The Only Solution To The U.S. Treasury's Debt Crisis

Peter Knight

- There are some very big holes in the idea the US can’t raise interest rates and the impact it would have on the US economy.

- Desperate depositors looking for interest income have been sucked into the long end of the curve, enabling the US Treasury to fix its debt service costs at 2.37% until 2026.

- I see higher short-term rates, more quantitative easing, dollar devaluation, and US debt monetization on deck.

- Long-term U.S. dollar devaluation will fuel all investments backed by tangible assets or a bonafide income flow higher over the next 48 months.

.

Source Federal Reserve.

Source Federal Reserve.Without Fed QE, US rates will rise, as there is no one to replace the Fed in buying $30 billion to $100 billion per month of US Treasuries at non-competitive rates on the open market to fund US deficit spending.

Higher rates, more QE, or both?

The Fed's US economic numbers post "economic stimulus" are the worst in US history. They certainly do not support the representation that the US economy is in recovery. What they do show is that "economic stimulus" for the US taxpayer and economy was the most costly policy failure in US history.

Over the last 7 years of emergency and temporary rate cuts, the Fed has enabled the US Treasury to suck in desperate depositors, looking for any interest income at all, into the long end of the curve.

Currently the average duration for US Treasury debt is a little over 10 years with an average yield of 2.37% or the debt service cost for the US on the current $18.1 trillion in debt is fixed at 430 billion per year through 2026.

Source: Treasury direct.

Had the US Treasury not refinanced their debt and fixed it for 10+ years at 2.37% each 1.00% increase in rates would consume 10% of total US tax receipts ($181 billion per 1.00%).

Considering the US national debt during "economic stimulus" has risen 93% while tax rece

ipts were up only 28%, this would be more than problematic for the US Treasury.

Source: Federal Reserve.

Source: Federal Reserve.Now that the current 18.1 trillion in debt has been locked in at 2.37% through 2026 the Fed can raise rates without the US Treasury worrying about their debt service cost consuming the majority of all tax receipts if and when rates "normalize." The Fed can raise rates going into the US November 2016 election in the name of "economic recovery."

All debt instruments, stocks with high debt loads, precious metals and energy I believe will move lower in the short term. The move lower will accelerate as foreign liquidation of US debt and dollars engage.

