The Jury Is In: Creative Destruction Was More Effective Than QE

by: Adam Whitehead

- As the economic normalization begins, the final analysis of QE is reading more like an obituary.

- Janet Yellen has been able to create FOMC unanimity in the absence of consensus - no mean feat.

- As the American economy seems to be out of the woods, the Bank for International Settlements debunks the QE myth.

- The FOMC signals it intends to deflate alleged global asset prices bubbles during the normalization process.

- Judging the correct economic outcome of the collapse in oil prices is a key decision for the FOMC in 2016.

- Janet Yellen has been able to create FOMC unanimity in the absence of consensus - no mean feat.

- As the American economy seems to be out of the woods, the Bank for International Settlements debunks the QE myth.

- The FOMC signals it intends to deflate alleged global asset prices bubbles during the normalization process.

- Judging the correct economic outcome of the collapse in oil prices is a key decision for the FOMC in 2016.

Source: Business Insider.

As the line is drawn under the Fed's QE process, the narrative switches to framing its legacy for posterity. Several winners and losers are now being suggested. Ironically, QE itself is being presented as the biggest loser.

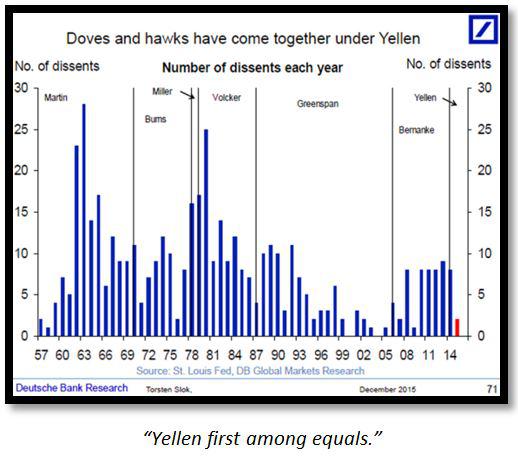

Janet Yellen's most notable success of 2015, was in convincing her FOMC colleagues to trust her judgment in timing the start of the normalization process and its rollout going forward.

The economic data has given support to both the Hawks and the Doves, so Yellen has done a great job in keeping them all within her broad church on monetary policy. This suggests that she will be given greater room for manoeuvre; and will also be able to make a few mistakes along the way since her standing with her colleagues is so high. Yellen has a working mandate in 2016.

The release of the last FOMC minutes showed just how much respect and credibility Yellen has with her colleagues. Considerable concern about the continued failure to hit the official inflation target was evident. The interest rate increase was by no means a slam-dunk decision, with significant dissent around the table. The conflicting economic data easily justified staying on hold. Yellen was able to get unanimity despite the evident lack of consensus. Both Hawks and Doves now trust her to do the right thing by the incoming data and state of the global economy. If Angela Merkel was Time's person of the year in 2015, Yellen just missed out; and could be there or thereabouts if she pulls off this remarkable balancing act throughout the year.

Yellen must have breathed a huge sigh of relief, at the December Employment Situation report, assuming that she had not seen it already. The healthy numbers and some positive framing by Jon Hilsenrath is all that is needed to convince those with short attention spans, who also like to drive by looking in the rear-view mirror, that the US economy is out of the woods.

Yellen's credentials and aura reached new highs as the numbers crossed the tape. The halo effect surrounding Yellen compares even more favourably, when viewed in contrast with that of her peers at the Bank of England, ECB, BOJ and PBoC. As Yellen seems to continue to make the right calls, her global peer group seem as equally prone to making the wrong calls. For now, she can do no wrong.

Now that the US economy is allegedly out of the woods in global pole position and the US Dollar remains supreme as the world's reserve currency, the Bank for International Settlements (BIS) has summoned up the courage to deal the final blow to QE. In a recent report, the BIS destroyed the credibility of Ben Bernanke and his QE thesis.

According to the BIS, the twin assumptions of a global savings glut and secular stagnation that support the QE thesis are bogus. America rebounded from the Credit Crunch, more than its peers, because it was the first and most aggressive to embrace its bad debt liquidation process.

As the Fed normalizes, it can therefore look on with some satisfaction as the ECB and ultimately the PBoC go through the creative destruction phase. The Fed can also temper its enthusiasm for normalization, based on the global headwinds blowing in from the creative destruction phase.

The normalization process is expected to be gradual and punctuated with periods of reflection; and analysis of the steps taken to date and their impacts going forward. Stanley Fischer was the first Fed speaker on deck in 2016; and gave a hint at just how protracted and gradual the process is going to be going forward. Even the title of his speech, "Monetary Policy, Financial Stability, and the Zero Lower Bound," suggested that the process of moving away from the current Zero Bound status quo will be almost imperceptible. He chose to address the normalization through rhetoric, by positing three questions.

