Deleveraging, QE, And Inflation

- The U.S. economy has gone through a household deleveraging and balance sheet recession that rendered conventional easing of monetary policy ineffective.

- Once the zero lower interest rate bound is reached, a central bank will resort to unconventional measures such as quantitative easing.

- Quantitative easing will prove inflationary as demand for credit increases. It will render the Fed's normal ability to tighten policy ineffective since reserves in the banking system are nearly unlimited.

- The Fed will have to sell securities in huge quantities to reverse the effect of quantitative easing.

That is typically how monetary policy functions. A deleveraging, where the zero lower bound on interest rates is already reached and demand for loans is still insufficient because debt to income ratios are too high and balance sheets need repair, renders traditional monetary policy ineffective. This has led to the widespread belief recently that a central bank is unable to create inflation (NYSEARCA:GLD). A central bank can create inflation the majority of the time during ordinary business cycles through decreasing interest rates and therefore driving demand for loans higher as credit becomes less expensive. The issue arises when debt to income ratios reach a point where people become focused on repayment of debt. There has to be sufficient net new lending for the economy and monetary system to function properly. Infinite expansion of loans is a requirement. The cure for a deleveraging is simply time. Balance sheets and debt to income ratios must be repaired before releveraging begins. This can take approximately a decade. A deleveraging happens approximately once in a generation and the last two in the United States were 1932 and 2009. For further reading on deleveragings I recommend the Bridgewater Associates documents, How The Economic Machine Works, and, An In Depth Look At Deleveragings.

So confronting insufficient demand for credit, the Federal Reserve resorted to unconventional monetary policies such as quantitative easing. Quantitative easing has multiple transmission mechanisms. First it provided massive liquidity to the banking system and flooded it with reserves. It also minimized long term yields, created financial asset price appreciation and effectively changed economic expectations. There are risks inherent in QE though, in the form of excessive inflation, which I see as a high probability scenario.

