Capitalism Is Grinding To A Halt

by: Shareholders Unite

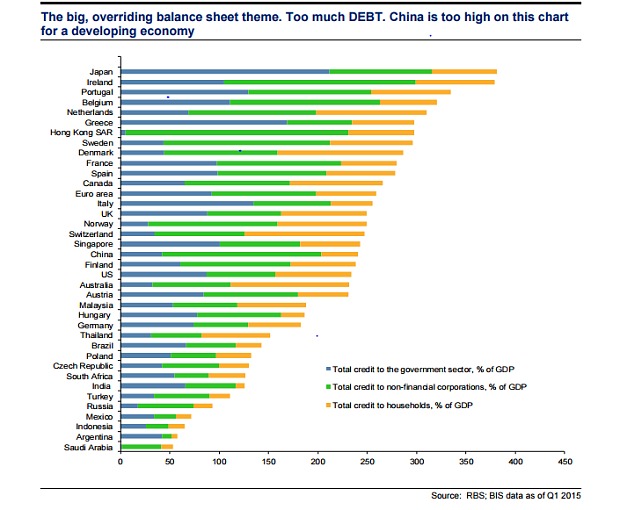

Debt has exploded almost everywhere.

Combined with low inflation and low growth, it risks ratcheting up further, greatly increasing the risk of debt-deflationary cycles.

Debt deflation and other forces are threatening the long-term dynamism of economies, not a conducive environment for investors.

Combined with low inflation and low growth, it risks ratcheting up further, greatly increasing the risk of debt-deflationary cycles.

Debt deflation and other forces are threatening the long-term dynamism of economies, not a conducive environment for investors.

Debt + deflation = disaster

Debt is everywhere, and almost everywhere it is either at record levels and growing, or both.

This holds for private debt and public debt alike.

This holds for private debt and public debt alike.

How did it ever come to this, and what are the implications?

Public debts have several origins, like:

- Baumol's disease

- Shifting preferences

- Recessions

- Political compromise

- Demographics

Not everybody will be familiar with the first reason, Baumol's disease. This explains the automatic increase in size of the public sector because productivity gains are more difficult in services compared to industry.

As the public sector is almost all services, the productivity lag will cause either public sector wages to lag the private sector, or it will automatically increase the cost of the public sector.

It is simply difficult to raise productivity in big swathes of the public sector, like defense, general administration, healthcare and education.

Healthcare is especially problematic. Populations are getting older, new and often more expensive treatments become available and it's difficult to increase productivity.

This is why healthcare is almost everywhere the main threat to the sustainability of public finances, there is little reason to assume its relentless rise as a percentage of GDP is about to halt.

ICT holds some promise (electronic health records, online education, eGovernment, etc.), but this is a very long and protracted process.

Shifting preferences also automatically increases the size of the public sector, when populations become richer, people tend to place more importance on a safe environment, on healthy products, on a cleaner environment, better schools for their children, better healthcare, etc.

All of this makes a disproportionate claims on the public sector (through regulation, justice, law enforcement or direct government involvement).

Recessions are usually a big drain on public finances, outlays increase (unemployment benefits, etc.) while wages, profits and expenditures grow slower or decline, seriously denting tax revenues. More often than not, these effects are compounded by pro-cyclical policy reactions, cutting spending and raising taxes in the midst of a recession, which tend to prolong it.

The public sector faces many demands, and public preferences are often contradictory (many people are against cutting expenditures, but they're also against raising taxes). The resulting political compromise also has a habit of shifting the cost to the future.

Demographics plays an important role in many countries, as it tends to decrease the tax base whilst simultaneously increasing outlays on pensions and healthcare especially. Japan, with its rapidly shrinking population and its 200%+ public sector debt, comes to mind as a textbook case.

All this explains why public debts have tended to ratchet upwards in so many countries, with recessions especially marked.

Private sector debt

Numerous trends tend to increase private sector debt, in no particular order of importance:

- Increased leverage

- Increased inequality

- Greatly reduced interest rates

- Global savings glut

- Demographics

- Cost of capital goods

Without even trying to be anywhere near exhaustive, all kinds of financial innovation and wizardry increased leveraged possibilities, increased inequality led to a lot of borrowing (especially in the US where median wages haven't gone up in decades, this was a way to share in the increased wealth).

Since the 1980s, central banks in developed countries have managed to basically conquer inflation, leading to greatly reduced interest rates.

The latter trend has been reinforced by a global savings glut brought on, in part, by demographic developments and falling cost of capital goods.

The risks

Public sector debt isn't a serious problem unless a substantial amount of that debt is owned abroad, or (even worse) is denominated in a foreign currency.

This is why Japan, despite people betting against Japanese bonds for over a decade, hasn't experienced any immediate crisis, although the level of public debt has reached a point (200%+ of GDP) where serious concerns about its sustainability are warranted.

But one should not lose sight of the fact that almost all Japanese public debt is in the hands of the Japanese themselves (who will inherit not only the debt, but also the bonds), and it's dominated in yen, which the Japanese central bank can print in copious amounts.

Basically, the Japanese owe the debt to themselves, and rather than 'stealing' from future generations, these will inherit the bonds as well.

Risks are much more severe for countries that borrow abroad, especially those that borrow in foreign currency. Any devaluation of their own currency immediately increases the debt, and this is how many developing countries experienced financial crises.

