Emerging Latin America's Economies And Their Development, Part III

Summary

Peru shows a lot of growth.

Safety and easiness of doing business are weak points for Latin America.

Latest changes in the world economy show huge challenges to commodity producers.

Mexico and Chile.

I have kept the text in its original form, even the notes for references are there so readers who are truly interested can go and find that source material here. This information is only one-year-old so it is still quite accurate and hopefully interesting reading for everyone. I have added new comments to update the situation if seen necessary.

Foreign Direct Investments

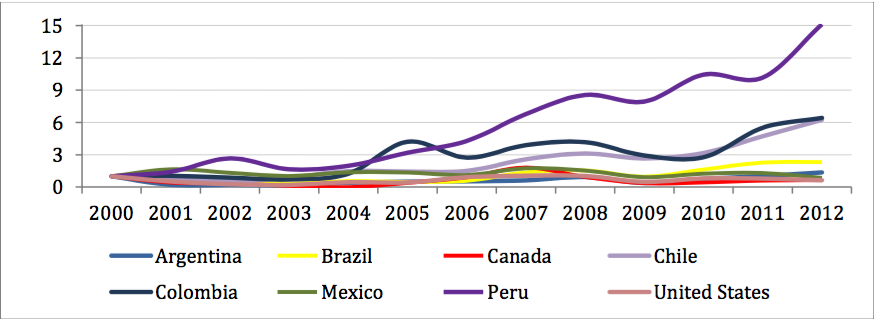

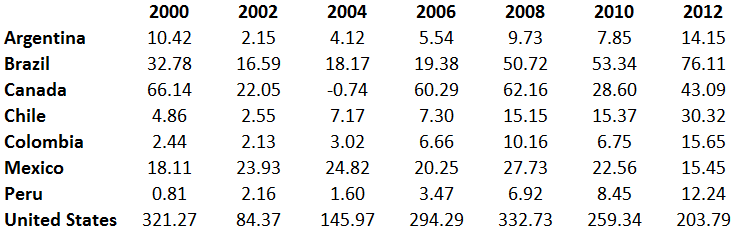

Foreign direct investments display clear differences between countries. The graph below, based on numbers by the World Bank, shows yearly values compared to the first value of the series to easily see how investment amounts have grown. Table 3 below shows those actual numbers.

Numbers are reported by the World Bank and the table below shows actual numbers from even years. Interesting detail is that, in 2004, Canada actually experienced an outflow of investments, but this was only during one year and recovery was quick. This might indicate that Canada is not trusted to be as strong economically as someone would first have thought, which creates its own set of difficulties and possibilities for international investors. Peru has experienced the largest growth, but it also had the lowest starting amount. What is one key point behind these numbers is that growth in foreign direct investments indicates that foreign investors find that country's growth to be credible and possessing room for new businesses.

(click to enlarge)

Figure 7. Growth of foreign direct investments

Chile, Colombia and Peru show the largest gains from their starting values and all South American countries show at least some level of growth. With Argentina, the situation is confusing, but lately it has been looking better than before. North America is the opposite, as South American countries are pulling in more investments, North American countries, Canada, the USA and Mexico, have all slowly gone downwards. With the USA, investors are probably expecting stronger signs of recovery before they return to the market again as they find new opportunities from many other countries, such as Peru. With Mexico, negative growth is surprising, as Mexico has supposedly been pulling investments from companies that want to offer their products to the USA and Canada but want Mexican workforce and low custom tariffs, or simply to offer their products to a population that is slowly getting wealthier.

Reported investments to Mexico should be growing in a few years. Brazil and Argentina could possibly face an outflow of investments if their situations continue to seem darker. If this could then affect the rest of the Latin American countries is a difficult question to answer; on some scale, the answer is yes.

An example is a news concerning Volkswagen's (OTCQX:VLKAY) North American investments that were mainly focused to Mexico (Reuters 2014; Wall Street Journal 2014). 2012 was a sudden quiet year for Mexico and this can be expected to change as Mexico is updating its laws to be more open for foreign and private investments. This is something Mexico did recently with their oil and gas field rights to boost their economy (Bloomberg 2014; BBC 2014c). As Economist explains (Economist 2014), emerging countries continue to be the target of many multinational companies, but not all have gotten their share of the success and even some previously successful companies are lately starting to experience slowing growth.