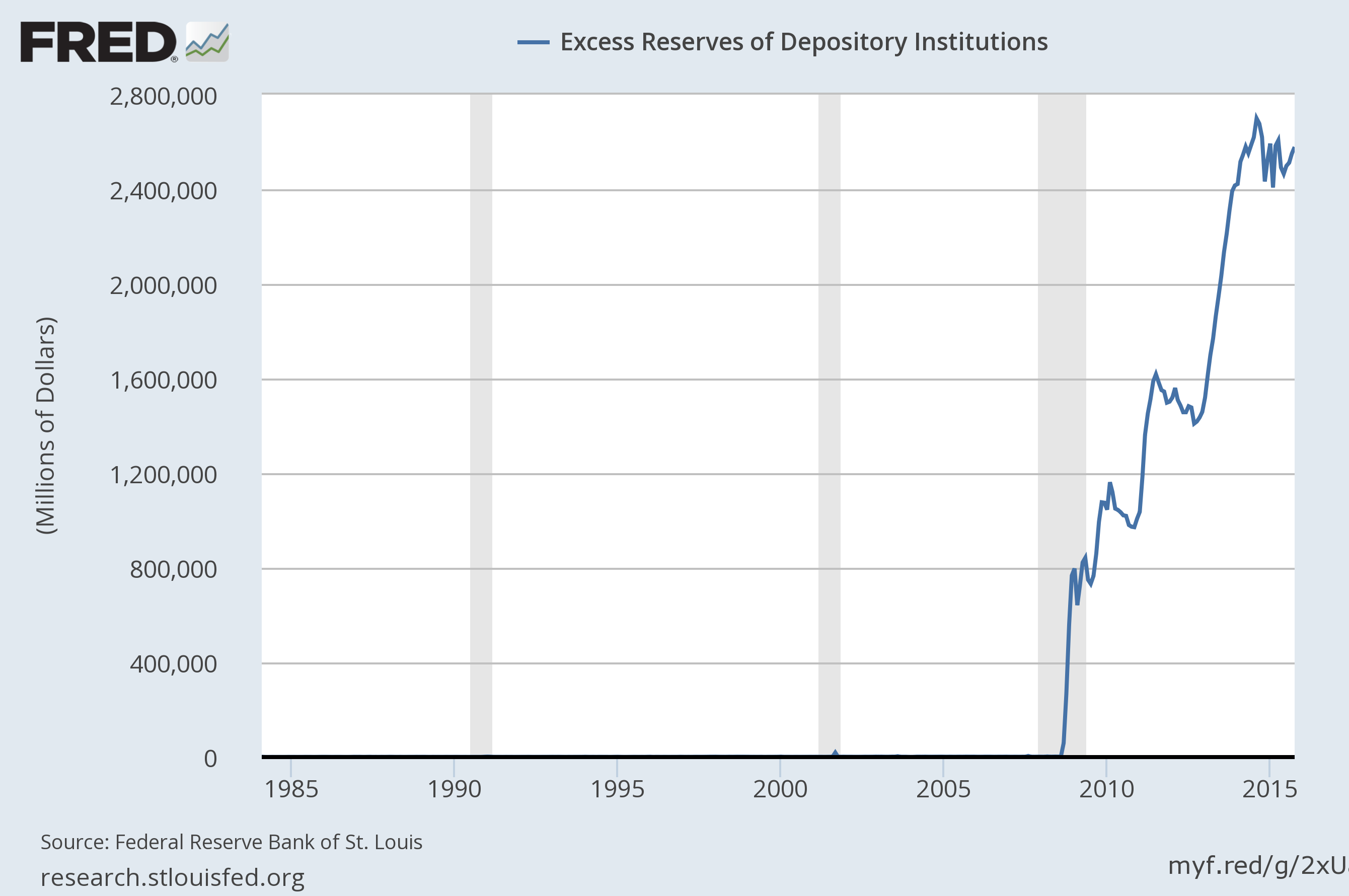

Just as a deleveraging rendered the easing effect of monetary policy ineffective, I believe QE will render the tightening mechanism ineffective as well. There are so many excess reserves in the banking system that when demand for credit begins increasing at a rate consistent with higher inflation the Fed will not have the ability to tighten effectively. Traditionally, a central bank would sell bonds draining reserves from the banking system. There are so many reserves right now that it would take an astronomical amount of securities selling and balance sheet contraction that would be detrimental to financial markets.

(click to enlarge)

The second option a central bank has is increasing the interest paid on excess reserves. The Federal Reserve pays interest on bank's reserves held at the Fed. Through increasing this rate it could theoretically set a floor under rates where banks won't lend to each other for less than they could earn from parking their reserves at the Fed. This would in turn drive up the Fed Funds Rate. This will prove ineffective in fencing in lending though. The rate at which banks lend to the economy will always exceed the rate at which a bank earns interest at the Fed. If demand for loans to economy increases and inflation returns, paying higher interest on excess reserves will be insufficient in cooling off lending because a bank would rather lend at the prime rate if the demand for credit is there.