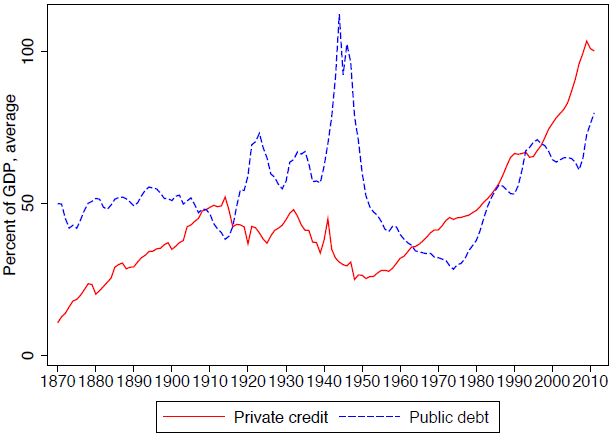

Private sector debt has also been rising fast nearly everywhere and this has been responsible for financial crises as well:

The graph above gives the public and private debt for 17 advanced countries, one sees a marked trend increase in private debt from the 1960s. This matters, as:

History demonstrates that excessive private-sector borrowing plays a greater role than fiscal profligacy in generating financial instability. However, when the credit boom collapses, the government's capacity to alleviate the downturn is limited by the prevailing level of public debt. [Jordà et. al.]

And:

In an update of work on debt and deleveraging, McKinsey notes that between 2000 and 2007, household debt rose as a proportion of income by one-third or more in the US, the UK, Spain, Ireland and Portugal. All of these countries subsequently experienced financial crises. [Martin Wolf, FT]

But the accumulation of public and private debt is very serious even in the absence of a financial crisis for a number of reasons:

- The declining ability of debt to spur growth.

- The accumulation of debt itself can slow growth, a sort of world deleveraging process.

- The accumulation of bad debts can tighten credit standards of banks and other financial institutions.

- High outstanding debt ratios reduce the effectiveness of monetary policy.

- These processes can be self-reinforcing.

The first is most obvious in China, where growth is slowing whilst debt has kept on rising (by 124 percentage points in the debt-to-GDP ratio between 2007 and 2014).

It is obvious that at a certain level of indebtedness, households and institutions start worrying about the health of their balance sheets and their capacity for financing these debts.

This is likely to first result in a reduction of new credit demand, and ultimately, in increased savings and reduced spending, paying off old debts rather than taking on new debt in order to restore the health of balance sheets.

It will be clear from this that monetary policy effectiveness can be seriously compromised if more debtors tighten their belt to pay off old debts.

According to Richard Koo from Nomura, this effect can become so strong as to render monetary policy completely powerless, hence the term balance sheet recession.

Banks can reinforce this process by tightening credit standards, which they might very well do when they become worried about their own balance sheets due to the level of non-performing loans.

This not only can push certain creditors over the edge, it also leads to further declines in credit creation, slowing economic growth.

The slowing economic growth from reduced credit demand and supply, and the ineffectiveness of monetary policy to revive these, can easily worsen balance sheets by reducing incomes and asset values which underpin debts and debt service capabilities.

This, on its turn, can increase bad debts and reinforce the cycle. This doesn't necessarily lead to a so called Minsky moment in which the integrity of the whole system collapses after a tipping point is reached, producing widespread failures and bankruptcies.

If not aggressively dealt with, it can lead to a sort of lingering zombie economy where indebted institutions, companies and households linger on as interest rates collapse and economic growth and inflation slow to a crawl.

Japan has some experience with this, especially in the 1990s.

How to deal with the debt?

There are simply just three ways:

- Boost economic growth.

- Boost inflation eating away the real value of the outstanding debt.

- Write-offs, restructurings and bankruptcies.

A combination of growth and mild inflation used to be the way rich countries dealt with previous debt binges, like the one that resulted from financing WWII.

However, as we explained above, the accumulation of debt and the pervasive effect on balance sheets everywhere is slowing growth and inflation everywhere and this is turning into a self-reinforcing cycle.

Surprising as it may be, the US has done relatively well in this area, at least much better than either the eurozone or Japan, although the latter two each have structural disadvantages that the US doesn't suffer from.

The eurozone is greatly hampered by the inbuilt deflationary bias through the working of the monetary union, which basically functions like the gold standard in the 1930s.

Japan, despite heroic efforts the last couple of years with Abenomics, is simply suffering from ingrained deflation and a strong demographic headwind.

It will also be clear that the resulting investment climate isn't ideal. Low growth isn't conducive to top-line growth, lowflation doesn't give companies a whole lot of pricing power (unless they have a near unassailable competitive advantage for products and/or services that are relatively price inelastic).

The way companies deal with this is to increase the payout ratio, together with buybacks this is over 90%.

This in itself only reinforces the trend of low growth and low inflation, as this shifts income from those with a low propensity to save to those with a high propensity to sabe.

Basically, the economy is slowly moving towards a model where many households and institutions are nurturing weak balance sheets and are spendthrift as a result.

Others are happy to collect relatively meager returns from bonds and/or dividends. There is still a fair amount of entrepreneurial activity, but the formation of new companies seems to have slowed down, as well as productivity growth.

Economies face serious challenges escaping debt-deflationary cycles and hysteresis effects, whilst at the same time trying to revive economic dynamism. Unless these challenges are met, these are not times conducive to producing great stock returns.

0 comments:

Publicar un comentario