The Fed's Devil In The Details

- Discussion of the FOMC actions taken on Dec 16th, 2015 and their potential effects on equity, bond, commodity, capital and asset markets.

- Brief discussion of the FOMC announcement and implementation details.

- Brief discussion of the effects of further squeezing of the "dollar".

"The greatest trick the Devil ever pulled, was convincing the world he didn't exist. And like that, he's gone." - Verbal Kint - The Usual Suspects

Many were focused on the FOMC rate decision of January 16th, 2015. Would they raise or not, and if so how much? Would the statement be dovish or hawkish? Would markets be pleased or not?

Many were focused on the FOMC rate decision of January 16th, 2015. Would they raise or not, and if so how much? Would the statement be dovish or hawkish? Would markets be pleased or not?Lost in the shuffle of the crowd, the Devil in the details.

In brief, this is the third in a series of thematically related missives which will attempt to identify the macroeconomic forces with potential to adversely affect capital, commodity, equity, bond and asset markets.

Again, I wish to dedicate this missive, to one of my mentor's Salmo Trutta, who is a prolific commenter on SA. Without Salmo's tutelage, and insistence in not masticating and spoon feeding the baby ducks, as in learning the hard way, by doing the leg work and earning it, this missive would not have been possible. To you "Proximo"... "win the crowd and win your freedom" - Spaniard

IMHO - Key Phrase in the Fed Speak of December 16, 2015

"The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. "To find the "Devil" in the details, one must always read the fine print. Here is the fine print in the implementation statement…

"The Board of Governors of the Federal Reserve System voted unanimously to raise the interest rate paid on required and excess reserve balances to 0.50 percent, effective December 17, 2015."

"Effective December 17, 2015, the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1/4 to 1/2 percent, including: (1) overnight reverse repurchase operations (and reverse repurchase operations with maturities of more than one day when necessary to accommodate weekend, holiday, or similar trading conventions) at an offering rate of 0.25 percent, in amounts limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day; and (2) term reverse repurchase operations to the extent approved in the resolution on term RRP operations approved by the Committee at its March 17-18, 2015, meeting."

"In a related action, the Board of Governors of the Federal Reserve System voted unanimously to approve a 1/4 percentage point increase in the discount rate (the primary credit rate) to 1.00 percent, effective December 17, 2015."

By reading the fine print found above, we find that in effect the Fed not only raised the FFR (Federal Funds Rate) but also raised the discount rate, IOER (interest on excess reserves), RP - repo and RRP (Reverse Repo) rates all by 25 bps.

Raising the discount rate and FFR (overnight interbank lending rate) is a double edged sword as IBDD's (Interbank Demand Deposits) which are a critical measure of systemic liquidity, have been contracting along with everything else.

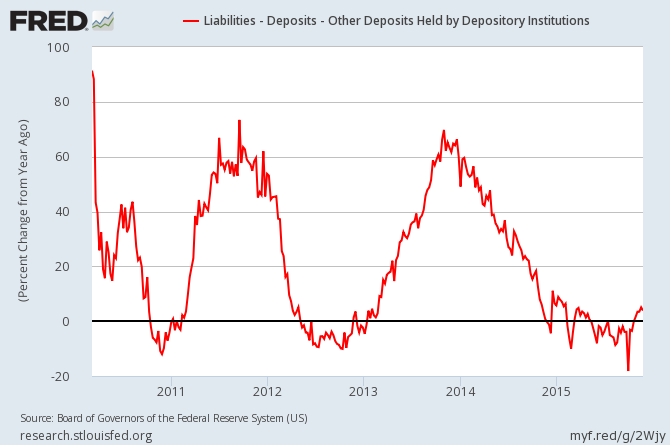

Above note, the YOY percentage ROC (Rate of Change) in deposits, IBDD and otherwise. Note the oscillations coinciding with the Fed expansions of reserve bank credit. Also note the -18% spike in Sept 2015; and that growth has trended negative whenever the Fed fails to expand reserve bank credit. In other words, outside of Fed pumping, the growth rate of deposits in the CB's (Commercial Banks) is negative or in contraction. This is not a healthy systemic condition.

In any event, higher costs get passed on by raising rates and despite being able to charge a higher rate, higher costs can mean lower flows and less liquidity. As Jeffrey P. Snider accurately points out, the FFR is a useless and volumeless policy lever. To wit, RP and RRP transactions dwarf FFR on a daily basis.

Effectively Repo Rates are the overnight rate on everything at the Fed window and circulating in the system. Raising RP repo rates raises the banks cost to park collateral at the window and take a cash or liquidity injection from the Fed. Raising RRP reverse repo raises the Feds cost to siphon cash out (drain liquidity) from the banks while lending out collateral for the CB's (commercial banks) to hold and collect IOER. Higher repo costs generally mean less flow and therefore, less liquidity.

Raising IOER will cause further bank disintermediation and incentivize the banks to sit on excess reserves by paying them twice as much to do so. In other words, it's business as usual, encouraging further bad behavior (staying in the savings rather than lending business) with higher costs, which should further contract flows and reduce liquidity. What this does for increasing or decreasing NIM (net interest margin) which is the bane of the banksters existence,

I will not fathom here.

In closing and to summarize, to have any hope of the global economy getting on its feet again, getting off the zero bound is necessary. However, IMHO unless changes in IOER, RR and RRP rates are made, the FFR and discount rate increase as implemented is going to cause further:

- bank disintermediation

- contraction in monetary flows

- contraction in market liquidity

- contraction in global economic conditions vis a vis economic stagnation and malaise

- contraction in global demand

- self reinforcing squeeze of the "dollar"

- wash, rinse, spin and repeat

All of the above are negative for the US and global economy. Following the FOMC announcement, those who pay attention to the fine print, should find the "devil" in the details and the wise guys portfolio analysts might begin to quietly realign their portfolios accordingly for the New Year.

Since the market potential is broad in both scope and scale, our conclusion could not be more specific than the discussion already had. Again, more grief in the dollar "short" or squeeze and its associated liquidity issues, with the potential to adversely affect capital, commodity, equity, bond and asset markets. Will it happen? TBD, and forewarned is forearmed.

Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of an investment vehicle. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from the principal or a financial advisor.

0 comments:

Publicar un comentario