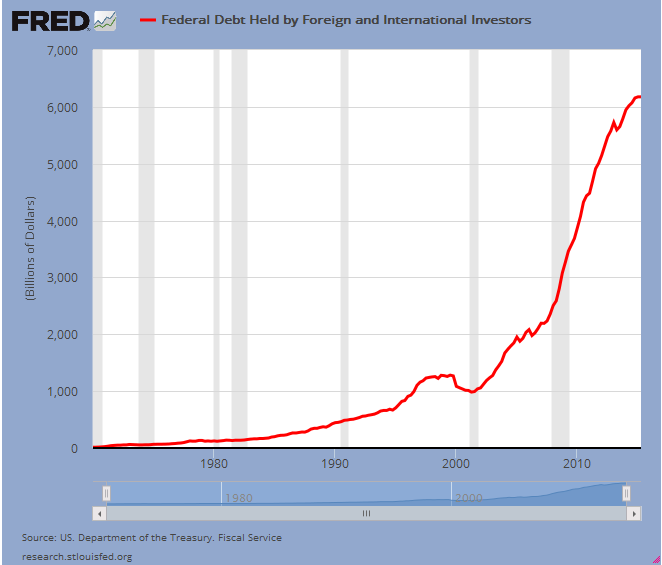

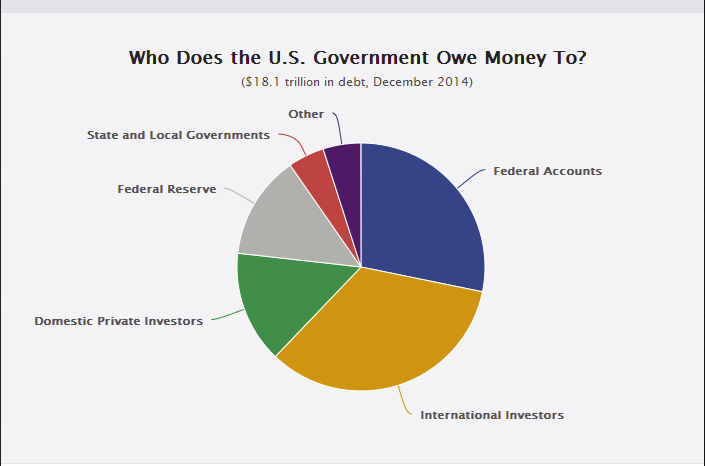

Currently there is $6 trillion of US Treasury debt owned by non-US investors. Currency and instrument risk for these non-US investors is more in one day than annual yields.

US Treasury debt held by Non-US investors:

Source: Federal Reserve.

Source: Federal Reserve.Non-US investors currently own nearly twice the amount of US Treasuries as domestic private investors. Does this look right to you?

For non-US investors there is very limited upside potential with debt instrument prices coming off all time highs as rates begin to rise.

A 30-year, $100,000 face value Treasury bond has lost more than $12,000 at the current annual yield of 3.11%:

10-year $100,000 face value Treasury notes have lost nearly $10,000 at their current annual yield of 2.34%:

5-year $100,000 face value Treasury notes have lost over $6,000, with current annual yield of 1.74%:

The dollar is shaky at best, near its 10-year high:

Non-US investors also hold trillions more in non US Treasury debt with these instruments having the same or greater risk.

No alternative to US debt and dollars?

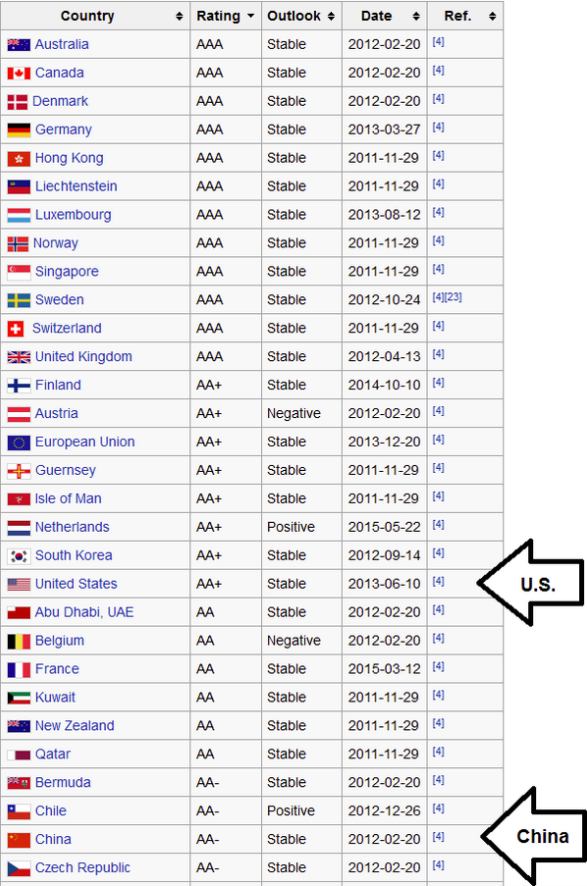

Think again, 12 countries currently have higher credit ratings than the US; the majority of these countries have the same or higher rates with greater currency appreciation potential.