In answer to the question "Are We Moving Toward a World With a Permanently Lower Long-Run Equilibrium Real Interest Rate?" he implied that, under the current macroeconomic conditions, the answer is most likely yes. Cryptically, he qualified his final answer, by saying that much depended on the trajectory of fiscal policy. The door is therefore open for a fiscal expansion in the next Presidential cycle.

He then moved on to address the direct criticism of the QE, which states that it creates disincentives for investment and consumption. This came under the rhetorical question "What Steps Can Be Taken to Mitigate the Constraints Associated with the ZLB?" Various suggestions have been made to mitigate these consequences; such as raising the inflation target, raising the equilibrium rate of interest, using negative interest rates and doing away with physical currency. Fischer discounted all the mitigation suggestions at the current time; but said that they are all worthy of further investigation.

Finally, he addressed the issue of the Fed's intentions and capabilities to sustain a tightening in both monetary and financial stability policy, with the rhetorical question of "How Should Central Banks Incorporate Financial Stability Considerations in the Conduct of Monetary Policy?" His answer was clear. Since in his opinion the Fed does not have the panoply of financial stability tools that its global brethren have, it will reserve the discretionary right to use monetary policy as the ultimate financial stability tool.

What can be gleaned from Fischer's exegesis reflects the practical teachings of the Saltwater School of economics that he imbibed and poured at MIT. The Fed is going to play the limited number of policy cards that it has got sequentially. These cards are interest rates and financial stability rules. It will only use interest rates as the ultimate weapon to counteract any financial bubbles if the financial stability cards do not win the round.

Coming after Fischer, Cleveland Fed President Loretta Mester and San Francisco Fed President John Williams both sounded optimistic notes, that stronger growth in 2016 will hit the required KPIs for interest rate increases. There was, however, nothing overly optimistic in their comments, thus underlining Fischer's prosaic projection for the FOMC's gradualist behaviour going forward.

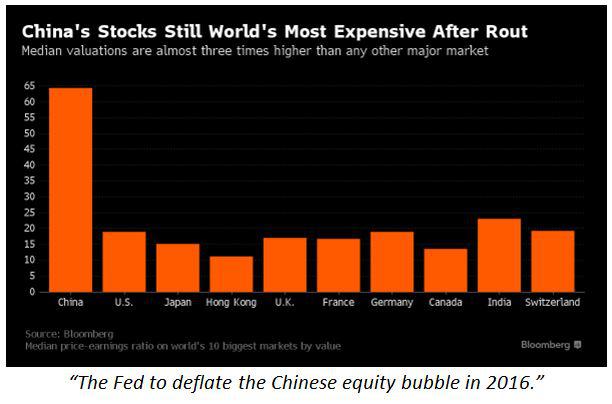

Source: Bloomberg.

Mester's insistence that the collapse in Chinese equities, which triggered a global rout, would not cause the FOMC to deviate from its normalization process was very enlightening. Mester's Hawkish tone was exacerbated by IMF chief economist Maurice Obstfeld's observation that the Chinese economic slowdown was going to create further falls in global equities. Put into the context of Fischer's speech, about bubbles and monetary policy, one could infer that the Fed is deflating a Chinese equity bubble (and possibly a global equity bubble) with the ultimate policy tool of interest rates.

Ever cautious, Stanley Fischer felt it necessary to qualify Mester's comments, within the context of his previous remarks on interest rates and financial stability. In his reframing of Mester's comments, Fischer opined that the markets' assumption of four rate hikes for 2016 was "in the ballpark." He then signalled that the fallout, from the current turmoil in China, made the path of interest rate increases more unpredictable. He therefore confirmed that the FOMC intends to stick to its guns, with four rate hikes, at this point time. The process of deflation of the Chinese equity bubble and the global impacts of this will, however, influence the decisions about future rate increases and their timing.

To underline the aforementioned skill of Janet Yellen in creating unanimity in the absence of true consensus, the Hawk Jeffrey Lacker then agreed with Fischer's ballpark estimate of four more interest rate increases in 2016. Lacker went even further to join the "unanimous," when he said that his prediction is conditional upon there being no external shock to the US economy.

Lacker thereby obliquely referred to the global headwinds that are creating blowback into Fischer's explanation of interest rates and financial stability.

Lacker thereby obliquely referred to the global headwinds that are creating blowback into Fischer's explanation of interest rates and financial stability.

Caution has never been something that Richard Fisher has been known for, either as President of the Dallas Fed or in his retirement. Free from the shackles of the Fed, he felt free to give his own commentary. According to him, the Fed has no tools available for further accommodation.

China and the global economy will just have to suffer. Even more worryingly, he reported that the Fed had deliberately boosted asset prices with QE, immediately after the Credit Crunch.

The inference is that there is an ugly correction in store for equity markets to "normalize" their bubble valuations.

China and the global economy will just have to suffer. Even more worryingly, he reported that the Fed had deliberately boosted asset prices with QE, immediately after the Credit Crunch.

The inference is that there is an ugly correction in store for equity markets to "normalize" their bubble valuations.

