Summary

Both GLD and the HUI looked like they were on the verge of one big final drop, then on October 2, the U.S. nonfarm payrolls data for September was released.

There are some bearish hurdles that suggest this rally might soon run out of steam.

Possible rotation out of the market and into gold is one bullish aspect to consider right now.

When you look at the big picture, the chart of the HUI doesn't show a huge move over the last few months.

I started to buy in big on October 2, as I anticipated a run to at least that level given what gold did that day.

And then a "curveball" came. As I said in a previous article:

"Besides, I simply don't have a crystal ball. I can't be 100% sure where the exact bottom is at. Rarely do things in the market go EXACTLY as you expect them to. There will probably be some curveballs along the way."So what do we make of this latest rally in the SPDR Gold Trust ETF (NYSEARCA:GLD), as well as the strong rebound in the gold and silver stock indexes such as the HUI and XAU? Is this the start of a new bull market, or is this just one last bear market rally before the final lows are hit? Does this curveball (meaning the HUI deciding to break higher, not lower) change the outlook? Well, I'm certainly still very cautious right now, but I have moved back to neutral until we get more clarity on a few things.

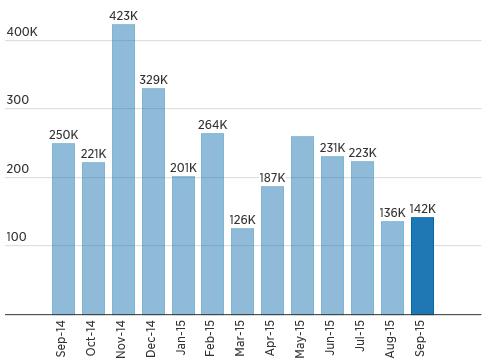

Both GLD and the HUI looked like they were on the verge of one big final drop, and then on October 2, the U.S. nonfarm payrolls data for September was released. The report said the U.S. economy created only 142,000 jobs in September, economists were expecting 203,000 new jobs for the month.

And the data from August was revised downward to 136,000, from the first reported 173,000 figure.

(Source: CNBC)

Investors interpreted this miss as further proof that the Fed would most likely hold off even longer when it came to raising rates, and gold spiked as a result. You can see the huge move in price and the massive volume that occurred just after the jobs report was released at 8:30 a.m. EST.

(Source: Business Insider)

GLD has added to its gains over the last week or so, as have the precious metal companies.

Many gold stocks have had strong percent increases during that time - climbing 25% or more.

Hurdles To Overcome

Given the rebound that has taken place this month, or maybe I should say stick save, some would argue that the lows are in. But there are some bearish hurdles that suggest this rally might soon run out of steam. These would need to be overcome before we could start to talk about a new bull market.

The first hurdle is we didn't see a capitulation type event in gold and silver, but one could make the argument that we did in the HUI. GLD had a slight downdraft in June and July, which amounted to only about a 9% decrease during those months. The HUI on the other hand, dropped 40%. Gold and silver stocks have a lot more leverage than GLD, but the massive carnage in the miners seemed to be suggesting that GLD was about to drop further. It didn't though, instead, GLD rebounded and now it's only down about 2.5% from where it was at the start of June. The HUI, on the other hand, is still down 21%. There is a big divergence occurring, and the gold stocks are still predicating more downside. Unless they can get back in line with the price of gold very soon, then GLD is going to decline once again.

It almost feels like an incomplete bottom. Had GLD moved down a lot further, then it would be easier to say the lows are in. But that is not what has happened. Gold would need to move above $1,200, or 115 on GLD, for this rally to have some real momentum behind it. Until that happens, it's too early to say the bear market is officially over. The short-term trend might be up, but the long-term trend isn't yet.

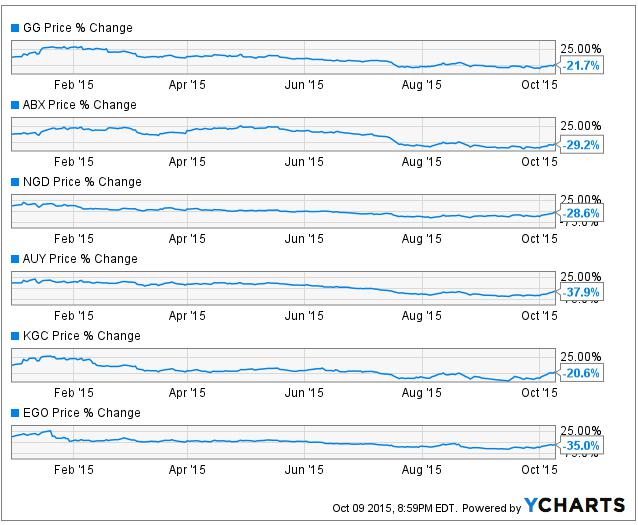

The second hurdle is, given that the mining stocks are down significantly for the year, they could start to be hit with tax-loss selling. The recent rebound has "painted some lipstick on these pigs," as the losses were a lot worse just a scant 2 weeks ago. But the vast majority of these gold and silver miners are still showing hefty declines YTD. Goldcorp (NYSE:GG) is down 21.7%; it was down 35% YTD at the beginning of this month. The rest listed below are still lower by a sizable percentage. There has been a major improvement since October 2, but as you can see the losses are still there. It's possible that the rally continues and most of these are erased, but if it doesn't, then tax-loss selling can feed on any stagnation or further decline in the HUI and XAU.

