Fed Policy: Unsafe At Any Speed?

- The Fed took the bait.

- Fed Chair Janet Yellen recently penned a response to an open letter from political activist Ralph Nader.

- It was a notable exchange to say the least that warrants a closer review.

A notable exchange to say the least that warrants a closer review, particularly the response from Chair Yellen.

Before even considering the content of Chair Yellen's reply, it is worth it to question the following.

Why exactly is Ms. Yellen and/or her staff spending the time crafting a response to Mr. Nader's letter anyway? It would be one thing if Ms. Yellen was a financial blogger or Mr. Nader's elected representative, but she is the Chair of the U.S. Federal Reserve. Whether I agree or disagree with the content of Mr. Nader's letter, it seems that her and her staff's resources could be better spent on other endeavors. Sure, the transparency and consideration to respond to such letters is certainly appreciated, but where now is the line drawn. Will she be responding to trolls next?

One of the issues associated with Chair Yellen submitting a signed open letter response to Mr. Nader is that it leaves her reply subject to critique. And to this point I am inclined to provide some selected observations.

First, Ms. Yellen concedes the fact that at least some savers have suffered hardship at the expense of the Fed's monetary policy since the outbreak of the financial crisis more than seven years ago. The justification for the zero interest rate policy for so many years has been the emphasis on restoring the economy to prosperity so that it can support higher returns. I agree completely with the intent, but it immediately raises an important question. Is a wait of more than seven years and counting an acceptable length of time for savers still suffering at the hands of Fed policy to wait for the economy to restore itself to prosperity. After all, for many retirees, seven years represents a meaningful portion of an individuals life span in retirement. Yes, zero interest rate policy has been the Fed's dogged solution, but is it not reasonable to consider whether a different policy approach might have returned our economy to prosperity more quickly?

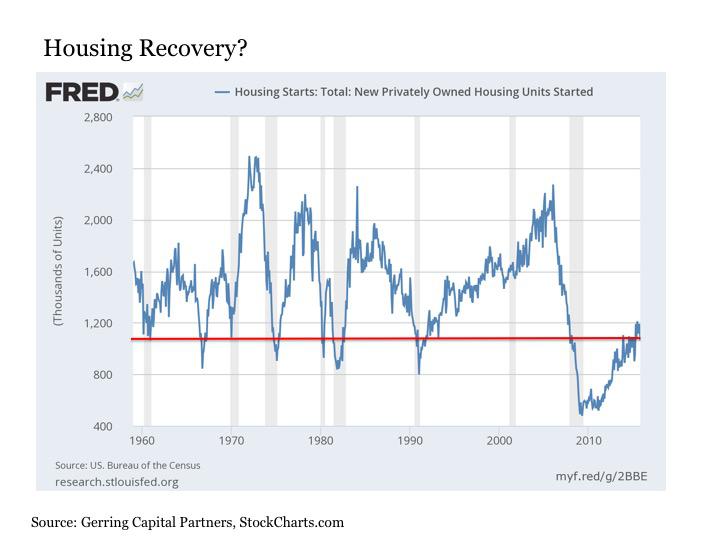

Ms. Yellen continues in her letter by reviewing the state of the economy in the immediate aftermath of the financial crisis. Indeed, the unemployment rate did rise to a peak of 10% by October 2009 and has been falling ever since. And yes, resulting lower mortgage rates have provided support to a housing market that was left decimated by the housing bubble that was left unchecked by this same monetary policy institution in the years leading up to the crisis.

That is, of course, for those lenders in the post crisis period that were actually able to qualify for the loans at these lower mortgage rates. And while home prices have recovered, they remain -13% below the levels from nearly a decade ago in early 2006. As for the housing market itself, it's recovery over the last seven years has brought it back to levels today that would have represented cyclical lows during past housing market downturns. Hardly anything to build an open letter victory lap around.

(click to enlarge)

The more dubious statement from Ms. Yellen comes at the end of her second paragraph:

"Americans generally have benefited, most particularly lower- and middle-income people affected disproportionately during the downturn."

This particular comment raised an eyebrow.

