The Fed and emerging markets

The secular sulk

America’s looming rate rise will expose more frailties in emerging markets

.

THE prospect of interest-rate “lift-off” in America gives investors a reason to take their money there. So it has been odd to see a procession of emerging-market officials call on the Fed to get on with it, the sooner the better. Central bankers from India, Indonesia, Malaysia, Mexico and Peru are among those who have professed a desire for America’s rates to rise.

One explanation is that they are a little like patients waiting to give blood, tired of the excruciating wait and just hoping to be done with it. Things could certainly get painful. As it is, capital is already being diverted away from developing countries and towards America. In 2010-14 non-residents put $22 billion into emerging-market stocks and bonds every month, on average. In November they moved $3.5 billion out, the fourth month of such outflows in the past five, according to the Institute of International Finance, a trade association.

Further outflows in the coming months would put more pressure on the beleaguered currencies of many emerging markets. Depreciation makes their hefty external debts even more daunting.

Dollar credit to non-banks outside America reached $9.8 trillion in the middle of this year; a bit more than a third of that was owed by borrowers in emerging markets, according to the Bank for International Settlements, a forum for central bankers.

To defend their currencies, central banks can raise interest rates in line with the Fed. In recent weeks Peru, Chile and Colombia have done just that in anticipation of lift-off, as have Angola, Ghana, Zambia and others. Higher domestic interest rates, though, come at a cost, dampening economic activity. They also make it more expensive for companies to refinance domestically, a problem since the bulk of their new debt in recent years has been in their local currencies.

Whichever route emerging markets choose to take, in other words, some pain is inevitable—hence the desire to get it over with quickly.

Another explanation for their sang-froid in the face of the Fed is that the worst might already be behind them. It has been a brutal year for the assets and currencies of many developing countries. Average real exchange rates for emerging markets, excluding China, are now as weak as in late 2002, when investors still had raw memories of the crises of the 1990s.

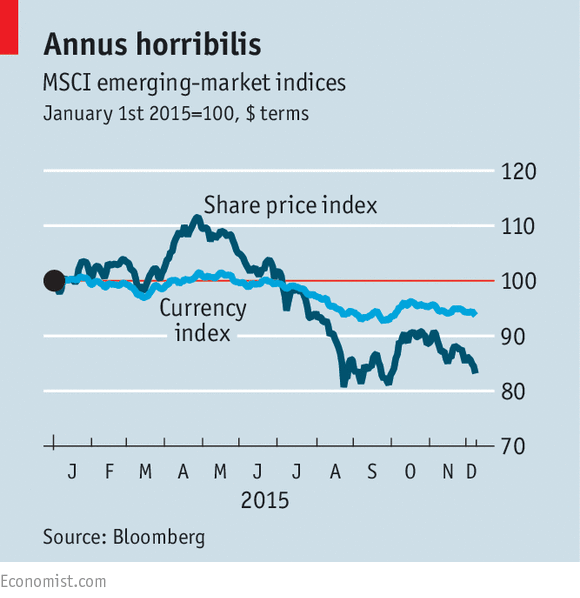

A decade of furious growth had dimmed those memories, but this year has revived them. The MSCI index of emerging-market equities has fallen by 15% (see chart), badly underperforming developed markets and hitting its lowest level since the height of the financial crisis in 2008.

From this vantage, much of the downside from rising American rates appears to have been priced in already. Take two of the most battered currencies, the Malaysian ringgit and the Russian rouble. They are down by some 25% and 50%, respectively, over the past two years. A steadying of their value would make nominal corporate earnings in both countries look far healthier in dollar terms: other things being equal, they would go from double-digit falls to being flattish. Jonathan Anderson of Emerging Advisors forecasts that the big theme of 2016 will be a “stabilisation trade”, as portfolio investors are lured back to developing countries.

The International Monetary Fund sees a similar trajectory for economies as a whole. It forecasts that emerging-market growth will average 4.5% next year, up from 3.9% this year, breaking a streak of five straight years of decelerating growth. It is not that emerging markets will have suddenly regained their lustre. Rather, it is that recessions will be less severe, if not over, in places like Brazil and Russia.

Yet if the best that can be said about emerging markets is that they will stabilise, this points to a more troubling reason for their relative indifference: the realisation that the Fed is the least of their problems.

In 2013, investors dumped emerging-market assets when America signalled the beginning of the end of its programme of quantitative easing. That episode came to be known as the “taper tantrum”. This time the gloom that envelops emerging markets might be more accurately described as a “secular sulk”.

The fear is that a golden era of growth, fuelled by China’s ravenous appetite for commodities, has come to a close, exposing deep cracks in their economic foundations. David Lubin of Citigroup, a bank, talks of a “broken growth model”. Governments cannot stimulate their economies because their creditors will not tolerate big deficits. Companies are also unable or unwilling to invest more because they have built up big debts. Exports are of little help because many of these economies are now overly reliant on commodities.

The feeble state of manufacturing across emerging markets, with the exception of parts of Asia, means that many will miss out on the one big upside to lift-off. The Fed is set to raise rates because of America’s relative economic strength. America, in turn, should provide a boost to countries that make the things it wants to buy.

But emerging markets such as Indonesia and South Africa that specialise in commodities have not just been hit hardest by China’s slowdown; they are also the least likely to benefit from America’s growth. To them, lift-off will sound like a cruel joke. They will stay pinned to the ground.

0 comments:

Publicar un comentario