The Central Bankers' Death Wish

In fact, Europe is stranded in economic stagnation because statist dirigisme and the massive crush of welfare state taxation and finance have ground enterprise and productivity to a halt. But Draghi says it’s all China’s fault, and that he will fix their dereliction with even more monetary madness:

In fact, the so-called slowdown in China is the best thing that ever happened to Europe, as is the present spot of unusually low consumer inflation. And there is no mystery as to why these things are happening.

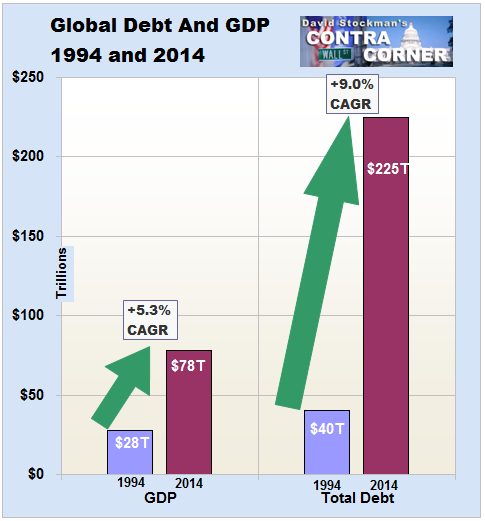

China and the rest of the world have just come through a mind-pending credit binge which took global debt from $40 trillion in 1994 to $225 trillion at present. China was in the forefront of that binge, sporting a 56X gain in outstanding credit during the same two decade period (from $500 billion in 1995 to $28 trillion at present).

The effect of that freakish $185 trillion debt eruption was a worldwide crack-up boom. It was initially manifested in a massive expansion of unsustainable debt financed consumption in the US and other DM economies and runaway fixed investment in China and the other EM economies which supply it.

Accordingly, much of the $40 trillion of global GDP growth shown in the chart reflected purchase money output, not sustainable organic gains in productivity and earned incomes.

Needless to say, purchase money GDP disappeared the instant that DM households could no longer tap their home ATM to spend borrowed money on restaurants and new kitchen countertops; and EM government and enterprises could no longer borrow to build uneconomic steel plants, empty luxury apartments or bridges that no one takes to anywhere.

What this crack-up boom cycle entailed then is a monumental, two-phase global deformation that lies at the heart of what Draghi was babbling about yesterday.

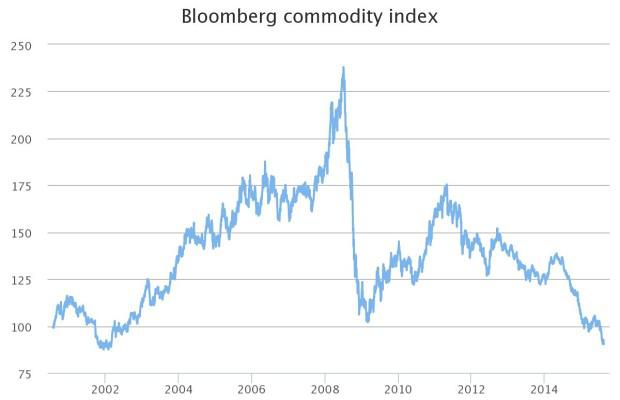

Initially, it led to a surge in global demand for energy, metals and other raw materials in excess of currently installed capacity, thereby fueling drastically higher commodity prices and periodic eruptions of consumer level inflation. Thus, oil went from $20 per barrel to a peak of $150 during the commodity inflation phase; and copper went from $1 to $4 per pound and iron ore from $30 per ton to $200.

Then, in the second phase of the global crack-up boom, drastic financial repression by the world’s central banks after the 2008 crisis led to massive over-investment and malinvestment in production capacity. This unprecedented CapEx boom ranged from the new iron ore mines of western Australia to the shale patches of the North Dakota Bakken to the excess steel and auto plants of China to the containership and bulk carrier capacities of the world’s shipping lines.

In fact, these massive additions of fixed capital and supply capacity throughout the global commodity/industrial complex are still coming on stream just as the leading age of the global credit Ponzi is coming to an abrupt halt in China. Accordingly, throughput volumes are faltering and are actually declining in many sectors, while the swelling availability of high fixed costs production facilities is leading to an unprecedented wave of wholesale price reduction.

The global crack-up boom cycle is evident in the Bloomberg commodity index, which has now plunged to below 2001 levels. Indeed, the area under the graph line tracks its two-phases almost perfectly- with the deflation phase incepting in 2012.

This huge global impulse of commodity inflation at first and now payback time of commodity deflation is being relentlessly transmitted down the supply chain. In the case of US producer prices for all commodities and for manufactured goods, respectively, the global cycle is plainly evident in the graph below.

Between 1995 and the May 2014 peak, US wholesale prices for all commodities rose by 70% or by 3% per annum. Likewise, the PPI for manufactured goods rose by 27% through early 2015.