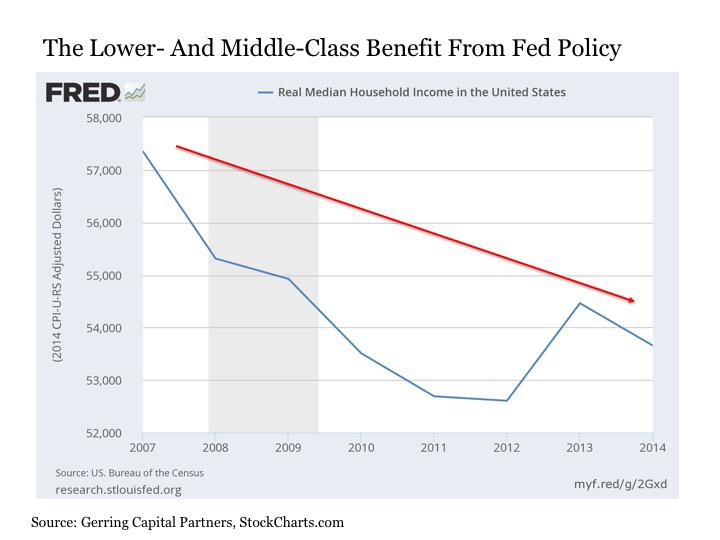

First, to suggest that lower- and middle-income people have been the primary beneficiaries of the Fed's zero interest rate policy since the financial crisis is disingenuous at best. One has to look no further than real median household income in the United States since the outbreak of the financial crisis to see that the average American have not necessarily thrived under the current monetary policy regime and that an alternative approach might have served them better.

(click to enlarge)

Also, it has clearly been by Chair Yellen's own admission the highest income individuals that have benefited most from the Fed's zero interest rate policy since the financial crisis. For example, during a speech on economic opportunity and inequality sponsored by the Federal Reserve Bank of Boston just over a year ago on October 18, 2014, Ms. Yellen openly and candidly lamented how "the past several decades have seen the most sustained rise in inequality since the 19th century" and that "by some estimates, income and wealth inequality are near their highest levels in the past hundred years, much higher than the average during that time span and probably higher than for much of American history before then." And she also cited during this same speech the stock market as a primary culprit for this widening inequality gap, particularly since the outbreak of the financial crisis. With all of this in mind, how is it then that lower- and middle-income Americans have particularly benefited from the Fed's zero interest rate policy when the income and wealth inequality gap are near their highest levels in the past century caused by a soaring stock market?

But it is in her next paragraph from her reply letter where arguably the most important points for scrutiny are raised. In the letter, Ms. Yellen raises the following:

"Would savers have been better off if the Federal Reserve had not acted as forcefully as it did and had maintained a higher level of short-term interest rates, including rates paid to savers? I don't believe so. Unemployment would have risen to even higher levels, home prices would have collapsed further, even more businesses and individuals would have faced bankruptcy and foreclosure, and the stock market would not have recovered."

Ms. Yellen's point here is notably imperceptive and in my view completely misses the point as to why so many Americans that follow the Federal Reserve are disgruntled with how the Fed has managed monetary policy in the post crisis period. I would contend that most are in full agreement with the Fed's swift policy response to the financial crisis in late 2008 and early 2009.

From my own perspective, I not only fully agreed with the Fed's implementation of what is now known as QE1 and the alphabet soup of special programs that were implemented at the time, but I would go so far as to credit the Fed with saving the global economy from total collapse. So in this regard, I completely agree with Ms. Yellen that the Fed was correct to have acted as forcefully as they did at the time. But this is not the argument.

Instead, at issue is how the Fed has managed monetary policy in the years since they succeeded in pulling the global economy back from the abyss. For when the Fed launched into these extraordinarily aggressive policy responses to the financial crisis back in late 2008 and early 2009, they did so with the following explanation. The Fed first needed to stabilize the financial system, and once it did it would move to slowly dismantle the too big to fail financial institutions as well as determine what the appropriate penalties would be on those bad actors that caused the financial crisis. So in short, the objections to the Fed's response to the financial crisis is not what was done in response to the crisis, but instead what has been done since the crisis.

