Demographics - The Real Opponent The Fed Has Been Fighting For Decades

Summary

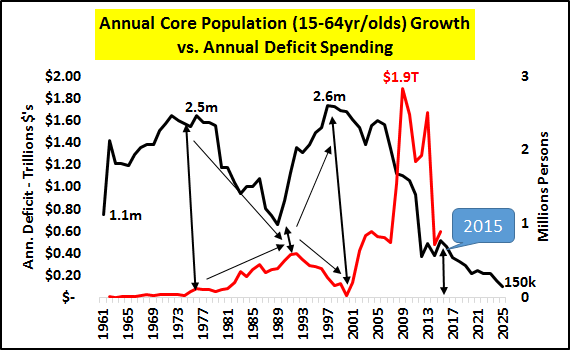

Changes in the growth of the US core 15-64 year old population seem to drive economic activity (growth and recessions). Federal Reserve's FFR changes seem highly correlated with changes to core population.

The Federal Reserve's secular changes to FFR and federal government deficit spending seem highly correlated to the accelerations/decelerations of the core population.

With significant further deceleration of core growth, a given for the next decade, can massive deficits and ZIRP (NIRP?) be the answer to maintain growth? Or is change upon us?

Still, sometimes it's simply finding the right means to communicate something for it to be accepted. I think the charts below do just that.

However, I'm not implying the numbers alone drive anything but it's what they represent. This core segment represents the highest order of consumption and earnings growth. The relatively minor population changes of this group (in comparison to the total population) seems to have impacts that are magnitudes greater than their numbers would imply.

As the chart below shows, periods of increasing core population growth correlate with periods of low federal deficit spending and periods of decelerating core population growth with increasing déficits.

However, the current declines in deficit spending while core population growth remains at historic lows compounded by further core growth deceleration over the next decade (all according to OECD estimates) looks a bit ominous. Either this relationship has been broken, or significantly larger deficits and/or NIRP are upcoming?

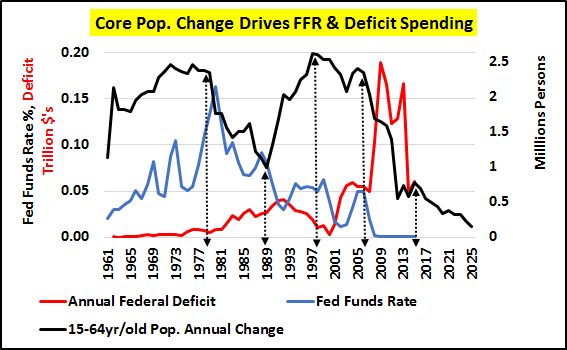

The second chart below adds a third variable; changes in the Federal Funds Rate or "FFR".

The changes in the "FFR" seemingly coincide with secular changes in core population growth, with a year or two lag. The resultant annual federal deficits (absent the rising interest service burdens thanks to the rate cuts) are also highly correlated.

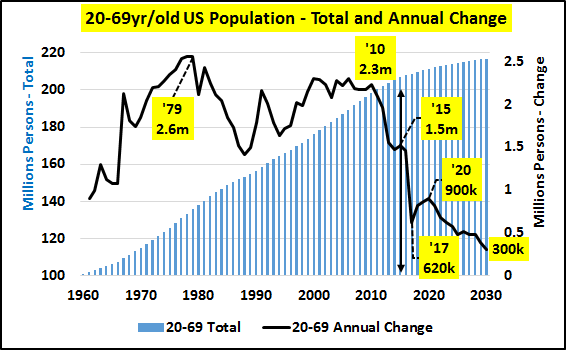

Maybe this focus on 15-64 year olds is a bit unfair, as over time, kids are entering the workforce later and the old are likewise retiring later. So, perhaps a peek at the 20-69 year old population segment is appropriate here. Unfortunately, from this metric (below), there is a triple waterfall from the near high watermark of 2010's population growth. By 2017, the US will be feeling the effects of the second of the three decelerations in population growth, with the final drop beginning around 2020.

Anyone anticipating this slightly older segment to be the savior is likely to be bitterly disappointed.

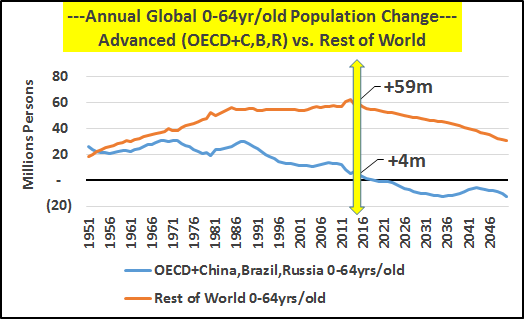

The US demographics are far better than most advanced and many developing nations where outright core shrinkage is and will be a feature for decades. Also unfortunate is the fact that over half of all global 0-64 year old population growth has shifted to the poor of India and even poorer of Africa, and away from the higher income nations of the world. As the chart below highlights, trading high-income for low-income population growth simply will not provide significant new consumption or growth. The chart below is simply showing the changes in the 0-64 year old populations of all 34 OECD members (including the US, Japan, most EU nations, Canada, Australia, S. Korea, etc.) plus China, Brazil and Russia (about 40% of the world's population) vs. "the rest of the world".

Regardless of international considerations, the data shows quite clearly that absent the strong domestic core population growth, US economic activity suffers. The only answers have been FFR cuts and federal deficit spending along with QE and various other consumption-inducing new "tools" since 2008.

Some, including my wife, will ask "so what"? My point is the policies being undertaken by the Federal Reserve and federal government are entirely inappropriate if the intention is the economic (and likely social) well-being of this and future generations. The intelligence or intentions of the Federal Reserve and leadership of the federal government needs to be openly questioned and quite likely entirely replaced. The path chosen by those in leadership was, is, and will be entirely proven a disaster. The fact that population growth wasn't acknowledged as a secular tailwind which, in time, would blow itself out and be replaced by little, no, or negative growth is astonishing. The data has been collected for a reason and the theory the Fed wasn't aware when and how this population shift would occur seems implausible. Those placed in positions of shepherding this nation who either don't know what they are doing, or know but don't care for the ultimate good of the people, must be reconsidered.

It is truly a time to reconsider everything, take the bought and paid for reins of leadership back, and focus the nation's best brain power behind how best to extricate ourselves from the mess we find ourselves. Only by acknowledging the fact that our present leadership has failed us (whether done so unintentionally or otherwise) can we take the first step in rebuilding.

0 comments:

Publicar un comentario