Preparing For A Market Collapse, Part III

Summary

U.S. equities are down but not cheap.

They could fall further.

It is time to prepare….

… In fact, it is always a good time to be prepared. This is the third in a series. You can read Part I and Part II for background.

… In fact, it is always a good time to be prepared. This is the third in a series. You can read Part I and Part II for background. Since the series began, the S&P 500 (NYSEARCA:SPY) is down over 10%; it could have much further to fall.

What current shorts have the most asymmetric exposure? How can average investors see the need to short? Here are three specific short ideas followed by three ways for investors, including retail investors, to weigh when to short.

China

In terms of country exposure, China is among my favorite shorts. Artificial central bank stimulus drove the Chinese equity mania in early 2015. New equity buyers flooded into the market. These new investors purchased stocks using a record amount of margin debt. They had weak hands once the market direction turned around. The supply of new capital was finite. Eager new investors pushed up prices, but quickly pulled out of the market once prices declined. How do you short China? One way is to short Direxion Daily China Bull 3X Shares (NYSEARCA:YINN).

It is down over 70% since I first disclosed this idea, but it could drop much further over time. That being said, not all Chinese equities are expensive. While China is a big short idea overall, there are some small long ideas worth considering, such as Taomee (NYSE:TAOM).

Biotech

Turning to sector exposure, biotech is another favorite short opportunity. This has been a hot sector, but one with market prices that are high, unstable, and precarious.

It is down over 20% but remains overpriced. In the long term, it will probably decline substantially further. While biotech is a major short opportunity, one can find bargains in the wreckage. Depomed (NASDAQ:DEPO) is one worth considering. Due to its drug prices, it is far less sensitive to political pressure than Horizon (NASDAQ:HZNP) or Valeant (NYSE:VRX).

High Yield

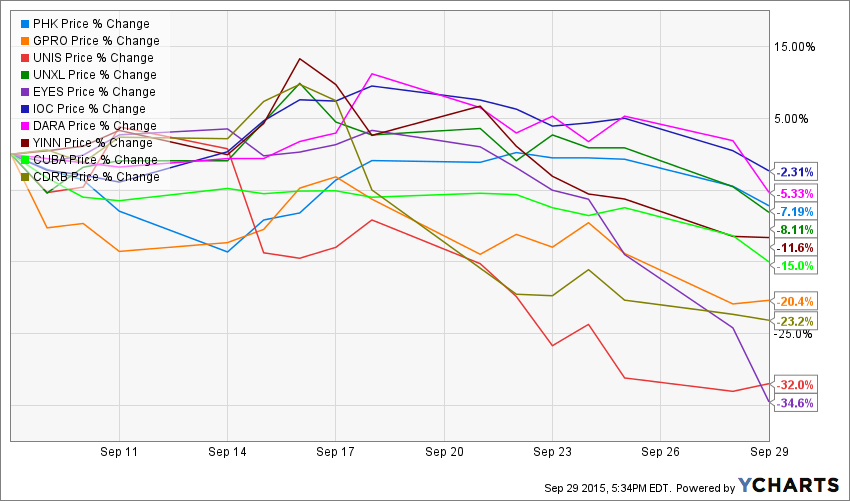

In the current credit environment, "high yield" is a bit of a misnomer. In fact, it borders on false advertising. This is one of my favorite types of securities to short because high yield is expensive enough that it does not cost too much if it maintains these rarified prices, and investors long this exposure will probably not hang in there if it begins to decline substantially. Retail investors (including not just a few on Seeking Alpha) who seek yield at any price have driven securities with the appearance of stable yield to zany prices. One security to consider is PIMCO High Income Fund (NYSE:PHK). As of today, it trades at a 13% premium to its NAV.

Down over 25%, it is still overpriced. Its price should continue to converge upon its value in the years ahead. If credit spreads widen from here, it could decline substantially. Should you own any broad-based bond exposure? At today's prices, no.