(Source: YCharts)

The third hurdle is the Fed still hasn't waived the white flag. It delayed hiking rates, but in no way has it suggested they are completely off the table for this year - even if economic data is weak. The temper tantrum that the stock market threw in August was the main reasoning the Fed has pushed back its timing for the first rate increase.

But the market is now assuming that the Fed will wait until 2016, or possibly even later, before it raises rates. I'm not convinced that is going to happen. The Fed stands to lose a lot of credibility if it doesn't begin to increase the Fed Funds rate this year. It might come as a shock to some investors, but the Fed has been implying for the last 3 years that it would raise rates during 2015. It hasn't deviated at all from that plan.

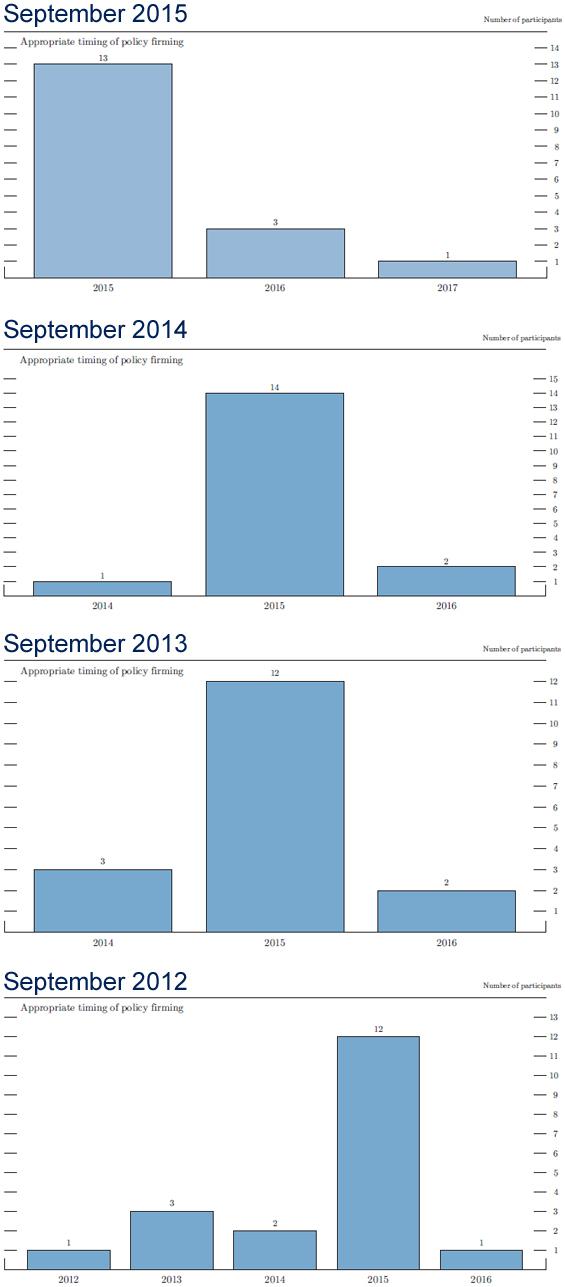

If you look below, you will see that the latest meeting in September showed a large majority of Fed members/participants believe that policy tightening should happen in 2015. That has been a consistent message since September 2012. Imagine how it would look if all of the sudden they flipped.

(Source: Federal Reserve)

After the September meeting concluded, Fed Chair Janet Yellen said at the news conference that followed:

"The recovery from the Great Recession has advanced sufficiently far, and domestic spending is sufficiently robust, that an argument can be made for a rise in interest rates at this time. We discussed this possibility at our meeting. However, in light of the heightened uncertainty abroad, and the slightly softer expected path of inflation, the committee judged it appropriate to wait for more evidence including some further improvement in the labor market to bolster its confidence that inflation will rise to 2 percent in the medium term."

"Now, I do not want to overplay the implications of these recent developments, which have not fundamentally altered our outlook."

"The economy has been performing well. And we expect it to continue to do so."

