Is It Another Oil Supply Cycle Or Something More Ominous?

by: Gary Bourgeault

Summary

- Why this isn't just another supply cycle.

- What is different this time around about the price of oil.

- Most likely scenario for oil over the next year.

- The difference between the last supply glut and this one.

- What is different this time around about the price of oil.

- Most likely scenario for oil over the next year.

- The difference between the last supply glut and this one.

The last time we had a major supply glut hitting the oil market was in the latter part of the 1980s and into the 1990s. By 1998 the price of oil had plummeted to as low as $10 per barrel. As today, Saudi Arabia was one of the reasons for the oversupply, with Mexico and others also contributing to the high production level.

Many believe this is simply another oversupply cycle that will work itself out as it did in the last time. I don't see that happening for several reasons, including the fact that demand from China in the 1980s and '90s was the reason for the rebalancing. This time around China is being downwardly revised concerning its estimates for 2016, and we'll probably see the same in 2017, as its economy continues to slow down.

Supply is also continuing to increase instead of remaining somewhat steady. This time around there is also the supply coming from shale oil, which is the major impetus behind me not believing the current oil price environment can be described as the result of an oversupply cycle. It's more than that - it's a disruption of the industry that will last for decades.

The only question that remains is whether or not demand will increase at levels that can overcome the increasing amount of oil on the market. That also includes the large amount being stored, which will have to be worked through before having much of an impact on the price of oil.

source: money.cnn

Not just another supply cycle or glut

One of the things baffling many investors has been why this current low price environment, which has come about from oversupplying the market, isn't acting in the same way supply cycles of the past have. The answer is this isn't the same as those cycles, and I argue it may not be a cycle at all, but a long-term disruption of the oil market.

There is a possibility a supply cycle could be layered over this disrupted market, but it's hard to see because of the variables associated with supply coming from shale oil producers, and the response to it from traditional oil sources. In other words, this is more than rebalancing supply and demand as we have thought of it in the past. That isn't to say rebalancing isn't part of the equation, but that it's coming from a new source of supply that hasn't been part of the competitive landscape in past cycles.

Consequently, we're in uncharted territory. The way to simplify it is to focus on how supply and demand is working out, rather than the numerous changes happening before our eyes.

Those are important and need to be understood, but they can also be overwhelming and cause investor confusion and paralysis if they aren't taken into consideration in light of normal market fundamentals of supply and demand.

My point is this isn't another supply cycle depressing the price of oil. It's an entirely new source of supply that is coming to the market first in the U.S., and over time, increasing around the world, which now has an estimated 419 billion barrels of recoverable shale oil.

What that means is no matter how the market tries to rebalance in the way it has in the past, shale oil supply is waiting to ramp up and be brought to market. It'll take time to see how this all plays out on a seasonal basis, but over the long term, this has totally changed the oil industry.

What is different concerning oil prices

One other important point to make is in the past the price of oil, when driven by oversupply, has taken longer to rebalance than when price movement is driven by falling demand. Even though the primary driver of prices isn't a supply cycle alone, I do suspect this will be the way this plays out as well.

That's one of the factors confusing some investors because it hasn't happened at this level in a long time. The other factor, as already mentioned, is the introduction of a huge amount of shale oil into the market, which in the years ahead will add a lot more oil to global supply.

Those are the catalysts, but the response to those catalysts is what is putting downward pressure on oil prices. This market is now being driven mostly by fear and emotion, which means it's difficult to know what, if any, fundamentals are being considered by investors when making decisions.

It also means it's difficult to ascertain if the market is being oversold or if it's close to where it should be.

Keep in mind a market is a place where we're supposed to find accurate prices. That's what it's for. When a price is difficult to find, it usually ends up with investors pushing prices down.

Is oil oversold? I have no idea. Some are asserting it is, but that's only because they think the current price doesn't reflect the fundamentals. But when you consider how much oversupply is in the market on a daily basis, I'm not so sure that's really the case.

Going forward it is going to be hard to find an accurate price until the market figures out how to price the now disrupted oil industry. Once that happens, we'll get a better look at where the new price range of oil will move. It will take time.