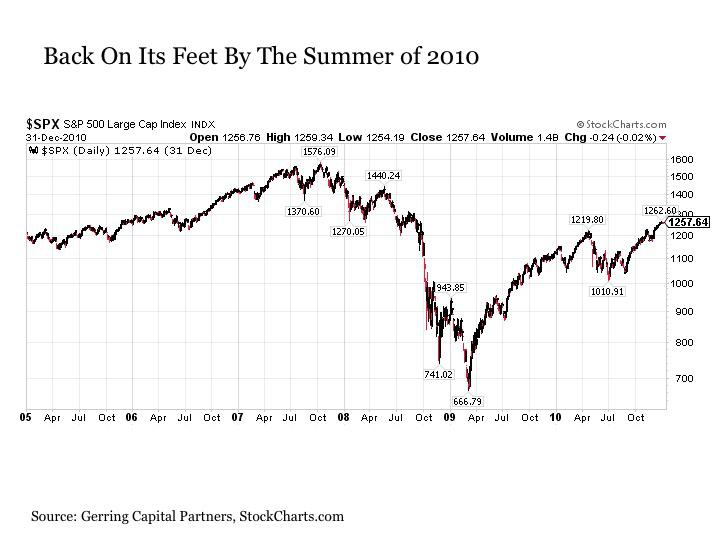

(click to enlarge)

By the summer of 2010, the Fed had succeeded in pulling the global economy back from the brink. Was it perfect? No, but one should not expect conditions in a capitalist system to be perfect and rosy at all points in time. But by the Fed's own beloved metric in the U.S. stock market, the S&P 500 Index (NYSEARCA:SPY) had been returned to 2005-2006 levels just prior to the 2007 peaks. The Fed's quantitative easing program had drawn to a close and presumably the markets would be left to stand on their own and undergo a much needed cleansing phase to wash the excesses that had been built up during the housing bubble from the financial system in a controlled and orderly way. After all, this is what the Fed had promised us when they engaged in their great rescue plan only 18 months earlier.

Also, this would have been the time to begin contemplating how the bad actors would be penalized for nearly breaking the global financial system with their absurdly reckless behavior during the housing bubble.

But the second part of the bargain is not what we received from the Fed. Instead, the Fed did the total opposite. Instead of allowing the economy to cleanse, addressing the structural problems associated with these large at risk financial institutions, and moving to punish bad actors, the Fed instead decided to pour on more with the launch of QE2 in the second half of 2010. And in the years since, the Fed has piled on more and more and more stimulus despite the fact that the Fed had already essentially stabilized the economy so many years before.

And it is to this point where the dissent against the Fed is sourced for so many. For by continuing their zero interest rate policy for more than five years longer than arguably necessary, they have essentially created a brand new crisis threat by encouraging the same undue speculation and risk taking that led to the bursting of the technology bubble and the housing market collapse related financial crisis over the past decade and a half. And the Fed has done so at the expense of the savers that have been repeatedly told to wait and absorb the near zero interest rates on their savings for so many years to encourage this same speculative behavior once again. Fool us once, fool us twice, but fool us three times?

I applaud Ms. Yellen and the Fed for their priority to use monetary policy to foster economic expansion and stable prices. And I commend Ms. Yellen in particular for her progress in directing monetary policy from the beginning of QE3 tapering nearly two years ago to the point where the Fed is considering raising interest rates as soon as next month. But if it turns out after one or two rate increases that the Fed is forced by the economy to reverse course on policy, it is my hope that they will consider policy prescriptions other than lowering rates back to zero and engaging in yet another round of QE4 asset purchases. For while QE1 and its associated programs did splendidly in rescuing the global financial system, the efficacy of the various stimulus programs that have followed are far less clear. In fact, it could be argued that these post 2010 programs have proven more detrimental than helpful to the economy and the financial system.

So while QE and zero interest rates may be great for rescuing an economy, it may not be the best approach for generating a robust sustained recovery. Decades of experience in Japan provide evidence to this latter point. And after seven years now of following the same script with an economy that remains sluggish at best, perhaps at minimum the consideration of a new and decidedly different monetary policy approach to the problem may finally be warranted.

0 comments:

Publicar un comentario