Summary

- Bond yields are terrible and the weak interest rate environment is hammering retirees.

- Inflation is nonexistent for most of the economy, it is just the retirees getting screwed.

- Despite all the posturing by the Federal Reserve, the market is starting to recognize their futility.

The problem with raising rates is tied to the flow of jobs between countries.

- The only hope for raising rates is an international agreement between central banks to raise rates in unison.

My portfolio includes two mREITs and precisely zero direct bond positions. The problem is that my primary reason for buying bonds would not be the interest income; it would be a play on interest rates moving even lower. I believe a very solid investment thesis can be written for rates moving even lower, but I don't like buying into a bond position to make short term bets on price movements. It goes against my investment philosophy of establishing long term positions in quality assets.

Rates Suck, No Improvement on the Horizon

I feel for the millions of retirees that would love to have a substantial bond position to establish a reliable level of income for their portfolio that was contractually obligated rather than relying almost entirely on dividend income as the driver of the portfolio's income. The situation they are facing stinks, but I don't foresee interest rates moving materially higher on a permanent basis in the next decade. I'll grant the Federal Reserve may offer some really great posturing that could drive up yields and down prices, but I'd see that as a bond buying opportunity since I don't think "high" rates will last. To be fair, the rates we are likely to see would be better described as "less anemic" than high.

The Federal Reserve Can't Do It

When it comes down to it, I simply don't believe the Federal Reserve can create the influence on interest rates that they want to create. Further, I believe that their posturing is damaging their credibility with the market. While the board continues to blather about the importance of raising rates, the market is placing their own bets and clearly the Federal Reserve has about as much credibility as a five year old with chocolate smeared on his face. Sure, it was the dog that got into the cookies…

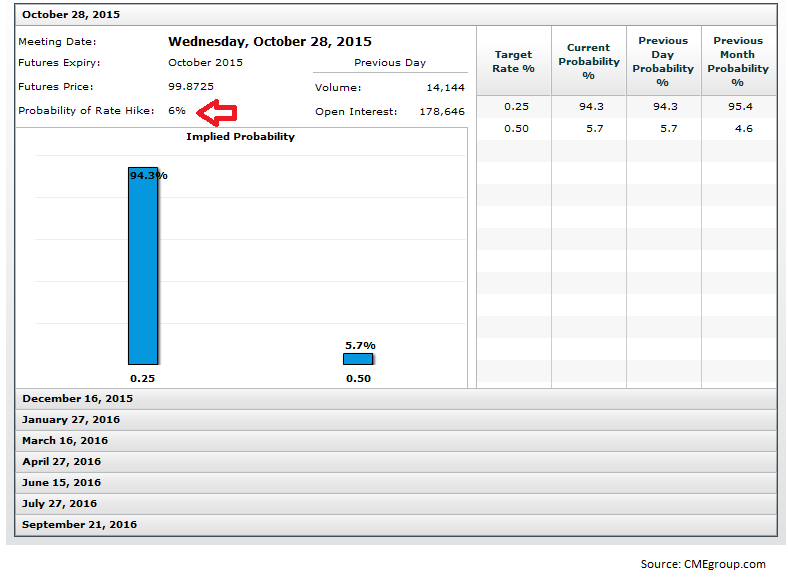

The best guesses currently available for predicting the movements of the Federal Reserve come through the form of the "Fed Fund Futures". The following chart from CMEgroup.com demonstrates the markets belief in the Federal Reserve jacking up rates at the next meeting:

(click to enlarge)

Note the red arrow indicating a 6% chance of an increase in rates. I'd say that's about the same level of credibility I'd give that kid with chocolate on his face.

The Problem

It isn't that Federal Reserve does not want to raise rates; it is that the international markets are simply not going along with that script. The Federal Reserve has a dual mandate for price stability and full employment. The goal for inflation has generally been 2% per year and full employment is sometimes assumed at 5% unemployment. We have been seeing inflation, but it has not been inflation across the entire economy. I think retirees have been disproportionately impacted by the inflation as a function of the premiums they must pay. Since increasing costs have not been evident across the entire economy, it is difficult to believe that the Federal Reserve will suddenly declare that the 2% goal is achieved.

The unemployment picture is even worse. I believe full employment is around 3% unemployment rather than 5%, but I don't think the Federal Reserve wants to buy into that theory. When they apply the Taylor Rule to policy decisions, they may generate a higher expected fair rate than I would generate because they have a different baseline assumption about the definition of full employment.

Even if the Federal Reserve can force short term rates higher, the consequences could include capital flows into the United States. That may sound pretty nice in theory, until you consider the consequences of strong dollar policies. An appreciation of the U.S. currency reinforces the outsourcing of labor to other countries which drives up domestic unemployment. When those jobs leave, it is very difficult to bring them back. Any taxes targeted specifically at exporting jobs would be a political landmine, but the incentives to export jobs are substantial. In addition to the strong dollar driving effective costs down, the lack of strict international worker safety laws lowers the cost of doing business abroad.

Quite simply the consequences of raising rates without a coordinated international effort could be severely damaging to the long term prospects of domestic workers. This isn't a problem that only impacts the United States; this is a problem for any country that needs domestic workers to have jobs. To the best of my knowledge, that still describes every country on Earth.

Possible Future Scenario

I think there is a decent chance that the Federal Reserve summons the courage to jack up rates for a quarter or two. If they manage to lift the longer ends of the yield curve or crash the price of equity REITs, I'd see either as a buying opportunity. If they do get rates up, they may find themselves forced to drop the rates back down subsequently due to the pressures of international trade.

The Way Higher

The one method I can foresee to really get rates going up on high credit quality bonds is to have an international agreement between central banks to raise the rates together. Such an agreement to raise short term rates throughout the developed economies would prevent the enormous capital flows. Doing so would result in dramatically less damage to employment rates.

I want to stress that the impact of low rates on employment is an international case rather than being a strictly domestic issue. Low interest rates simply are not stimulating enormous amounts of capital expenditures that would create an abundance of jobs. Corporations are not ramping up their capital expenditures; they are approving enormous amounts of share buybacks to drive up EPS by reducing the volume of shares outstanding. Thus the problem with raising rates is not that it would suddenly cause corporations to cut back on capital expenditures.

Because low rates are not spurring dramatic capital expenditures, a commitment across most developed nations to raise rates in unison should not be expected to drive global unemployment higher.

Conclusión

Absent an international agreement to raise rates, I simply don't see a path for the Federal Reserve to raise long term rates. They might be able to push up short term rates, but such a policy would still require disregarding their only two mandates. I'd love to see higher rates available on high quality securities, but any country trying to get there alone is just asking for punishment.

0 comments:

Publicar un comentario