Gold Weekly: An Ineluctable Rally On The Horizon

- Bearish sentiment hit an all-time high as of December 15.

- ETF bought gold at a strong pace in the week ending December 18, reflecting a positive swing in sentiment.

- Macro environment may become less bearish for commodities; a rally is still in the cards.

- We are constructive on gold prices over a one- to three-month horizon.

Buddha

Every week, I closely monitor the net speculative positions on the COMEX as well as the ETF holdings inasmuch as the historical economic behavior of gold prices suggests that, over a short-term horizon (<3 months), gold prices are largely influenced by changes in the forward fundamentals, reflected in changes in net spec length and ETF holdings.

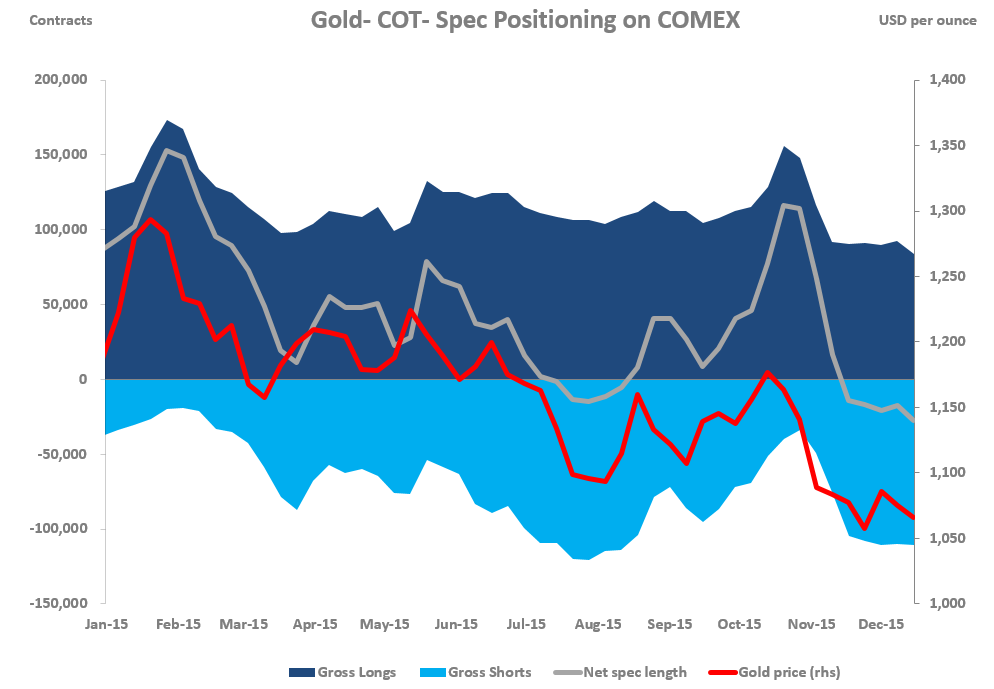

Speculative Positioning

Source: CFTC

According to the latest Commitment of Traders report provided by the CFTC, money managers, viewed as a relevant proxy for speculators, raised their net short fund position in the week ending December 8 while spot gold prices were down 1.36 percent over the period covered by the data (December 8-15).

The net short fund position rose 9,797 contracts to 27,219 contracts from 17,422 during December 8-15. This is the largest net short fund position since the CFTC started to report its statistics. In other words, the bearish sentiment toward gold has reached a new all-time high. This was largely attributable to long liquidation (-8,871 contracts) and reinforced by a tepid reengagement of shorts (+926 contracts).

The net spec length, which is in short territory for the fifth consecutive week, is now down 131 percent on the year. Contrary to our expectations, the spec positioning has not gradually improved despite the fact that the futures market is clearly overstretched on the short side. We believe that longs became increasingly nervous ahead of the conclusion of the FOMC meeting and preferred to close out their positions accordingly.

But given that the Fed has now started the process of its monetary policy normalization without inducing a resurgence of volatility due to its transparent communication, longs could rebuild their position in the weeks ahead. At the same time, gross shorts remain at a high level judging by the historical standards, which raises the likelihood of short-covering.

Looking ahead, we expect the spec positioning to gradually improve, acknowledging that gross shorts, up 170 percent on the year, are too extended. But as we documented recently, we cannot exclude the possibility that gold prices experience renewed weakness from current price levels despite an improvement in spec positioning. Indeed, our analysis of spec positioning suggests that gold prices can continue to depreciate despite an initial improvement in spec positioning before eventually rallying as it was the case around the end of 2013.