However, both are now rolling over as the world’s deflationary payback phase gathers momentum and transmits down the price chain. The US wholesale index for all commodities is down by 9% and manufacturing goods by 1% since their respective peaks.

(click to enlarge)

Stated differently, the world has had its quota of consumer inflation and then some over the past two decades. Now it is payback time as the “excess supply” phase of the global crack-up boom supplants the “excess demand” phase.

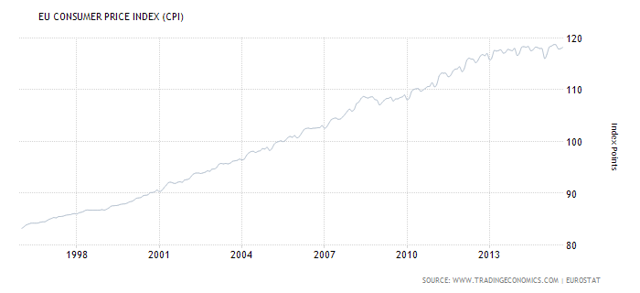

In that context, eurozone consumers are not being deprived of what central bankers apparently believe to be their God-given right to CPI inflation and the continuous erosion of the purchasing power of their wages. In fact, the eurozone consumer price index at 118.7 in September reflected a 2.1% per annum rate of gain since 1996.

(click to enlarge)

Do the mountebanks who run the ECB, along with the entire central bankers guild of the world, not believe that history has actually happened? Do they hold that NASA didn’t really land on the moon, as it were?

Do they think that there is some crank principle of economics that requires consumer inflation to be metered out in exactly 2.000% annualized rates every year, quarter, month and day?

Folks, Mario Draghi’s central banker view of consumer inflation is just brain dead ritual incantation.

Self-evidently, the rate of change does not need to be smooth as the skin on a baby’s butt for optimum economic performance.

In fact, 2% inflation is a purely religious proposition that is unrelated to the prosperity of main street; it is no more relevant to gains in real wealth than the rite of full immersion baptism.

Indeed, the 2% inflation meme is so threadbare that it needs to be called out for what it is. It’s a convenient cover for the radical usurpation of power undertaken by the world’s central bankers during the last two decades. And it survives only because it serves the interest of Wall Street gamblers and the world’s politicians and fiscal authorities alike.

The latter get to run up endless public debt because the central bankers buy it up under QE and drive the carry cost virtually to the zero bound. Likewise, the top 1% of financial gamblers cannot get enough of the 2% inflation hoax because it means free carry trade money as far as the eye can see.

In short, Europe, the US, Japan, China and most of the rest of the world is in thrall to a tiny coterie of power-hungry central bankers. If you do not think they are driving the financial system to the mother of all bubble crashes, just ponder the following justification by a top ECB authority for depriving eurozone consumers of even a brief spot of zero inflation in their cost of living:

So there is no alternative except to take cover because the latest stock market rip is based on pure central bank hopium

Indeed, Mario Draghi has confirmed once again that the world’s central bankers have a monetary death wish. Unlike the gamblers who bought Cramer’s top 49 stock picks, the best course of action is to sell, sell, sell- and do it now.

In a news conference, Mr. Draghi stressed the “downside risks” to both economic growth and inflation arising from slowing growth in China and other large developing economies, as well as weak commodity prices.These are the words of a slow-witted man who was born yesterday. That is, they evince an economic model that says every single year, month and day of prior history is irrelevant; and that regardless of how we got to the present moment the answer is always more heavy-handed central bank intrusion in the financial system in order to achieve an utterly bogus 2% inflation target.

In fact, the so-called slowdown in China is the best thing that ever happened to Europe, as is the present spot of unusually low consumer inflation. And there is no mystery as to why these things are happening.

China and the rest of the world have just come through a mind-pending credit binge which took global debt from $40 trillion in 1994 to $225 trillion at present. China was in the forefront of that binge, sporting a 56X gain in outstanding credit during the same two decade period (from $500 billion in 1995 to $28 trillion at present).

The effect of that freakish $185 trillion debt eruption was a worldwide crack-up boom. It was initially manifested in a massive expansion of unsustainable debt financed consumption in the US and other DM economies and runaway fixed investment in China and the other EM economies which supply it.

Accordingly, much of the $40 trillion of global GDP growth shown in the chart reflected purchase money output, not sustainable organic gains in productivity and earned incomes.

Needless to say, purchase money GDP disappeared the instant that DM households could no longer tap their home ATM to spend borrowed money on restaurants and new kitchen countertops; and EM government and enterprises could no longer borrow to build uneconomic steel plants, empty luxury apartments or bridges that no one takes to anywhere.

What this crack-up boom cycle entailed then is a monumental, two-phase global deformation that lies at the heart of what Draghi was babbling about yesterday.

Initially, it led to a surge in global demand for energy, metals and other raw materials in excess of currently installed capacity, thereby fueling drastically higher commodity prices and periodic eruptions of consumer level inflation. Thus, oil went from $20 per barrel to a peak of $150 during the commodity inflation phase; and copper went from $1 to $4 per pound and iron ore from $30 per ton to $200.