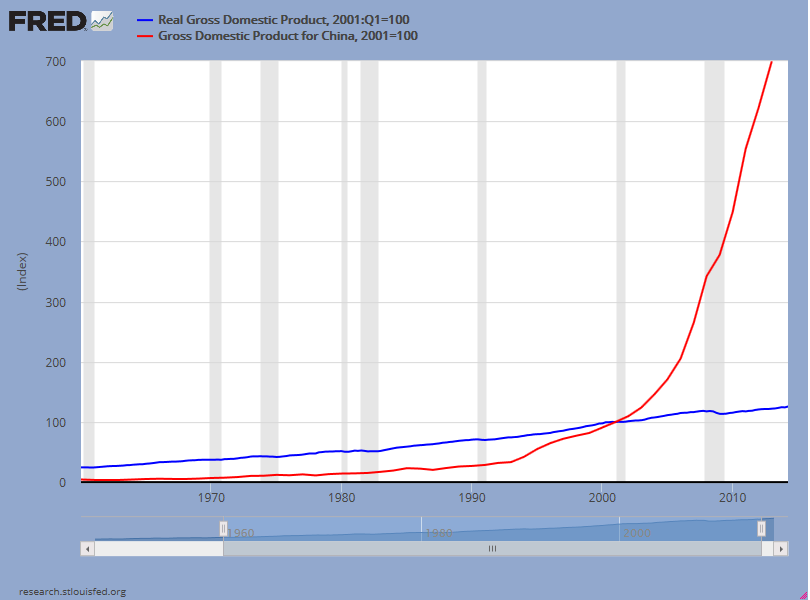

Lower-grade alternatives like China, the world's second largest economy, also offer an alternative to US debt and dollars.

China's GDP is a little less than 7%, and they are lowering rates, fearing a economic slowdown.

The US's GDP is less than 3%, and they are raising rates because of economic recovery -- does this sound right to you?

China's current growth rate -- more than twice the US's over the next decade -- could jeopardize the US's status as the world's largest economy. The inclusion of the renminbi as a world reserve currency could also motivate Asian and other investors out of the USD and into the Chinese renminbi.

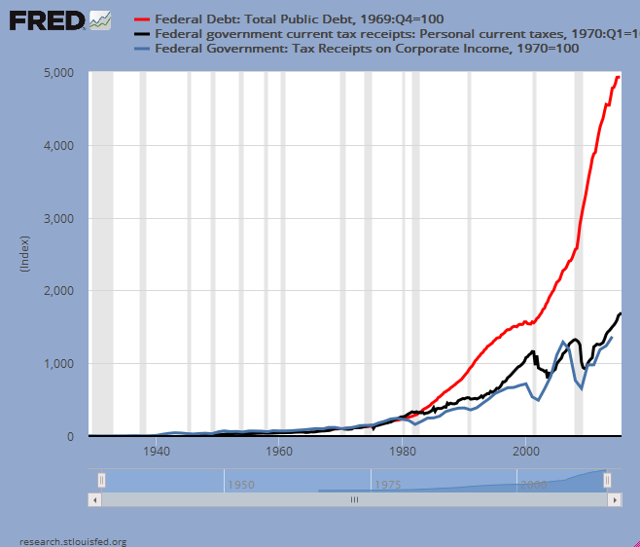

By the Fed's numbers

US versus China - growth:

Source: Federal Reserve.

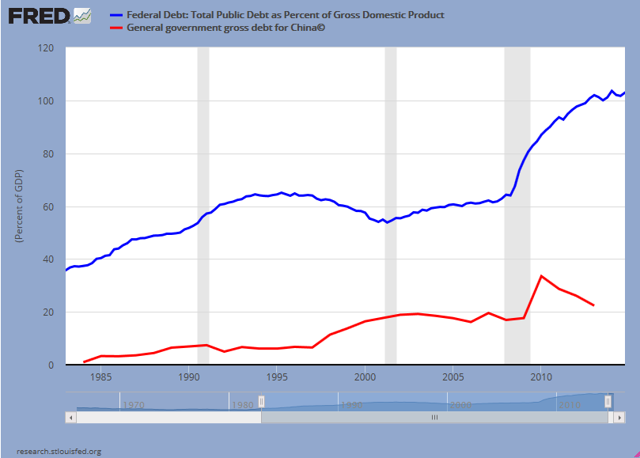

Source: Federal Reserve.US versus China - debt-to-GDP ratio:

Source: Federal Reserve.