"HPHs [high priced helpers] frequently think of risk as a function of asset class along the lines of "cash is safe, stock is risky, and bonds are in the middle". In reality, risk is never a function of asset class; it is a function of price. Thinking proxies such as asset class-based risk models are designed only to excuse HPHs from doing any fundamental analysis to determine value. They can't make you safe because they can't even define, let alone quantify, risk. If you are a 65-year-old retiree, a smart-sounding HPH might say that you should be 65% in bonds, with others arguing importantly that the right number is 70% or 60%. The right number is 0%. Alternatively, come up with an explanation of how the credit market is currently undervalued. I could, of course, be completely wrong, but the current credit market looks like an epic bubble. It is conventional to own a lot of bonds, but when the bubble bursts, you will conventionally lose a lot of money."- Where Can I Find Safe Income For Retirement?

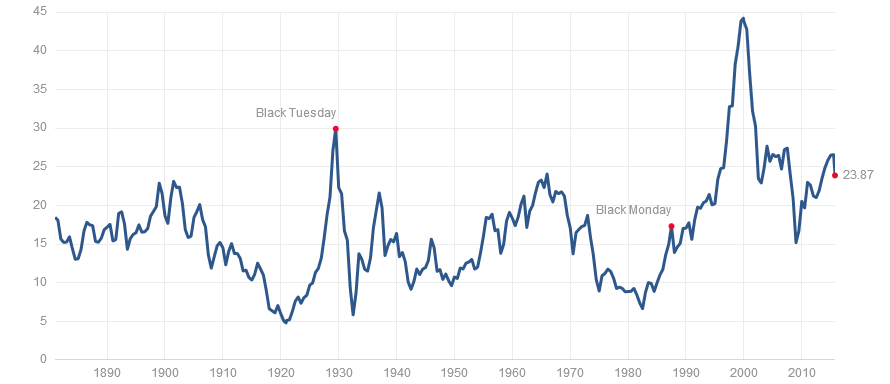

Shiller P/E

When to short? At the level of individual securities, the fundamental analysis and event analysis takes more time than most investors have to short stocks. In terms of shorting country markets, sectors, or parts of the capital structure, there are some readily-available resources that might be helpful in knowing when to short.

For a quick heuristic on the market's price, you might consider the Shiller P/E. This ratio is more indicative of value across business cycles because it is less impacted by fluctuating profit margins.

The U.S. equity market's Shiller P/E is currently over 43% above its historical mean of about 17. Market prices have rarely maintained such high multiples for long. For further reading on topics, including the Shiller P/E, you might like Rock Breaks Scissors: A Practical Guide to Outguessing and Outwitting Almost Everybody. U.S. equities are the fourth most expensive in the world according to this metric, behind only Japan, Ireland, and Denmark.

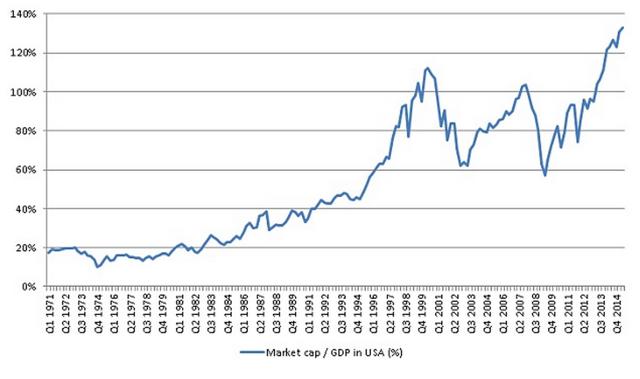

Market Cap/GDP

Market capitalization / GDP in the U.S. is another key metric. When it is high, it is a particularly important time to focus on short opportunities. Today, the U.S. market cap is about 112% of the U.S. GDP. Historically, from such lofty levels, subsequent total returns are typically less than 2% per year.

