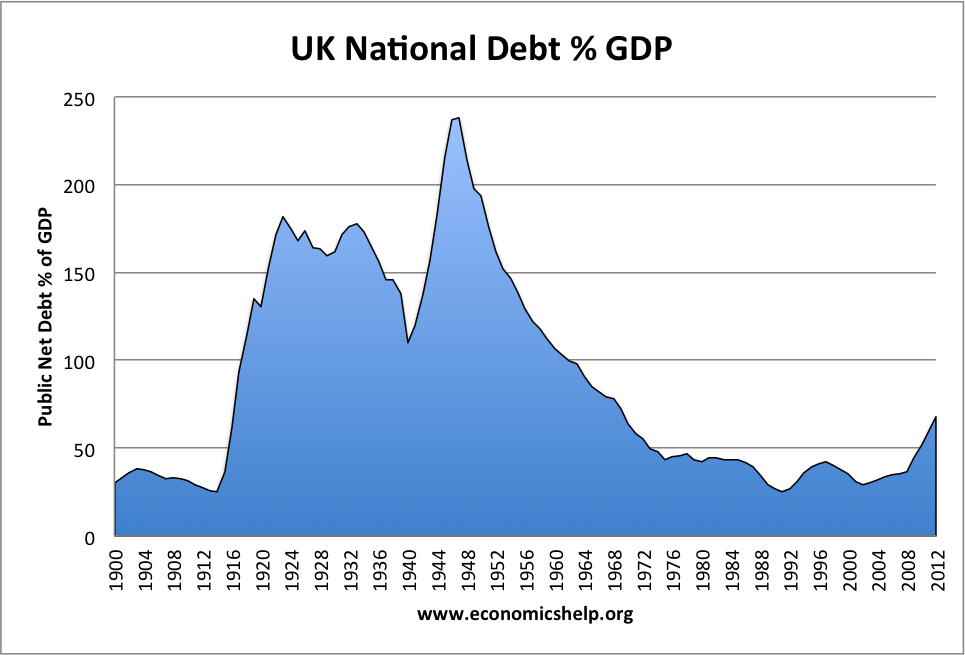

A rather spectacular example of a country surviving a huge debt crisis is the British Empire after the end of the Napoleonic War in 1815. Debt had climbed over a period of 100 years as one war after another was fought, reaching its zenith of 237% of GDP in the year after Waterloo, and yet the British Empire survived. A combination of currency devaluation during and after the Napoleonic War, a linking of the currency to a gold standard after 1821, and higher taxes through many decades allowed the debt to be paid off over the next 100 years.

World War II sent them back to the same general level of debt as in 1820, but again the UK got its debt under control by various measures, this time taking about 45 years to reduce it to about 25% of GDP. Some observers have noted that there are also plenty of modern examples of austerity working as a solution to debt crises.

One very good example was the US depression of 1920-21, which has been reported on in depth by famous analyst James Grant. In this depression, during which nominal GDP fell by 23.9%, inflation (CPI) fell by 8.3%, and wholesale prices dropped by 40.8%, as unemployment soared from 2% to 14%. The administration of Warren G. Harding met this challenge by balancing the budget (!), and the Federal Reserve actually raised rates rather than lowering them. The result was a surge in industrial production during 1922 of 27.3%, and by 1923 unemployment was back down to 3.2%. This can hardly be described as a Keynesian response, and yet it appears to have worked.

.

Two more recent examples where austerity seems to have worked relatively well are Germany and Sweden. They each moved to near-balanced budgets in 2009-11 after the Credit Bubble and GFC, enjoying sustained strong growth. Apparently austerity didn't hurt them much, since they experienced annualized real GDP growth rates of 3.6% and 4.9%, respectively over several years.

These countries still look like the best of the bunch even as Europe begins its fifth year since the 2011 banking crisis. In contrast, countries with high deficit spending in the last few years, like Greece, Portugal, Spain, Italy, Ireland, and the Netherlands (with average deficits of 3.0 to 7.9% of GDP over the years) are still experiencing follow-on problems, such as renewed banking troubles, high unemployment levels, crushing debt burdens, and capital flight.

.

Two other examples, from Finland and Sweden back in the early 1990s, involved strong recoveries from financial crises and recessions following major currency devaluations and austerity. In each country, an initial deleveraging phase was followed by substantial bank reforms and structural government spending reforms. Both countries ended up cutting their annual deficits, and then their government debt significantly within a single decade.

For still another example, we can examine what happened in the US during the inter-recession growth recovery between 1933 and 1937 (during the Great Depression but before the big savings surge of the 1940s). There was a huge surge in GDP to an average of 7% growth annually, which was caused in part by a 60% devaluation of the currency when we went off the gold standard.

The growth interlude within the Great Depression ended in 1937 when other countries also went off the gold standard (causing more competition), the Federal Reserve tightened monetary policy too soon, and FDR raised taxes to an 83% top marginal rate. Only after another deep recession with high (20%) unemployment had ensued, and World War Two had begun, did the surge in austerity-driven savings and export income of the war years save us from the Great Depression.

.

The dilemmas faced by Japan, or parts of the Eurozone, or China and other emerging markets right now, are just previews for what we in the US will someday face as a result of slow growth and ever higher debt. The pattern of government expenditures over the last 20 years provides a shining example, if one is needed, of what happens when supply-side economics is used to guide the federal budget, instead of the discredited but ever-popular Keynesian theory. Under President Bill Clinton, supply-side economics prevailed as government spending declined from 23.5% of GDP to 19.5% of GDP, and the deficit declined each year until there was an actual surplus when he left office. Tax rates were moderate to low. Unemployment was moderately low and manufacturing was a healthy part of the economy. The entire economy did rather well during this period, as you may recall.

In contrast, under President George W. Bush, tax rates were even lower, but unfortunately government spending increased to about 22.6% of GDP as spending soared, and then exploded as the financial crisis unfolded late in his second term, and every possible Keynesian gimmick was tried to stimulate the economy. Finally, under President Barack Obama the deficit spending became astronomical in scope, with total outlays climbing to a high of 27.3% of GDP in 2009. Spending slowed after the 2010 by-election, but deficits are still in excess of $400 billion per year.

In any case, we know that all of this excessive spending in recent years has been accompanied by a very weak economic recovery, which is not at all what the Keynesians predicted. Thus, the changing patterns of spending over the last 20 years, and the resulting long-term economic weakness in which we find ourselves do not support the Keynesian dogma, at least when a credit bubble and the resulting BSR are involved.

.

A huge debate thus continues in the financial media and amongst policy makers as to how we should deal with the global debt crisis. Although there are many complex issues involved, a discussion of which is outside the scope of the present commentary, we do know some simple things that have worked historically and would work again.

This debt crisis has lasted longer and done more damage than was perhaps necessary, in part because the essentials learned in other crises have mostly been ignored. Austerity leading to high savings rates, combined with banking reform, structural entitlement reforms, moderate tax increases and in extremis, currency devaluation have been very effective in a variety of countries over many decades. We can choose a better path than the one we have collectively been following, and bring economic growth back to life in the US, China, Europe, Japan, and elsewhere.

What is needed is for us to act in each case on a practical basis using proven methods grounded in economic history, rather than blindly misapplying Keynesian economic theory to every situation, regardless of merit, and endlessly stalling to avoid the inevitable. Voters in many countries may not yet fully understand this, but their leaders will do them a great service if they set out to resolve their part of the global debt crisis using this pragmatic approach to ending the pain.

They should cut the Gordian Knot.

..

0 comments:

Publicar un comentario