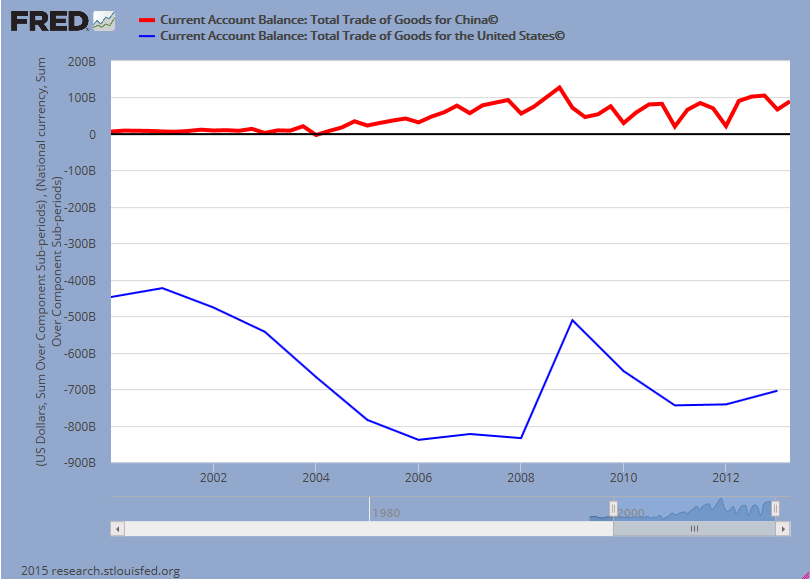

US versus China's - trade surplus/deficit:

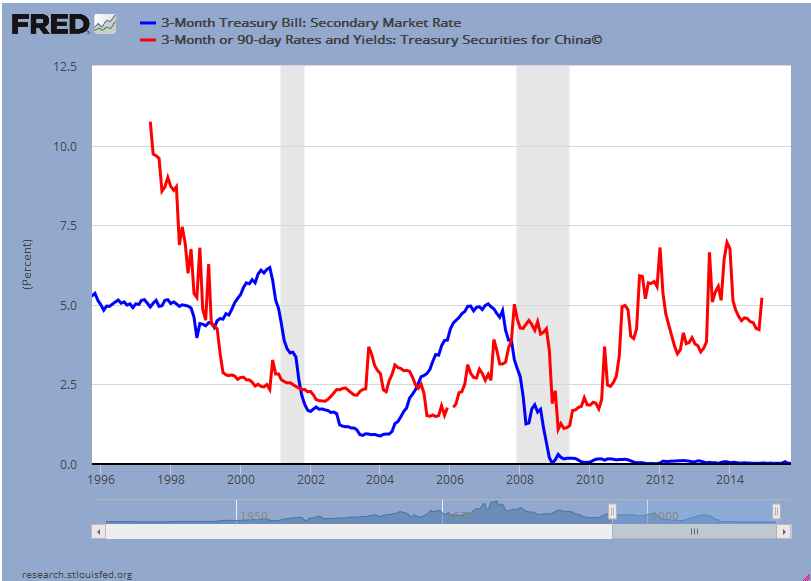

US versus China - 3-month rates (this spread has narrowed with China's rate reduction, and the Fed has not yet updated the data):

Source: Federal Reserve.

Source: Federal Reserve.As the major long term trends for US debt instruments change from up to down trends I believe non US investors will start aggressively selling US debt instruments accelerating the downward move caused by the expectation of and the eventual US rate hikes.

Next I see these investors aggressively selling US dollars reversing the shaky uptrend to down.

Currently I can't see anything or anyone capable of stepping in front of this multi trillion dollar selloff aside from the Fed.

For many non investors they'll not only liquidate longs but create net new shorts to capture the move lower in US debt instruments and the USD.

No liquidity to hedge or liquidate?

Think again the US 3 month rate contract traded at the Chicago Mercantile Exchange by itself currently trades a face value of over 2 trillion dollars per day, open interest for futures and options contracts on the 3 month rate contract now exceeds 20 trillion in face value, there are an additional 30 interest rate futures contracts on this exchange alone that trade trillions more.

Trillions more traded daily in the USD through the forex market making the exodus from the USD painless for non US investors.