The U.S. equity market is pricey on both metrics. Real returns are probably negative or too low to justify the risk. Incidentally, on both metrics, Russia is a bargain. Its Shiller P/E is about 5 and its market cap/GDP is about 18%, close to its historical minimum of 17% over the past 15 years. The inverse, leveraged Russian ETF (NYSEARCA:RUSS) is down over 25% since our previous article on that opportunity.

However, despite the move in price, it remains an attractive short.

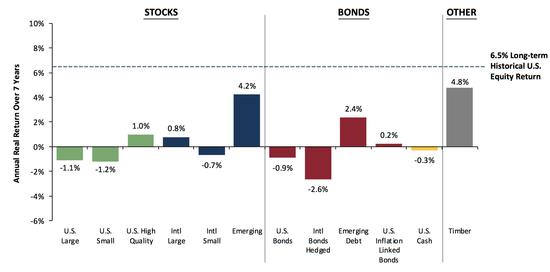

7-Year Real Return Forecast

GMO publishes a monthly chart comparing the estimated prospective annual real return over the subsequent seven years of various asset classes from current market prices. The comparison between the 6.5% long-term historical U.S. equity return and the returns from today's levels is not favorable for today's equity investors.

Average returns will probably be around zero, with somewhat negative returns overall and only marginally positive returns for equities that GMO considers to be high quality. At least we have plenty of timber in Maine, so we have that one covered.

Conclusion

Part I covered the virtues of maintaining both sizing discipline and a cash balance.

"Ordinary opportunity sets should lead to only ordinary position sizing, leaving extraordinarily large positions for only the rarest of opportunities. At a one percent position, one could conceivably find subsequent risk:reward opportunities to double down three times and still have a statistically diversified portfolio. Hyper-diversification accomplishes very little, but having a dozen truly uncorrelated positions accomplishes much of what correlation can offer. However, if one starts with a 5% position and doubles it three times on apparently better subsequent entry points, one is left with an over-concentrated or overleveraged portfolio."

"When everything is going horribly wrong, the comparative advantage of being more liquid than your marginal counterparty becomes extreme. So, while I do not know what the right amount of cash is, I am certain that it is better to have more. You should have more than whomever you are trading against when nothing is working in the markets. How much is that? I currently have 25% of my assets in easily accessible cash and am glad that I do. My percentage might be too low but I am virtually certain that it is not too high. Whatever opportunity cost that I pay in terms of diminished return can be quickly recouped during the next market collapse."Part II covered some of my favorite company-specific short ideas. The ten disclosed short ideas declined from 2 to 35% since publication; none have yet to fully converge upon their intrinsic values.

The average decline of 16% is over three times the S&P 500 (SPY) decline over the same period. The larger point is that a flexible mandate that allows one to go long or short creates an optimal environment for analytical rigor.

"When someone is able to buy or short investment opportunities, he can first be analytical - gathering relevant facts, measuring value, and examining events that are likely to unlock or reveal that value. One need not be a fan, only an analyst. Regardless of whether or not you like what you are looking at, there is something to do either way. One can buy, one can short, one can ignore. One does not need to prejudge before reaching a conclusion informed by the relevant premises."You can protect your capital by shorting expensive (and therefore risky) securities with exposures to China, biotech, and high yield credit as described above in Part III.

Additionally, you can monitor the Shiller P/E ratio, the market cap/GDP, and the 7-year return forecast for a quick look at the market's price. These tools are valuable additions to the toolkit of the prepared investor. Regardless of the specifics on how you choose to prepare for the possibility of a market crash, it is unlikely that the next half-century will look anything like the past.

It is (barely) conceivable that it continues at the current pace and the S&P 500 races through 48,000. But even if it is possible, it is not a safe bet. When it comes to investing, I do not hope for or expect any single outcome. I do not hope or expect that my home will burn down either, but I still have fire extinguishers and plenty of insurance. None of this is a call to panic; it is a modest call to prepare. I would be perfectly happy to be wrong in my view that such preparation is both wise and timely.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

0 comments:

Publicar un comentario