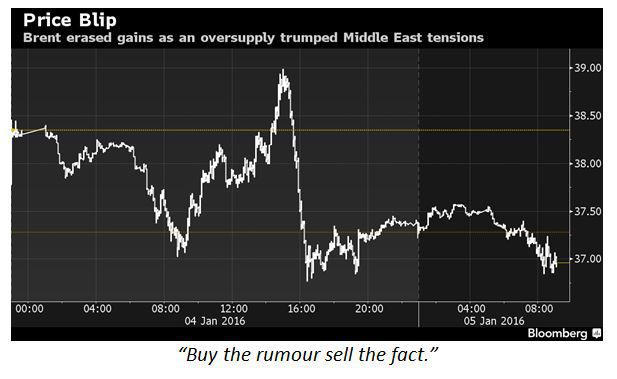

The last report examined the emerging geopolitical headache for the Fed, in relation to the disintegrating situation in the Gulf and its impact on oil prices. Falling in oil prices could be a disinflationary headwind or a tailwind, depending on how one looks at it. The war of attrition between Saudi Arabia and Iran hardened further, after the execution of the Shi'ite cleric Nimr Al-Nimr. The uncertainty initially triggered a rise in oil prices. The Fed should be happy with this; since it, in theory, creates the inflation trigger that will help the Fed hit its inflation target.

Source: Bloomberg.

Looking through the knee-jerk reaction in oil prices, however, a war of attrition implies that both combatants will go after each other by expanding production and driving the price lower.

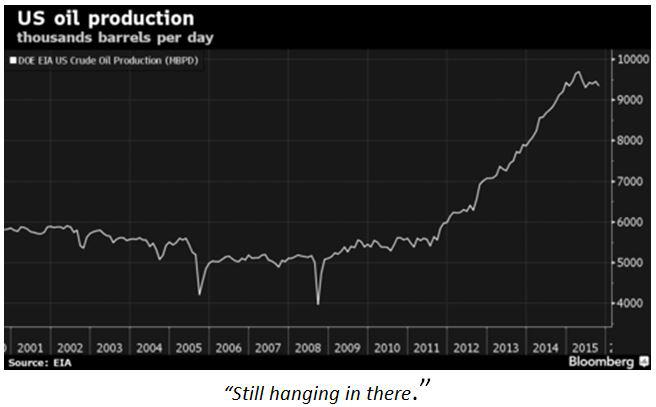

Far from being a casualty in this war of attrition, the US shale industry has just become a major combatant.

The first cargo of US shale oil set sail for the international markets on New Year's Eve, marking the end of 45 years of absence.

Source: Bloomberg.

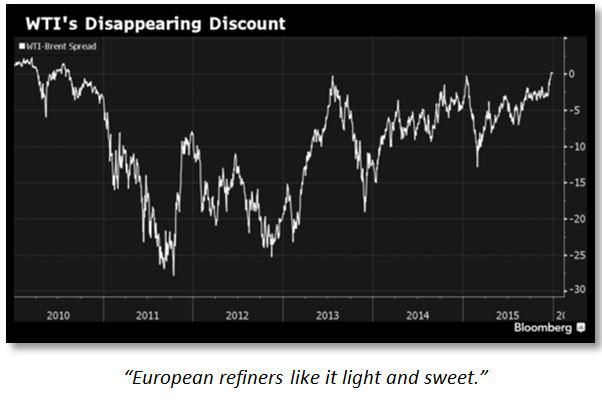

The commonly held view is that US shale is uneconomical to produce at current spot prices; and also that the steep decline curves in shale well production is just about to kick in. The US shale oil being exported is also "light" and "sweet" enough to command a premium in Europe, because it can then be blended with other grades to add value to them. As new global environmental fuel standards vitiate against "heavy" and "sour" grades, the future for US shale looks bright. Global demand for US shale is therefore strong. US shale drillers have also got substantial debts to pay off, so they must therefore continue to remain full-on until bankruptcy and or well declines occur. The recent issue of more shares by Pioneer Natural Resources Co. (NYSE:PXD) shows that there are at least still parts of Texas where oil drilling is economical at these prices.

Source: Bloomberg.

There is also the phenomenon known as the "fracklog" which overhangs the market. It has been estimated that there are 3,994 US oil wells, drilled between January and August 2014, that have since then been idled. Since it is more economical to re-open these wells than to drill new ones, this inventory must be worked through first. The "fracklog" therefore represents another potential source of supply which hangs over the oil Price.

Thus far, technology has been able to not only re-open formerly uneconomical conventional wells to fracking, but also to maintain their productive lives. Low interest rates have then been able to sustain them commercially. If the normalization in interest rates from the Fed is as shallow as the market expects, there may be even more life in US shale. Continued global oversupply of oil, and hence lower prices, look set to remain in place for the foreseeable future.

The Fed is thus faced with a disinflationary risk that may also be a consumer tailwind for the economy. With no clear signal on how this all plays out, the Fed must therefore sit on its hands and watch.

0 comments:

Publicar un comentario