The short term the move down I believe will get ugly and is why I have been recommending using "collars" to define risk on all trades and for the duration of all trading periods.

If the "correction" that I'm anticipating occurs the Fed will have the justification they need to fire up the QE printing press with tenacity.

The Fed's excuse will be "defending" the US dollar and to protect the "integrity" of the US financial system/markets from non US sales of US assets.

With trillions more dollars eventually created and pumped into circulation chasing after the same amounts of goods and services US inflation will engage.

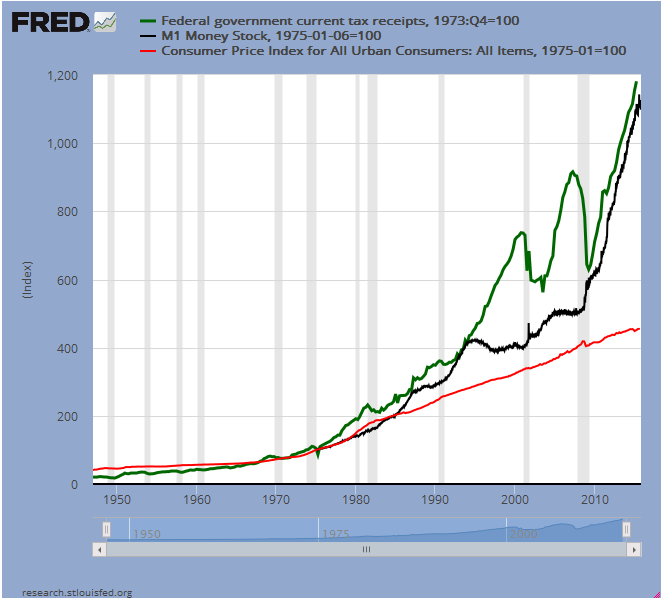

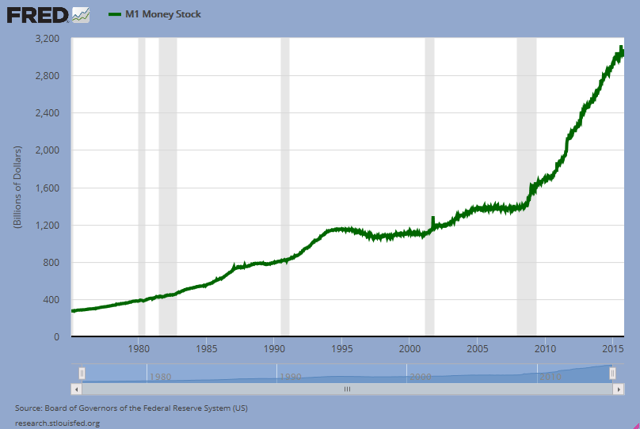

When the prices of goods and services rise so do tax receipts. The chart below shows the 50 year correlation between M1 (money supply) and tax receipts.

Source: Federal Reserve.

Source: Federal Reserve.Let's keep it simple and assume between now and the end of 2022 the Fed increases M1 by trillions more using "quantitative easing" cutting the actual buying power of the USD in half.

The prices of goods and services could double, with these price increases tax receipts could double as well moving them from the current 1.8 trillion to 3.6 trillion annually. This long-term trend already in place will continue.