Yellen further made it clear that the crash in the Chinese market, as well as the severe decline here in the U.S, was the reasoning for the delay in rate hikes:

"The Fed should not be responding to the ups and downs of the markets and it is certainly not our policy to do so. But when there are significant financial developments, it's incumbent on us to ask ourselves what is causing them. And of course while we can't know for sure, it seemed to us as though concerns about the global economic outlook were drivers of those financial developments."Even though the disappointing September jobs report was released a few weeks after Yellen's news conference, it should have no major influence on the decision of when to hike rates, as Yellen stated at the time:

"And so they have concerned us in part because they take us to the global outlook and how that will affect us."

"As I noted earlier, it remains the case that the timing of the initial increase in the federal funds rate will depend on the committee's assessment of the implications of incoming information for the economic outlook. To be clear, our decision will not hinge on any particular data release or on day-to-day movements in financial markets. Instead, the decision will depend on a wide range of economic and financial indicators and our assessment of their cumulative implications for actual and expected progress toward our objectives."The Fed is looking at the big picture, not single pieces of economic news. Major declines in global stock markets are really the only thing that would probably give the Fed a good reason to pause. The economy is in decent shape, and the Fed isn't going to wait until things look peachy either, as per Yellen:

"If we waited until inflation is back to 2 (percent), and that will probably mean that unemployment had declined well below our estimates of the natural rate, and only then did we start to begin to ... diminish the extraordinary degree of accommodation for monetary policy, we would likely overshoot substantially our 2-percent objective and we might be faced with then having to tighten monetary policy in a way that could be disruptive to the real economy. And I don't think that is a desirable way to conduct monetary policy."Even Stanley Fischer, vice chairman of the Federal Reserve, said in August that officials:

"would not be able to postpone a decision until all doubts were resolved." "When the case is overwhelming," he said, "if you wait that long, then you've waited too long."The statements from the Fed, as well as their consistent expectations over the last few years for policy tightening starting during 2015, seem to strongly suggest that we will see at least a 25 basis point move at either the October or December meeting (most likely December).

Investors should recall that just two years ago, the expectation was for the Fed to announce at its September 2013 meeting that it was going to taper its bond purchases. The stock market, and in particular the bond market, started acting up in May of that year in anticipation of this major change in policy. The Fed decided to hold off at the September meeting, as it wanted to give the market a little more time to adjust. It finally started to taper in December of that year.

We could see a repeat when it comes to the first rate hike, sometimes the market just needs a bit more time.

So I believe that rate hikes are still on the table, and this should be clear at the conclusion of the next Fed meeting in a few weeks. If this occurs, then gold could come under pressure again. But it will be short-lived, I'm looking for a "sell the rumor, buy the news" event.

One Bullish Aspect In Play

If I had to point to one positive development for gold, it would be the decline we have seen in the major U.S. indices. Some readers might recall that I have always said the main competition for gold over the last several years has been the stock market, not the USD. Gold is always going to increase over time, no matter what the U.S. dollar is doing. What has taken the shine off of gold over the last few years has been the gargantuan rally in stocks. The concept of investors chasing returns is a familiar one, and with the run that the Nasdaq, S&P, and DJIA have had since 2011, it shouldn't come as a shock that the gold market was suffering from lack of attention and investor dollars.

(Source: StockCharts.com)

It has been my argument that only when the market finally peaked and started to roll over, that gold would bottom out. Since this time last year, I have expressed my belief that not much in the way of gains would be seen in the stock market during 2015. In an article this past June, before the market started to collapse, I said the following:

"The stock market has had an incredible run over the last 31/2 years. While they don't ring a bell at the top of a bull market, I would say this is either close to being over or is over. That doesn't mean we can't keep hitting marginally higher highs during the next 6 months or so, just like we have been doing since the beginning of the year....There is always the possibility for a blow-off top to occur as well, but either way the easy money has been made and the stock market is very unappealing right now."

I was expecting a big sell-off in the stock market towards the end of this year or early 2016.

Well, the time-table got pushed up, as investors started to liquidate in August. This market now officially looks broken, and I don't believe we are going to see new highs anytime soon, especially not with the Fed looming in the background.

So one could make the argument that the smart money knows the bull market in stocks is over, and it's time to look for assets that are undervalued and have underperformed everything else since 2011-2012. The most logical place to rotate into would be the precious metals sector.

Unless the stock market can have one final hurrah and stage a decent rally over the next few months, this rotation could continue, and that would put a firm bid under the price of gold.