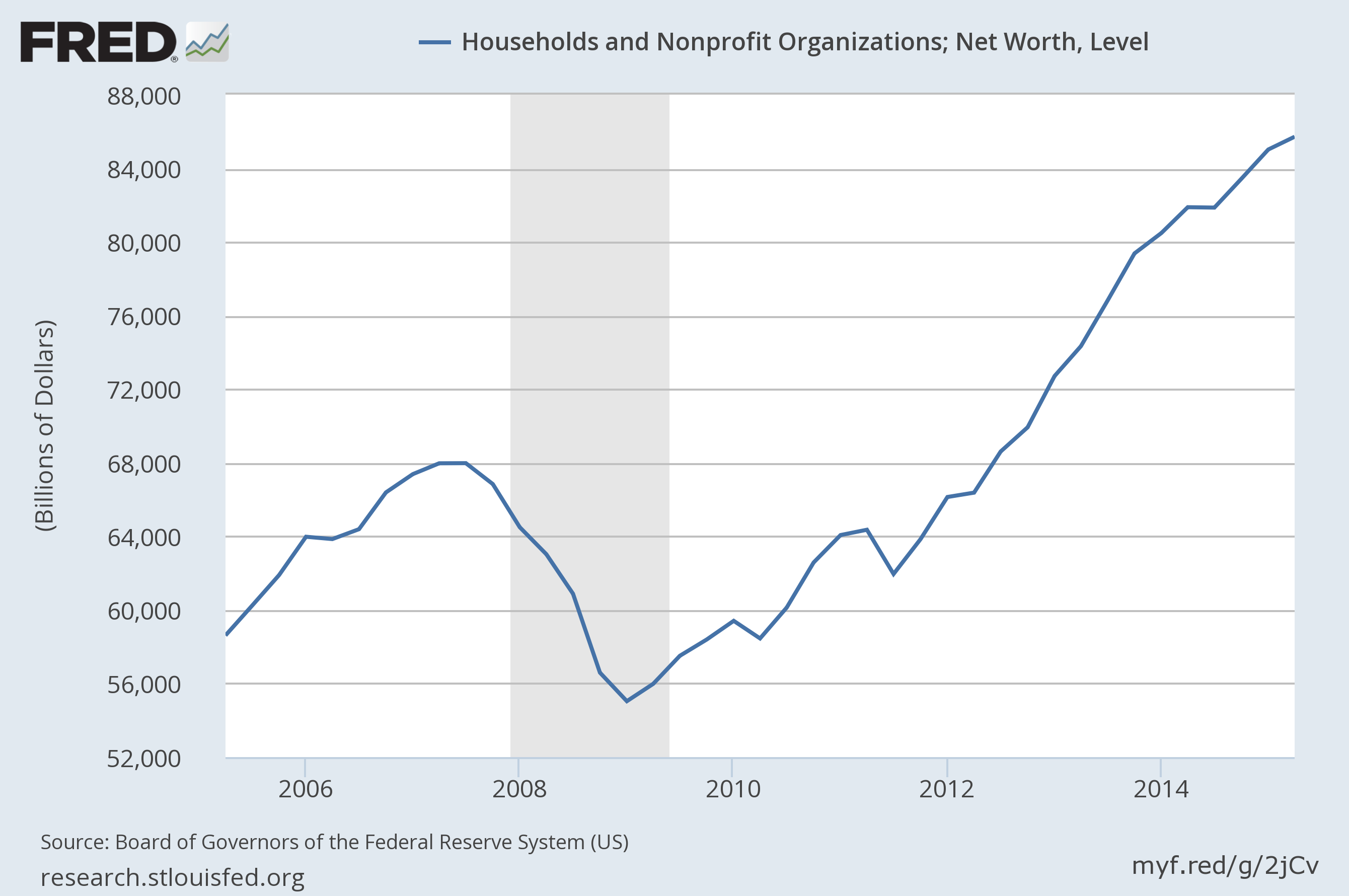

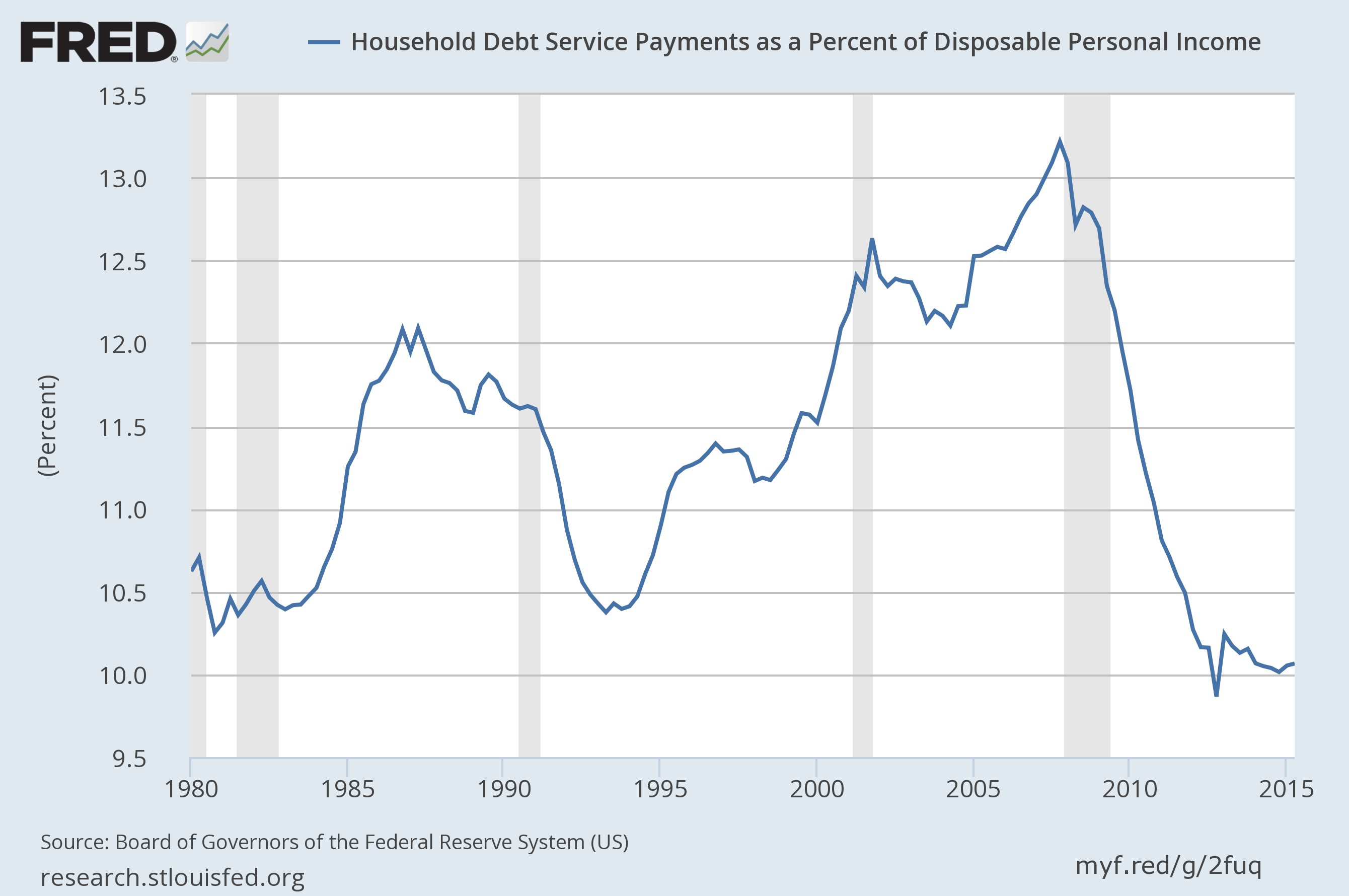

I believe were on the path of a major increase in demand for credit. Household balance sheets are repaired and debt to income ratios have returned to a normal level. What will stop the expansion of credit and inflation when it begins increasing? Banks have limitless reserves to lend and the Fed has a minimal ability to impact this meaningfully unless we see an extremely substantial contraction in the Fed's balance sheet, which may have recessionary consequences.

(click to enlarge)

(click to enlarge)

This is why I believe the next several years will be characterized by the overshooting of monetary policy. First, this ultra accommodative policy will overshoot and inflation will begin increasing.

Exactly when is unknown, but I would say late 2017. Credit will expand greatly therefore creating money and spending in the economy. The central bank will be unable to rein this in because of all the reserves it created during the quantitative easing program. It will require massive sales in the Fed's securities holdings such mortgage backed securities and bonds to drain reserves from the system. This will create major contraction in the Fed's balance sheet, which may prove recessionary. That is when the bull market and economic expansion will end (NYSEARCA:SPY).

In summary, when inflation increases, the Fed's ability to tighten policy effectively while not lowering growth and disrupting financial markets may be insufficient. Reserves in the banking system can be thought of as potential energy. Only when lent does it become kinetic. At the moment, there is massive potential for excessive inflation driven by the expansion of credit. I don't believe the Federal Reserve can unwind all this gently. If demand for credit begins increasing rapidly, inflation will be an inevitable consequence. Balance sheet repair and household deleveraging has essentially rendered the easing effect of monetary policy ineffective, while I believe in the future, the tightening effect of monetary policy will prove to be ineffective because of QE and the amount of reserves in the banking system. There is a risk of a nearly unconstrained expansion of credit.

Given this scenario, one might ask why I am short gold. I believe the USD (NYSEARCA:UUP) will continue climbing higher as a result of divergent global monetary policies, particularly between the Fed and the ECB. Longer term, I am extremely optimistic on gold, although I think it can fall, perhaps a lot, further in the near term. The key moment to go long gold will be when it begins trading up on higher inflation. Right now, higher inflation is bearish for gold as it signals Federal Reserve tightening. When gold trades positively on inflation it will be a huge change in the markets working opinion. Inflation will become the primary driver, as it has historically, rather than divergence.

0 comments:

Publicar un comentario