Summary

With the passing of the ECB events last week without any action, gold and silver prices had an opportunity to run higher and had begun to do so.

Though that opportunity was severely disrupted by the Fed Chair's statements Thursday evening, which failed to waiver in the slightest from the FOMC statement of a week prior.

With the extension of uncertainty about a potential Fed rate action through October now reinforced by an unwavering message, the dollar strengthened again Friday and gold gave up ground.

This week's intensification of the U.S. government shutdown issue will likely rehash prior rating agency discussions about the U.S. sovereign debt rating and burden the U.S. dollar and serve gold.

I expect the U.S. Fed will not raise interest rates in October. If it does not, the dollar should give up ground and give precious metals some lift.

The threat of an October interest rate action was thus reinforced and the dollar rebounded. In effect, Janet Yellen offset the impact of the passing of ECB events last week without any new action by the European Central Bank, which had stabilized the euro versus the dollar and given gold a lift. I still expect an intensification of government shutdown concerns this coming week and beyond to weigh on the dollar, and also for the October Fed meeting to pass without rate action, giving support to gold. The risk to this view is that if the Fed raises rates in October, I believe it would be a temporary setback for gold that could run into 2016 until investors begin to again anticipate European and global recovery and a normalizing dollar. If the Fed refrains from action in October, as I expect it should, precious metals prices should muster a run higher into November before again facing a Fed-driven challenge.

Long-term metals investors can expect a more sustainable upward trajectory to start in 2016 (likely in the second half), when the ECB is likely ready to end its quantitative easing program or if some other unforeseen factor comes against dollar strength.

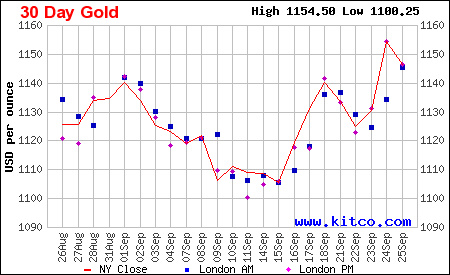

30-Day Gold Chart at Kitco.com

The 30-day chart of gold prices shows the makings of a rally that unfortunately appears to have been stopped short (likely temporarily) at the close of the week. Gold and silver prices immediately increased after the U.S. Federal Reserve failed to raise interest rates in September, but declined once it became clear the Fed could still act on rates in October of this year. Gold and silver were also pressured by investor anticipation of a potential action by the ECB to further loosen monetary policy, which likewise serves dollar strength and harms precious metals commodity prices. But when the ECB failed to act, as I expected, gold got the fuel it needed to start a more sustainable move higher. That is until the U.S. Fed Chair spoke in Massachusetts on Thursday evening.

The Fed's Janet Yellen failed to waiver in the slightest from the message the Fed presented at its monetary policy meeting a week prior. She reiterated that the FOMC members anticipated rates would rise "some time later this year." Unfortunately, that would be inclusive of October.

This irresponsible extension of uncertainty I believe is the failing of the Fed that enabled the nascent stock market volatility to continue forward for another month. It appears it will now do the same to precious metals prices, though with some exception.

| Precious Metal Relative | 09-25-15 |

| SPDR Gold Trust (NYSE: GLD) | -0.6% |

| iShares Gold Trust (NYSE: IAU) | -0.5% |

| ETFS Physical Swiss Gold Trust (NYSE: SGOL) | -0.6% |

| iShares Silver Trust (NYSE: SLV) | -02% |

| ETFS Physical Silver Trust (NYSE: SIVR) | -0.3% |

| Market Vectors Gold Miners (NYSE: GDX) | -1.7% |

| Market Vectors Junior Gold Miners (NYSE: GDXJ) | -2.3% |

| Direxion Daily Gold Miners Bull 3X (NYSE: NUGT) | -4.0% |

| Goldcorp (NYSE: GG) | -1.0% |

| Randgold Resources (NASDAQ: GOLD) | -2.0% |

| Barrick Gold (NYSE: ABX) | +0.2% |

| Silver Wheaton (NYSE: SLW) | -0.8% |

| Coeur Mining (NYSE: CDE) | -5.5% |

While the U.S. government shutdown issue is not especially dangerous to the U.S. economy, or appears so based on historical precedent, I anticipate it will still weigh on the U.S. dollar and help it to stabilize around current levels or creep lower. You'll recall that the rating agency, Standard & Poor's, in the past criticized the U.S. government's political environment, effectively warning that it was a negative factor on the sovereign debt rating of the nation.

These types of concerns will be rehashed this week and could have meaningful sway on the dollar.

However, this too shall pass, though I believe after much consternation and probably a government shutdown. Gold and silver prices should benefit from that eventuality, as I see it.

As we approach the October Fed meeting, though, the overhanging threat of a rate action will likely work against gold longs again. That will allow for a buildup of pressure as investors remain uncertain about exactly how the Fed will act in October.

It is my expectation that the Fed will again keep from acting in October, which would serve as a release of tension and let the dollar slip and gold and silver prices gain along with equities. In that case, the rally that should have been happening now - if not for the Fed's stubborn hold of position despite its impact on financial markets - should ensue and likely run into November for precious metals and longer for equities.

The risk to this view is that the Fed acts in October to raise interest rates. If that scenario plays out, I expect equities will still rise after perhaps a very short-term slip. Gold and silver prices, though, would be impacted in a more meaningful manner and likely remain burdened by a strengthening dollar into 2016. Long-term investors in precious metals should still see relief some time in 2016 when the ECB finally concludes its quantitative easing program or when some other unforeseen factor comes against dollar strength.

0 comments:

Publicar un comentario