Investment Positioning

Source: FastMarkets

ETF investors bought gold for the first time in seven weeks as of December 18, pushing the total ETF holdings to 1,493 tonnes.

Gold ETF holdings rose 13 tonnes during December 11-18, marking the largest weekly increase since February 2015. But the buying was concentrated on December 18, via the SPDR. Indeed, according to FastMarkets' estimations, ETF investors sold six tonnes of gold between Monday 14 and Thursday 17 before buying 19 tonnes on Friday.

Similarly to speculators' behaviour, we believe that tactical investors became extremely nervous ahead of the Fed's decision and decided to liquidate their holdings accordingly, before realizing that the Fed's well-telegraphed decision to raise the federal funds rate target by only 25 basis did not provoke a catastrophic sell-off in gold prices (contrary to some analysts' expectations), and as such, some bargain hunting at current price levels could be a rewarding long-term strategy.

As we correctly anticipated last week, the FOMC would send an extremely dovish message to investors to avert any financial turbulence. Apart from the bond carnage in the high-yield space, which incidentally started weeks before the December liftoff, the financial markets were broadly stable.

Looking ahead, we continue to expect gradual ETF inflows over the next few weeks, reflecting a less bearish macro environment as investors will now increasingly pay attention to the speed of monetary policy normalisation. And the combination of lower oil prices, EM currency weakness, and the broad-based decline in commodity prices could lead investors to view the expected federal funds rate-rise path for 2016 as more gradual than they had initially envisaged. Against such a backdrop, we would expect a lower dollar combined with stable US real interest rates, which would then prompt investors to temper their negative outlook on gold prices, we think.

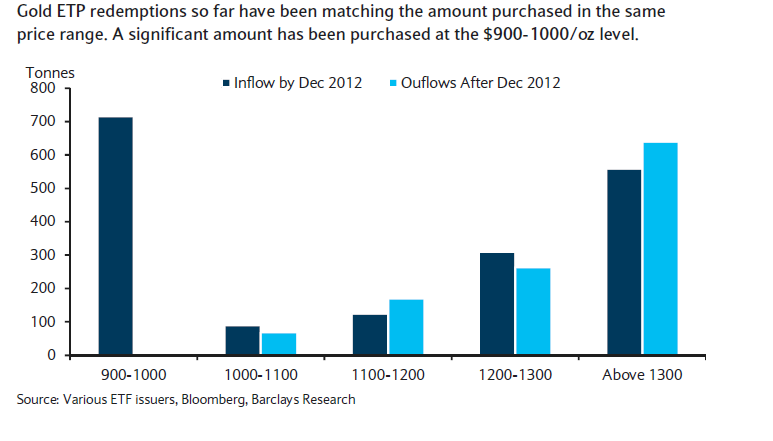

There is, however, a risk to our scenario, as we documented in our previous reports. According to data collected by Barclays, ETF investors who bought gold ETF shares prior to 2012 tend to sell their shares when their positions start to show a loss. So far, data show that investors who bought gold ETF shares above the $1,000 per ounce level until 2012 have liquidated most of their holdings since then. Given that a large block of ETF shares was purchased in the $900-1,000 range, totaling about 716 tonnes, according to their estimations, there is a risk to witness a strong liquidation of gold ETF holdings if gold prices should fall below this price range.

Spec Positioning Vs. Investment Positioning

Source: Mikz Economics

My GLD Positioning - Weekly Chart

Source: TradingView

Last week, we said, "our sentiment is that the SPDR Gold Trust ETF (NYSEARCA:GLD) will retest the $100 level and maybe break slightly below it before rallying sharply". In line with our anticipations, GLD made a low of $100.19 last week.

The bottoming-out process, which seems to have started since late November, is taking more time than we initially expected. Our spec positioning analysis suggested that a gradual improvement was on the horizon, but the latest CFTC statistics proved us wrong. Our ETF analysis, which pointed to progressive inflows, proved correct, though.

Looking ahead, we expect GLD to continue to form a base before rallying sharply. As a result, although it would be tempted to initiate a long GLD position from current price levels ($103.18 at the time of the writing), we prefer to await an improvement in spec positioning before making a bet. We would not be surprised to see a retest of $100 on a daily basis. But we acknowledge that the recent market action suggests that the $100 level is a solid support in so far as it was tested several times without being penetrated.

To sum up, we continue view the short-term risks to gold prices over a one to three-month horizon increasingly skewed to the upside. But we would be inclined to wait a little further before playing GLD from the long side.

0 comments:

Publicar un comentario