Table 3. Foreign direct investments in billions of USD

(click to enlarge)

Human Touch on Business Success

Following paragraphs look at a few indicators such as corruption and easiness of starting a business to especially see some human-made obstacles that these countries need to handle in order to get closer to their maximum potential. Let's look at easiness of starting and doing business in these countries to understand whether countries with slow foreign direct investment growth have a clear reason for it. In a study of 189 economies (World Bank Group), it states that these eight countries are in following order: Canada (rank 19 of all 189 for doing business; rank 2 for starting a business), the USA (4; 20), Chile (34; 22), Mexico (53; 48), Peru (42; 63), Colombia (43; 79), Brazil (116; 123), and Argentina (126; 164).

Let's also note that the average for a high-income OECD country is 11.1 days for a business application to be processed. Average for Latin America and the Caribbean is 36.1 days, so there we can see a clear obstacle hindering birth of new businesses in Latin America. Canada, the USA, Mexico and Chile are already relatively friendly for businesses, but last four are surely missing out on a large number of foreign direct investments until they lessen their bureaucracy (which can also mean bribery but most of all unnecessary paper work). Until this process is made easier, by for example eradicating corruption and eliminating sending of unnecessary application papers, Latin America as a whole is indeed slowing down its economical development.

Safety

In succeeding paragraphs, I will look at some other statistics outside economics: Corruption, political stability and homicide rates. This is done because corruption can set varying obstacles for a company to set up and run its business. Political instability, such as constantly changing governments makes it challenging to run a country or a business effectively and this creates uncertainty in people, as they cannot know how their future will be affected. Homicidal rate, on the other hand, marks safety of that country and this sets other kinds of obstacles or possibilities in areas such as the security industry.

Based on a report by the United Nations Office on Drugs and Crime (2013) that lists countries' homicide rates per population of 100,000 for 2012 (or latest available value): Colombia 30.8, Brazil 25.2, Mexico 21.5, Peru 9.6, Argentina 5.5, the USA 4.7, Chile 3.1, and Canada 1.6. There we can see a clear difference between developed and emerging countries, as Canada with 1.6 is quite far from Colombia. What could be considered surprising is that Chile is next safest on the list, before USA's 4.7, which is also closer to Argentina than Chile. Safety is something everyone wants for themselves and their family. It is one clear factor that makes people leave their country and outflow of brainpower is something no emerging country can afford.

Corruption perceptions index done by Transparency International (TI 2013) lists 177 countries according to their level of corruption compared to each other. On this list, countries followed by this thesis are given following ranks among all the countries (country with the smallest rank is the least corrupted and vice versa): Canada 9, the USA 19, Chile 22, Brazil 72, Peru 83, Colombia 94, and lastly Argentina and Mexico share position 106. Again, we see the USA and Canada at the top and Chile being close behind the USA. This tells us that if an investor wants to avoid corrupted governments in the emerging markets, then Chile is a top candidate as only a few underdeveloped countries manage to place better in the whole list. According to Economist (2014), Latin Americans also have very low public confidence level in their justice systems with high corruption, low conviction rates and in many cases growing murder rates.

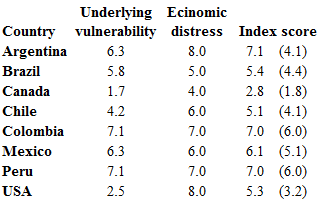

To measure political instability, I use the Political Instability Index that covers period 2009/10 (see Table 4). This information is collected and published by the Economist Intelligence Unit (EIU 2011). The index combines measures of economic distress and underlying vulnerability to unrest. For comparison, the most corrupted country, according to the list, is Zimbabwe with vulnerability to social unrest being 7.5, to economic distress 10 and combined index then is 8.8 (in parentheses is index score from 2007). Least corrupted country was Norway with ratios of 0.4 / 2.0 / 1.2 (0.2).