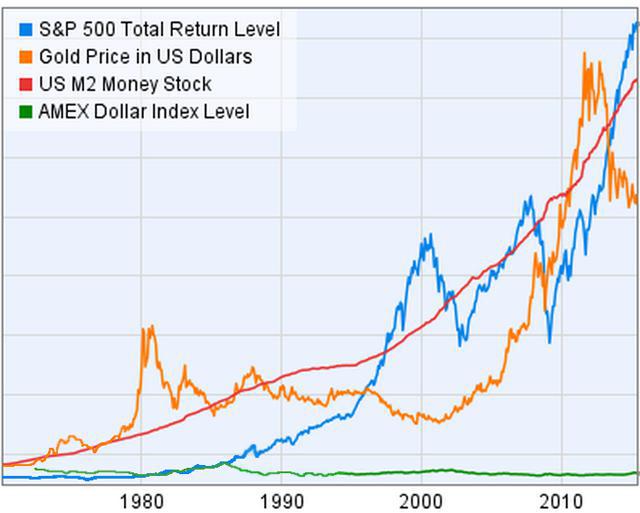

Below is a chart that I created using historical data points for the S&P, Gold, M2, and the USD.

I showed this chart in a previous article a few months ago when I talked about this eventual rotation out of the stock market and back into gold. Unless you are in some type of hyperinflationary environment, when gold does well, the stock market will underperform, and vice versa. This inverse correlation was very apparent in the 1970s, and has been since that time. Keep in mind we are talking long-term trends here, as gold and the stock market can rise and fall in tandem for months at a time. But when you compare long-term performances over many years, they just don't have their respective bull markets occurring during the same dates.

As you can see, gold and the S&P continually move higher with the money supply. But gold and the S&P usually move inverse to one another and oscillate around M2, as it increases in quantity. So when the S&P is in a long-term bull market (such as from 1980-2000), gold is in a bear market, and vice versa. This will eventually reverse course again, and it could be starting now. If that is the case, then over the next few years, the gold line will start to trend above the red one, and the blue line will trend below it. Over the long-term, the direction of the USD is irrelevant.

Source: Ycharts.com/author/FRED

As the saying goes, "never fight the Fed." The stock market has had an incredible run over the last several years; it's going to take a monumental effort to keep that going if rates are about to increase.

Money is rushing out of stocks a little sooner than I anticipated, and this "hot money" needs to find a home somewhere. Gold is the most logically choice.

So possible rotation out of the market and into gold is one bullish aspect to consider right now.

If This Is The Start, It's Still Very Early In The Game

There is a lot of anxiousness and confusion right now in the precious metal sector. Everybody wants to time this perfectly, or maybe I should say those on the sidelines that are calling for lower lows.

This is a great opportunity and investors want to maximize their gains. But most that are familiar with this sector know just how volatile it can be, and they know that the gold stocks can be down 30-40% in a heart beat. Nobody wants to step in front of this train if there is even the remote possibility for more downside. The gold sector hasn't been kind to many portfolios over the last few years.

But while it would be extremely rewarding to nail the lows in gold and the precious metal stocks, it's not necessary. The sector was massively undervalued to begin with, and still is, even considering the money that has been made since early October.

When you look at the big picture, does the chart below reflect a huge move in the HUI over the last few months? No, it doesn't, it looks like a blip on the screen. Even at 250, the index would appear to be just barely off the mat. If this is in fact the start of a new bull market, and I'm not suggesting it is yet, then it's very early in the game. Heck, we are just at the "singing of the national anthem stage," the game hasn't really even begun yet. Of course the chart below also supports the bearish argument that there simply isn't enough evidence yet to call a bottom.

(Source: StockCharts.com)

It's important to keep perspective here. So if you are still on the sidelines, know that if this is the start of a new bull market, then we have a long-long way to go. If you are even paying attention to this sector right now then you are at a big advantage compared to everybody else.

My Updated Plan Of Action

As I mentioned at the start of this article, I have been very bearish on gold since the beginning of June. However, as I told readers in early August, I was hedging my bets. The HUI was extremely oversold at the time, and at minimum, I expected some sort of rebound. I wasn't convinced that the lows in August were the final lows, but if they were then I would at least have a decent size build-up of precious metal shares. It was a very low risk opportunity at the time given the incredible pricing of the gold and silver stocks, and I felt that it was imperative to take advantage of it. I didn't jump all in, but I did establish many positions.

The plan since then has been to get in heavily, if the HUI breaks above 130; that was the key level to be taken out for me to get a lot more constructive in the short term. But I started to buy in big on October 2, as I anticipated a run to at least that level given what gold did that day.

I'm not acquiring these stocks on the notion that the bear market is officially over, rather I always just follow major support and resistance (as well as my gut). It has allowed me to avoid losing money in this sector, and is the reason I'm up for 2015 even though the precious metal complex is showing losses - sizable ones for many of the stocks.

I'm now neutral on the sector, given the recent gains. I'm going to hold for a bit and see what happens.

I have some good profits so I don't think I'm taking a big risk. Should this short-term move peter out, then I will look to book some of those.

The real tests still lie ahead, until those are passed, we can't label this a bull market yet. For now, let's see how this rally plays out and what the Fed says at the conclusion of its October meeting.

0 comments:

Publicar un comentario