The Federal Reserve

More red lights than green

The case for raising interest rates is worryingly hazy

Sep 12th 2015

.

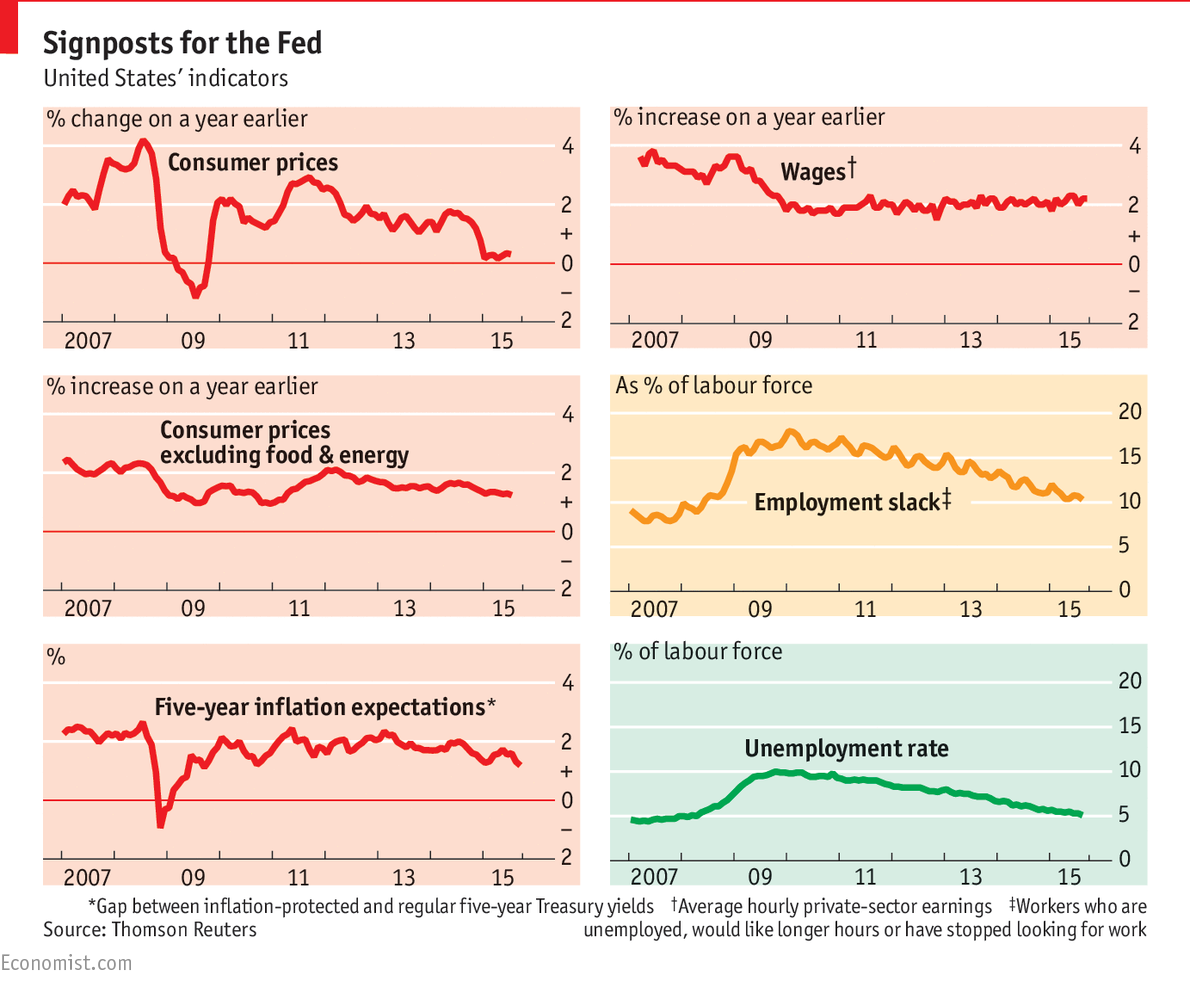

PITY the central banker. When models of the economy go haywire, academics can retreat to their offices to fix them. But even when signals flash red, amber and green at once (see chart), central banks must continue to steer the economy. When the Federal Reserve’s interest-rate-setters meet on September 16th-17th, there is a decent chance they will raise rates for the first time since 2006. The consequences of such a decision are shrouded in uncertainty, due to the strange behaviour of the American economy since the financial crisis.

Before the crash, economic models said central bankers had a straightforward task. So long as inflation expectations stayed on target, the Fed could more or less focus on the labour market.