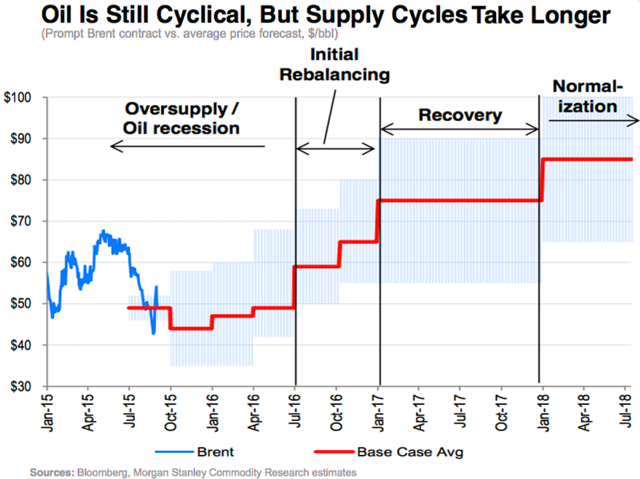

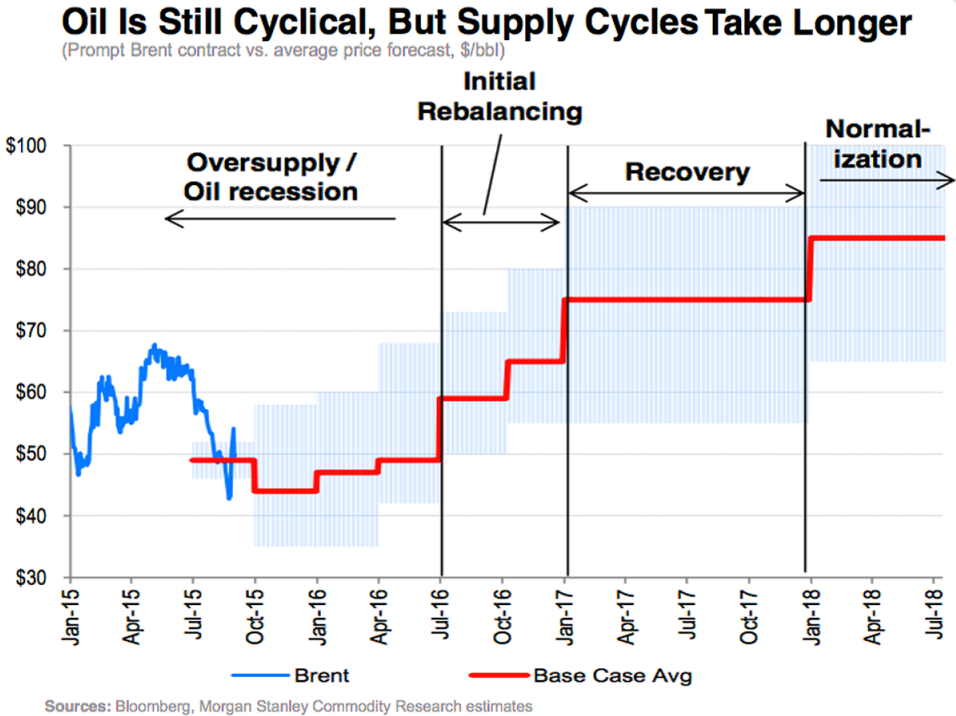

To give you an example, here's a chart from Morgan Stanley in September 2015, revealing its outlook for the price of oil through 2018. It has already missed significantly on the downside, and we're just getting into the new year.

source: Bloomberg, Morgan Stanley

Most likely scenario for oil over the next year

While I'm focusing primarily on the short-term movement of oil as measured by the next 12 months, this is going to be how it plays out for many years into the future.

Shale is the disruptive catalyst in the market, which has led to the response of OPEC and Russia to keep the oil flowing. With that in mind, other than slowing the shale industry down, there is nothing traditional oil producers can do to change the long-term outcome, which is to lose former market share.

The nature of shale production is producers can develop drilled but uncompleted (NYSE:DUC) wells, and then sit on them until they consider the current market conditions the most optimal to start producing from them. They can be brought on line very quickly.

Not only does the development of shale have a strong impact on the market, but it gives producers more control of the higher end of the price spectrum because once the price of oil rises, they can almost immediately bring the wells into production and put more supply into the market.

What this means is when the price of oil finds support, it quickly will be pressured downward by shale producers ramping up potentially hundreds of wells. This will primarily be U.S. shale producers over the next year or two, but will include others as shale deposits in other countries are developed.

For 2016, this suggests there will be an eventual rebound in prices, which should be followed by another downturn as a result of the boost in supply from U.S. shale producers. This doesn't include the export growth coming from Iran's increased supply.

I see some short-term upward price moves, consistently followed by plunging prices. There is nothing visible out there that could be considered a catalyst for price support anytime son.

Conclusión

If we're in a traditional supply cycle, that isn't the primary reason for the ongoing downward pressure on oil prices. This is a disruption and long-term upheaval of the oil industry.

Shale oil, outside its DUC well benefit, with over 400 billion barrels of recoverable shale oil around the world, is disruptive enough. But add the ability to target time frames and you get a ceiling on the price of oil after it makes an upward move.

All of this is important because investors making decisions based upon an oil industry that no longer exists could make some big mistakes. Even now I see some influential financial outlets and analysts treating the industry as if it is the same one we had even a decade ago. It's not.

Possibly more than any time in the history of the oil industry, there is a lack of visibility as to what the range of oil will end up at, because of these new circumstances. This is why so many projections and estimates will fail to come close to what it will be in the short term or long term.

Be wary of outlooks not including shale oil and its unique production advantage. Also watch out for those not understanding how deeply shale oil has disrupted the industry.

0 comments:

Publicar un comentario