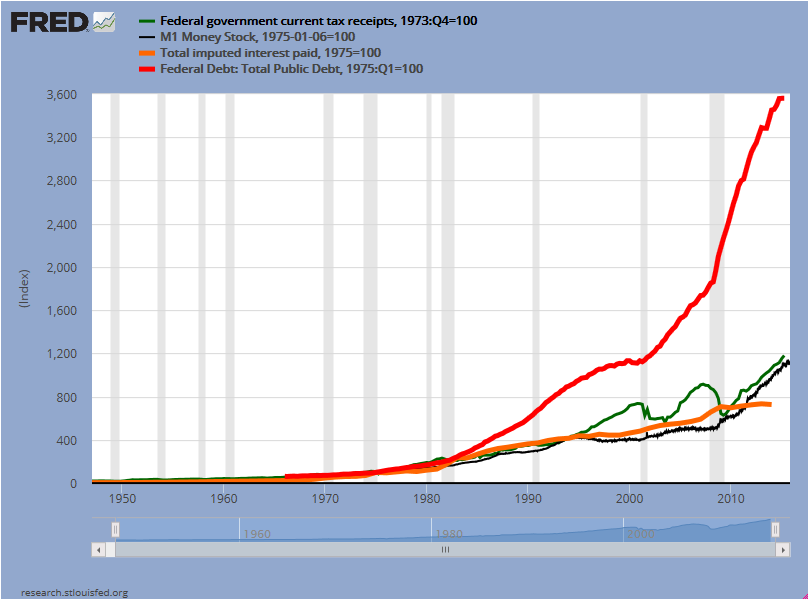

US debt in red, debt service cost in orange, tax receipts in green and M1 in black:

Source: Federal Reserve.

Source: Federal Reserve.Facts

Debt service cost has been fixed at 2.37% through 2026 at 430 billion annually.

The US treasury through inflation could potentially increase tax receipts from 1.8 trillion to 3.6 trillion annually.

The US Treasury will then have twice the tax receipts to service the same 430 billion in annual fixed debt service cost on the current 18.1 trillion in US debt.

Problem solved

It's called monetization and it's been around since the first fiat currency was introduced by China in 1,000 AD.

Bernanke has had this plan in place long before he or Yellen became Fed chair or the so-called Great Recession began.

In his November 21, 2002, speech entitled Deflation: Making Sure It Doesn't Happen Here, Bernanke provides information on his plan, reasons for US debt monetization is the solution and why deflation cannot occur for any country that uses a "fiat" currency:

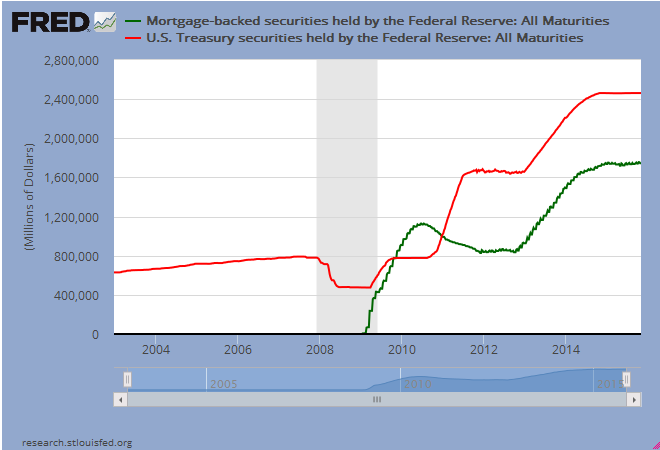

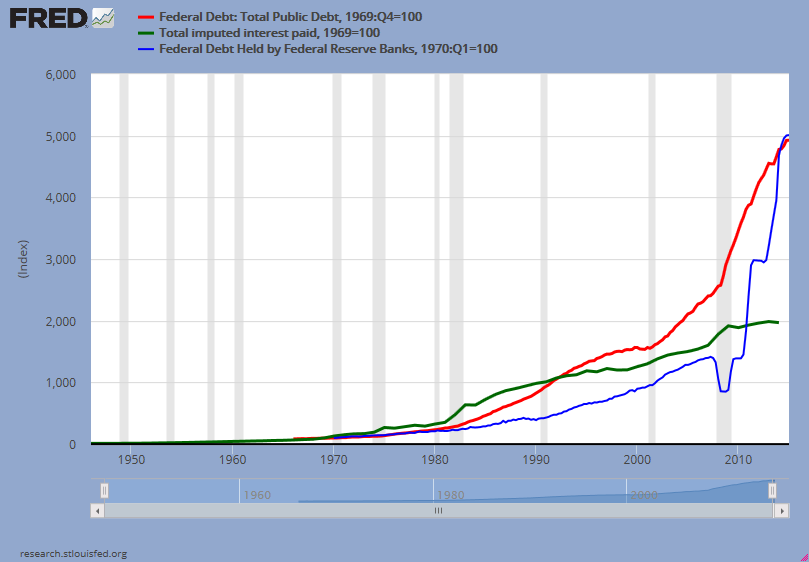

U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.Through quantitative easing, Bernanke led the Federal Reserve in creating $4.216 trillion backed by no tangible asset or income flow to buy US debt at non competitive rates to force and hold rates lower and for longer than any other period in history including the great depression.