High unemployment would allow firms to hire workers on the cheap, keeping their costs and prices subdued. A fizzier labour market would cause wages—and hence prices—to froth. The job of the central bank was to tweak rates to keep things in balance.

Yet in the six years since America’s economy hit rock-bottom, it has defied this textbook model.

In late 2009 unemployment reached a high of 10%. Such abundant slack should have caused inflation to disappear, but prices rose stubbornly. Today the opposite is true. The latest jobs figures, released on September 4th, showed unemployment falling to 5.1%—right in the middle of the Fed’s estimate of the labour market’s sweet spot. Yet inflation has vanished: the Fed’s preferred measure stands at just 0.3%, well below its 2% target. At their recent annual conference in Jackson Hole, Wyoming, monetary-policy wonks pondered this puzzle. In the meantime, however, ratesetters have to act.

The central bank is not just navigating through a fog; it is steering with a delay. The Fed reckons it takes 18 months for changes in rates to have their full impact. As a result Janet Yellen, the Fed’s chairman, has long emphasised that rates may rise before inflation is in sight.

By early 2017, the Fed reckons, many of the causes of today’s low inflation could have dissipated. The recent fall in oil prices, for instance, should depress prices only temporarily.

The dollar’s rise, too, should have a one-off impact: it is 16% stronger than a year ago, on a trade-weighted basis, which has made imports cheaper. If oil prices and currency markets now hold steady, inflation should rise.

That might coincide with a resurgence in wage-driven inflation, argue the Fed’s hawks. There are no signs of this yet, however. Hourly pay is growing by just 2.2% a year, down from around 4% before the financial crisis. Even accounting for America’s feeble productivity gains—growth in output per hour worked is running at just 0.6%—such paltry rises in wages are unlikely to be inflationary.

Weak wage growth suggests that there is still lots of slack in the labour market.

Underemployment, which includes workers who are part-time but want a full-time job, and discouraged workers who might be tempted back into the labour force, stands at just over 10%, higher than before the crisis. This measure probably has further to fall before wage growth picks up.

The Fed may also be underestimating how far unemployment can fall without stoking inflation.

In a recent note, Andrew Figura and David Ratner, two Fed researchers, point out that the labour share of income—the slice of GDP that flows to workers’ pockets—has dropped from an average of 70% in 1947-2001 to 63% in 2010-14. If that reflects a weakening of workers’ bargaining power—a result of globalisation and falling union membership—the so-called “natural” rate of unemployment may have fallen, too.

Making up for lost paycuts

Average hourly pay never shrank in cash terms, despite the surge in unemployment. This could have left “pent-up” wage deflation, according to researchers at the San Francisco Fed.

Eventually, however, this should run its course, allowing the link between inflation and unemployment to re-emerge.

If the hawks win out, their intention would not be to put the labour market into reverse, says Jon Faust, an academic and former adviser to the Fed. With interest rates still low, unemployment should continue to fall after a small rate rise, just at a slower pace. The economy is a big ship with a huge turning-circle; the Fed does not want to have to reverse course abruptly.

Inflation expectations seem sticky enough. In a recent speech Stanley Fischer, Ms Yellen’s deputy, emphasised that the results of surveys that ask people how high they expect inflation to climb in the long run have not moved much for years. But market-based measures of inflation expectations over the next five years—calculated by comparing the yields on inflation-protected bonds and regular ones—have recently fallen as low as 1.2%. Even the Fed’s own forecasts show inflation returning to 1.9-2% only in 2017.

The state of financial markets complicates matters further. Hawks have long worried that low interest rates stoke dangerous asset-price bubbles, by prompting investors to look to riskier assets for higher returns. The Fed is probably more alert to this risk now that unemployment has fallen so low.

Yet the markets also provide reasons for continued caution. The S&P500 is 8% lower than a month ago. Stockmarket falls alone should not much hurt the economy: direct investment in the stockmarket makes up only 14% of household assets and is concentrated among richer folk, who are less likely to rein in spending. But the turmoil has pushed up market interest rates and made it harder for firms to finance investment. An index of financial conditions compiled by Goldman Sachs, a bank, has been creeping up since mid-2014, and spiked in August. The combined effect is the biggest squeeze since 2008, all without the Fed taking any action.

A rate rise would cause a big market reaction, because it is not fully expected. Markets place roughly a one-third probability on it happening. Were Ms Yellen to hold off, she would have time to lay the groundwork for a more predictable rise in December. In recent years, nobody has lost money betting on such a delay. The past, though, is no guide to the future. Just ask a central banker.

0 comments:

Publicar un comentario