Buttonwood

Picnic for the bears

Fears of deflation and recession hit markets

GLOOM seems to have descended at the start of 2016. Equity markets have had the worst start to the year in at least two decades. The great and the good have queued up to warn of the dangers ahead.

George Soros, a fund manager, said the Chinese financial environment reminded him of 2008, when the financial crisis was at its height. Larry Summers, a former American treasury secretary, declared in the Financial Times: “The global risk to domestic economic performance in the US, Europe and many emerging markets is as great as any time I can remember.”

George Osborne, Britain’s chancellor, spoke of a “cocktail of threats” facing the global economy.

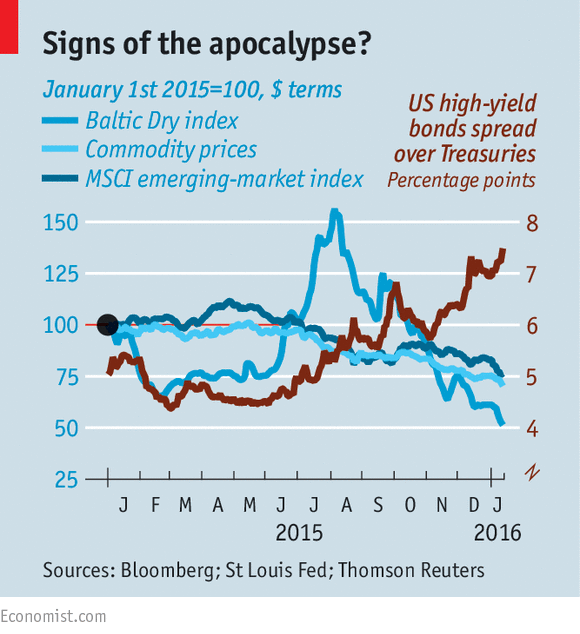

The chart shows a number of indicators of concern, from rising credit spreads (the interest-rate premium paid by risky borrowers) to slumping stockmarkets in the emerging world. Investors have many worries. The first is that the Chinese economy is weaker than the GDP statistics suggest.

Falling commodity prices, the collapse in the Baltic Dry index (which tracks the cost of shipping bulk goods) and the sluggish growth of global trade can all be seen as signs of weakness. Given China’s importance to global growth, this means that 2016 may turn out to be yet another year when growth disappoints.

Mr Soros sees a parallel with 2008 in the rapid credit growth in China and other emerging markets. If growth slows, borrowers may be unable to repay their debts. Similarly, emerging-market companies that have borrowed in dollars may be in trouble if their currencies depreciate. Asian nations might be forced to devalue if China lets the yuan fall sharply.

The second concern is that the Federal Reserve might have miscalculated when it pushed up interest rates in December—the first increase since 2006. The employment numbers in America may still be strong, as December’s muscular payroll numbers showed, but the labour market is a lagging indicator. The Atlanta Fed’s nowcasting model suggests that GDP growth in the fourth quarter was just 0.8% at an annualised rate. Manufacturing looks weak: the purchasing managers’ index has been below 50 (which signals contraction) for two straight months.

A related worry is that the global economy has become over-dependent on the stimulus provided by low interest rates and quantitative easing (QE). Such policies may have saved the world from another depression, but they have not led to a return to pre-crisis growth rates.

Moreover, by pushing up asset prices, they have spurred inequality. Nor has the problem of high debt levels been eliminated; the debt has simply been shifted from the private to the public sector. A swift return to what used to be thought of as “normal” interest rates (3-4%) would prove crippling.

Martin Taylor, manager of a hedge fund called Nevsky Capital, detailed his concerns in a farewell letter to clients. Despite having earned an average annual return of 18% for 15 years, he is closing the fund. He fears that the global economy has become too dependent on China and India, where he does not trust the economic data. Individual equities have also become riskier, since companies have taken advantage of low rates to borrow more. And the equity market is less transparent, with trading dominated by index funds and computer programs.

The risk of sudden, sharp shifts in prices has grown. “We could be caught up in an erroneous market trend, which could then persist for far longer than we could take the pain,” Mr Taylor wrote.

All this is in stark contrast with the idea of fund managers as “masters of the universe” or the Thatcherite mantra, “You can’t buck the markets”. Since 2008 central banks have shown they can bend the markets to their will, at least for a while. Investors have to devote a lot of their time to poring over every word of central bankers’ speeches and statements for a change in policy emphasis.

But perhaps this year’s sell-off indicates that central banks are losing their grip or that investors are less confident the authorities know what they are doing. Albert Edwards, an ultra-bearish strategist at Société Générale (SG), a French bank, says: “The Fed and its promiscuous fraternity of central banks have created the conditions for another debacle every bit as large as the 2008 global financial crisis.”

He thinks a global recession and widespread deflation are on their way. This may still be a minority view, but more people are listening: SG’s annual bearfest in London this week had 850 attendees, a record audience.

0 comments:

Publicar un comentario