Federal debt red, Federal debt purchased by the Fed blue, US debt service cost green:

Source: Federal Reserve.

Source: Federal Reserve.I believe as rates rise and the Treasury still can't sell what it needs on the open market to satisfy it's debt fix it will provide the Fed the excuse they need to continue more QE after the original hemorrhage is cauterized.

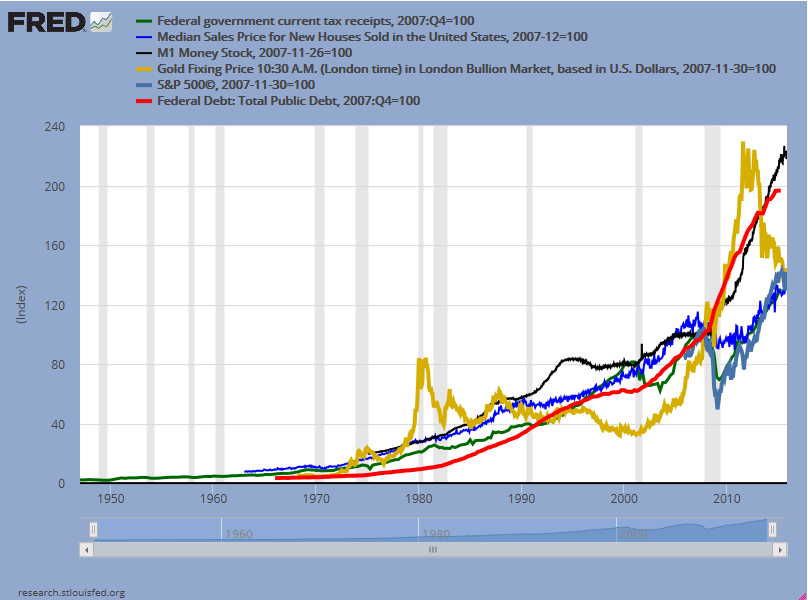

Long term US dollar devaluation will continue to fuel all investments backed by tangible assets or a bonafide income flow higher against the USD until tax receipts are high enough to let rates normalize.

Source: Federal Reserve.

Source: Federal Reserve.Get ready for higher volatility, more QE, and inflation

Stay with quality stocks in companies that have built high cash buffers and know how to manage them. Examples include:

- Apple (NASDAQ:AAPL)

- Microsoft (NASDAQ:MSFT)

- Alphabet ([[GOOG]], [[GOOGL]])

- Pfizer (NYSE:PFE)

- Cisco (NASDAQ:CSCO)

- Goldman Sachs (NYSE:GS)

- Moody's (NYSE:MCO)

- Oracle (NYSE:ORCL)

- AT&T (NYSE:T)

- AbbVie (NYSE:ABBV)

- JPMorgan Chase (NYSE:JPM)

- GLD (SPDR Gold Trust)

- IAU (COMEX Gold Trust)

- SGOL (Physical Swiss Gold Shares)

- DGL (DB Gold Fund)

- DGP (DB Gold Double Long ETN)

- GLL (UltraShort Gold)

- OUNZ (Gold Trust)

- UGL (Ultra Gold)

- DZZ (DB Gold Double Short ETN)

- UGLD (3x Long Gold ETN)

- DGZ (DB Gold Short ETN)

- DGLD (3x Inverse Gold ETN)

- GYEN (Gartman Gold/Yen ETF)

- GEUR (Gartman Gold/Euro ETF)

- UBG (E-TRACS UBS Bloomberg CMCI Gold ETN)

- GLDI (X-Links Gold Shares Covered Call ETN)

0 comments:

Publicar un comentario