UPDATE: I would love to compare how these numbers have changed, but sadly I haven't managed to find newer information that is available without charge.

Table 4. Political stability

Because these numbers are 2009/10 and compared to 2007, I cannot make direct conclusions as to what these numbers are today. A common theme for countries on the list has been that their index score has grown bigger from 2007. Because these are the years right on the financial crisis period, I believe this is the controlling reason behind this growth. By looking at the evidence above, it can be seen that since 2009 many indicators have again become much more positive, therefore it is reasonable to expect that index scores have gone down since, but later perhaps rose again in certain countries like Argentina (due to economic instability), Mexico (personal safety issues due to drug cartels) and the USA (growing government debt).

Conclusión

It is impossible to look at data and know for certain what the future of these countries be. Large part of their future is up to the international demand for their resources and know-how. This is something that is impossible to predict in the long term. Hopefully, these emerging countries manage to move more to the know-how as their resources cannot last forever. Some sort of change in Latin America, in general, is needed to motivate more growth to happen. For that, easiness of starting a business is one indicator that is important, but it is not the only one that requires attention and improvements. Though, it could be one of the easier ones to improve.

Some other issues, such as safety and corruption are critical to improve, but those take time and constant effort on many areas.

UPDATE: Sadly commodity prices have been going down for a long time, and that is bad news for all emerging countries (like Brazil and Peru) where commodities like oil and minerals are important to the economy. Only time will tell what are the consequences and how governments manage to go around this problem.

For the USA and Canada, their main problem is growing government debt that should be turned around. Behind this, however, many complicated problems are found (which can be military spending, nonworking parliament, education system, etc.). At the moment, international investors don't see that there is a real problem (indicated by good credit ratings) but rising debt is something that eventually would be a problem if not properly handled before.

Problems behind it have to be improved and effort has to be put to improve positive factors as well. Of course, that calls for strong political will and decision-making. In countries as wide in geographical and business terms, it requires strong cooperation from local leaders to first acknowledge common problems and then achieve nationwide results to achieve actual results.

Latin America's problems are more widespread. Chile is by many terms the best of the six. It is certainly closest to a developed country and can be expected to be the first to be called such of all Latin American nations. Peru and Colombia are growing well but do have many problems they need to be able to handle. Those problems are many and it will take time, but I would not be surprised to see these countries continuing to provide best growth rates in the near future.

Mexico has plenty of potential, such as a young workforce that is still unleashed, and the country should at least grow faster with the economic demand and help they get from their northern neighbors.

UPDATE: Now that I have been following the world economy since writing this, I am more pessimistic with my expectations. The USA is looking good for now and its demand will help especially Mexico. On the other hand, China is expected to need lesser minerals for its growth and this can be very bad for commodity-dependent countries like Brazil and Peru. In the end, it all comes down to how world economy develops, and at the moment, things are looking positive.

Considering factors such as indebtedness of developed nations and recent stock market behavior, I continue having pessimistic expectations for Latin American nations.

Argentina is a case of its own, being haunted by its past that won't let go. If a sudden improvement happens concerning the debt situation, we might see big changes in a short period.

However, we must remember previously mentioned education levels and also corruption levels.

Brazil's short-term future is also a question mark now due to latest reports telling it is officially in a recession (BBC 2014). A recession might hold Brazil's growth down for a few years, giving other countries time to catch up with its development and possibly overpass it in some sectors.

Overall, Latin America presents a great potential. Though there are still many obstacles to be improved upon, eventually those would be resolved and these countries would achieve a new level of prosperity. This leads to great investment opportunities for individual investors and western companies with steady enough direction, as hesitation or speeding to the market without a solid plan can all lead to a quick and an easy failure.

UPDATE: Overall, I hold very positive long-term expectations for Latin America. Chile is a good example of a country where things have been done right and Mexico is in a good situation (economically and geographically) to grow much more. In the end, it comes down to how world economy changes, and if the direction continues to be positive, it will benefit emerging markets everywhere.

0 comments:

Publicar un comentario