China Or Soros: Who Is Right?

By Valentin Schmid

The falling yuan and slowing economy must be wearing on the Chinese regime. Otherwise, why would they publish a childish op-ed on the People's Daily front page attacking billionaire investor George Soros, titled "Declaring War on China's Currency? Ha Ha."

First of all, nobody knows whether Soros is really declaring war on the yuan. He only said he was sure Asian currencies and China would have a hard landing at an interview at the World Economic Forum in Davos last week.

Maybe it was this statement that rubbed the Communist Party mouthpiece the wrong way, as they also defended the Chinese economy at large after making this statement about the currency:

"Soros's challenge for the renminbi and the Hong Kong dollar is unlikely to succeed-there is no doubt."

Aside from the fact that there is doubt if it is just unlikely and not impossible, Soros never said he was targeting the renminbi and the Hong Kong dollar, and even granted China the ability to manage a hard landing.

This did not prevent the People's Daily from blaming him for the steady decline of the yuan.

"Because of his influence, fluctuations in the international financial markets has intensified already existing speculative attacks. Asian currencies obviously feel greater pressure."

So, if we assume Soros is indeed short the onshore or offshore yuan or the Hong Kong dollar, who would be right, the People's Daily or him?

Maybe the Chinese regime thought it had to nip Soros's influence in the butt, because he is usually right about when currencies have to devalue, especially when they are pegged to other currencies.

For starters, he made 1 billion pounds betting against the bank of England on September 16, 1992, when Britain had to withdraw the pound sterling from the rigid European Exchange Rate Mechanism (ERM). Estimates vary, but the Bank of England spent 2 billion an hour in the morning of that day to defend the currency against Soros. Incidentally, this number is close to the $3.5 billion China spent every day in December to defend its exchange rate. At least the Brits gave up in the afternoon. China is still fighting on.

Several officials and politicians have also accused Soros of participating in the demise of the Asian currencies during the Asian financial crisis in 1997, although it is unclear to what degree and how much money he made.

The People's Daily doesn't think this matters much, though, and we should look at the larger historical context: "The continued appreciation of one currency against the US dollar for such a long time, and with an amplitude so large is rare. A slight pullback now is normal."

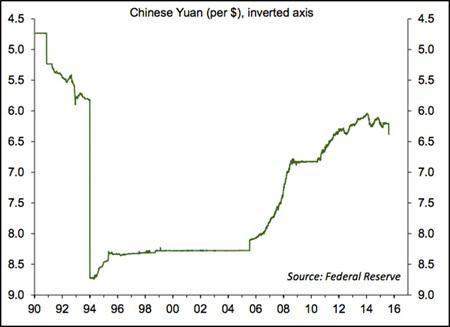

Of course, it helps if the currency devalues 33 percent before it starts to appreciate, like in 1994, which took the rate from 4.7 yuan per dollar to 8.7, but this is beside the point. The point is Soros sees the same problems he saw in Europe in the early '90s and in Asia in the late '90s.

.

(Raymond James)

The first commonality is a dominant central bank tightening monetary policy. This was the Bundesbank in 1992 and the Federal Reserve in 1997, although both started their cycle much earlier.

In this decade, the Fed started tightening monetary policy in 2013 with the beginning of the end of quantitative easing. The recent 0.25 percent rate hike is just the continuation of that policy.

Relatively tighter monetary policy made the Deutsche mark more attractive versus the pound and the dollar more attractive compared to the Asian currencies in 1997 and now.

Relatively tighter monetary policy made the Deutsche mark more attractive versus the pound and the dollar more attractive compared to the Asian currencies in 1997 and now.

The other commonality is a combination of debt and deteriorating assets. Although China has paid down a large portion of its foreign debt, there is still $877 left. This is the unwinding of the carry trade, which was the biggest factor in the Asia currency crisis of 1997 and plays a relatively smaller part for China in 2016.

China shares the fate of the United Kingdom in 1992 that domestic and international investors are losing confidence in the economy and asset markets. Even though the UK raised interest rates from 10 to 15 percent in one day, it did not convince the markets it would sustain that level given a faltering economy.

China is far away from raising rates, and, in fact, is trying to ease domestic liquidity conditions because of an unprecedented economic slowdown. In addition, much like Germany's government bonds were preferred to the UK's in 1992 because of a stronger economy and lower inflation, the United States' stocks, bonds, and real estate are preferred to Chinese real estate, stocks, and bank deposits because of deflation and systemic risks in the banking system.

Of course, don't tell this to the People's Daily. It hopes speculative attacks, which just profit from fundamental economic problems and never cause them, will lead to more financial cooperation between the Asian nations and even a single currency.

"International monetary cooperation from low to high is divided into international financing cooperation, joint intervention in currency markets, macroeconomic policy coordination, joint exchange rate mechanism, and a single currency. The direct power of its deepening is usually pressure from speculative currency attacks," it states.

Of course, the editors missed the point that Germany did not intervene on the UK's behalf in 1992 and founded the euro single currency with the countries who were still part of the ERM - after it won the war against the pound.

0 comments:

Publicar un comentario