Fed Can’t Solve Housing Puzzle Alone

Looser lending standards, not the Fed’s decision to hold rates at zero, may be more important for home sales.

By Spencer Jakab

.

Data on existing-home sales for August are due Monday, and Thursday will bring a reading on sales of new homes for the same month. Photo: David Paul Morris/Bloomberg News

Data on existing-home sales for August are due Monday, and Thursday will bring a reading on sales of new homes for the same month. Photo: David Paul Morris/Bloomberg News“There has never been a better time to buy a home.”

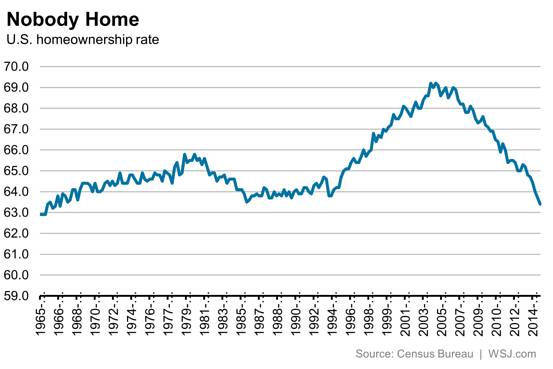

That phrase, or variations on it, can be found in thousands of advertisements from real-estate agents and home builders. While impossible to disprove without the benefit of hindsight, it is safe to say the slogan’s prominent use at the peak of the housing boom was unfortunate. Maybe it was even used during the Lyndon Johnson administration, which was the last time the U.S. homeownership ratio was so low.

With that in mind, it is worth asking whether the Federal Reserve’s decision last week to keep interest rates near zero for a bit longer will give a fillip to home sales. Monday’s data on sales of existing homes for August and Thursday’s release of new-home sales for the same month should shed light on where things were headed before the Fed meeting.

Both have been looking up but remain low historically. Existing sales are closer to normal. July’s annualized figure of 5.59 million was the best since before the crisis and 62% higher than five years earlier.

New-home sales, meanwhile, hovered near their postcrisis high of 507,000 single-family units and have enjoyed a much sharper bounce. Still, they are only around half their pre-housing-boom level on a population-adjusted basis.

Lower mortgage rates might help but are just part of the puzzle. According to an index of housing affordability maintained by the National Association of Realtors, affordability in July sank to the lowest level since 2008. But then, according to the same measure, affordability peaked between 2011 and 2013. Not only were sales of both new and existing homes lower then, but a large chunk of existing sales were to investors rather than individuals.

Equally important though tough to quantify is the ease of getting a mortgage. The Mortgage Lender Sentiment Survey conducted by Fannie Mae in August indicated a significant loosening of conditions.

A case of sales recovering as affordability dropped suggests that, within reason, interest rates take a back seat to credit conditions and pent-up demand. The Fed may not have to worry as much about sabotaging the housing recovery when it finally raises rates.

0 comments:

Publicar un comentario