Then, in the second phase of the global crack-up boom, drastic financial repression by the world’s central banks after the 2008 crisis led to massive over-investment and malinvestment in production capacity. This unprecedented CapEx boom ranged from the new iron ore mines of western Australia to the shale patches of the North Dakota Bakken to the excess steel and auto plants of China to the containership and bulk carrier capacities of the world’s shipping lines.

In fact, these massive additions of fixed capital and supply capacity throughout the global commodity/industrial complex are still coming on stream just as the leading age of the global credit Ponzi is coming to an abrupt halt in China. Accordingly, throughput volumes are faltering and are actually declining in many sectors, while the swelling availability of high fixed costs production facilities is leading to an unprecedented wave of wholesale price reduction.

The global crack-up boom cycle is evident in the Bloomberg commodity index, which has now plunged to below 2001 levels. Indeed, the area under the graph line tracks its two-phases almost perfectly- with the deflation phase incepting in 2012.

This huge global impulse of commodity inflation at first and now payback time of commodity deflation is being relentlessly transmitted down the supply chain. In the case of US producer prices for all commodities and for manufactured goods, respectively, the global cycle is plainly evident in the graph below.

Between 1995 and the May 2014 peak, US wholesale prices for all commodities rose by 70% or by 3% per annum. Likewise, the PPI for manufactured goods rose by 27% through early 2015.

However, both are now rolling over as the world’s deflationary payback phase gathers momentum and transmits down the price chain. The US wholesale index for all commodities is down by 9% and manufacturing goods by 1% since their respective peaks.

(click to enlarge)

Stated differently, the world has had its quota of consumer inflation and then some over the past two decades. Now it is payback time as the “excess supply” phase of the global crack-up boom supplants the “excess demand” phase.

In that context, eurozone consumers are not being deprived of what central bankers apparently believe to be their God-given right to CPI inflation and the continuous erosion of the purchasing power of their wages. In fact, the eurozone consumer price index at 118.7 in September reflected a 2.1% per annum rate of gain since 1996.

(click to enlarge)

Do the mountebanks who run the ECB, along with the entire central bankers guild of the world, not believe that history has actually happened? Do they hold that NASA didn’t really land on the moon, as it were?

Do they think that there is some crank principle of economics that requires consumer inflation to be metered out in exactly 2.000% annualized rates every year, quarter, month and day?

Folks, Mario Draghi’s central banker view of consumer inflation is just brain dead ritual incantation.

Self-evidently, the rate of change does not need to be smooth as the skin on a baby’s butt for optimum economic performance.

In fact, 2% inflation is a purely religious proposition that is unrelated to the prosperity of main street; it is no more relevant to gains in real wealth than the rite of full immersion baptism.

Indeed, the 2% inflation meme is so threadbare that it needs to be called out for what it is. It’s a convenient cover for the radical usurpation of power undertaken by the world’s central bankers during the last two decades. And it survives only because it serves the interest of Wall Street gamblers and the world’s politicians and fiscal authorities alike.

The latter get to run up endless public debt because the central bankers buy it up under QE and drive the carry cost virtually to the zero bound. Likewise, the top 1% of financial gamblers cannot get enough of the 2% inflation hoax because it means free carry trade money as far as the eye can see.

In short, Europe, the US, Japan, China and most of the rest of the world is in thrall to a tiny coterie of power-hungry central bankers. If you do not think they are driving the financial system to the mother of all bubble crashes, just ponder the following justification by a top ECB authority for depriving eurozone consumers of even a brief spot of zero inflation in their cost of living:

At Thursday’s news conference, ECB Vice President Vítor Constâncio ticked off a litany of reasons why prolonged weak inflation, or sustained falls in prices known as deflation, worries central bankers and justifies the massive stimulus many have undertaken. Falling prices may cause consumers to put off purchases if they expect that trend to continue, he noted. It also raises the cost of servicing debt. In addition, he noted that official consumer price measures may overstate the extent of inflation.

For deflation to take hold, consumers and businesses would have to expect price falls to continue. Central bankers want to persuade households and financial markets that, whatever its current reading, the inflation rate will be around their target over the medium term, in which case they describe inflation expectations as being “anchored.”

Mr. Draghi warned of a possible “de-anchoring” of expectations if the inflation rate remains low for a long time, and particularly if oil prices fall further. “These risks have gone up and we want to be vigilant,” he said.This is just plain rubbish. These half-baked propositions would have received a falling grade in even a junior college introductory economics course just 20 years ago.

So there is no alternative except to take cover because the latest stock market rip is based on pure central bank hopium

Indeed, Mario Draghi has confirmed once again that the world’s central bankers have a monetary death wish. Unlike the gamblers who bought Cramer’s top 49 stock picks, the best course of action is to sell, sell, sell- and do it now.

0 comments:

Publicar un comentario