Debt As Far As The Eye Can See

Summary

There is an alarming rise of public and private debt ratios in much of the world; this simply cannot continue like this.

The situation is greatly complicated by low growth and low inflation as we need high nominal GDP growth to stabilize debt ratios.

We look at the sustainability and alternatives to deal with the problem.

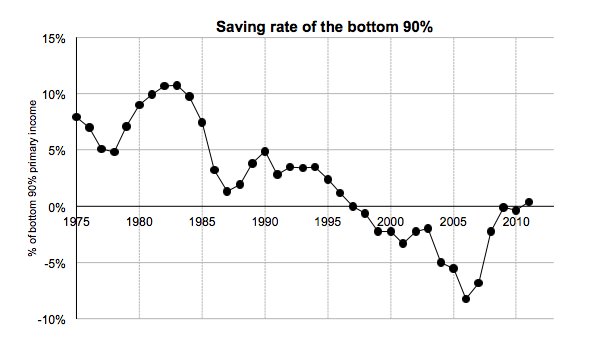

Much of this borrowing binge was financed by mortgage debt, which was very easy to get as banks and other mortgage lenders repackaged loans into inscrutinizable tradable securities which could be offloaded from their balance sheets and shifted to unsuspecting investors.

A big part of why the 2008 financial crisis produced such a big economic crisis is that household balance sheets were ravished, with $9 trillion in assets wiped off, or nearly 40% of household wealth, because of the crash in house prices while the debt remained.

Part of the reason the recovery was a little tepid was because of households trying to repair at least part of that damage to their balance sheets, hence the term balance sheet recession.

Deleveraging occurred, that is, households started to save more and spend less, in order to pay down debt. The increased savings in a balance sheet recession also explains why interest rates are so low and why monetary policy has been relatively powerless. Rather than take up new debt, households prefer to pay-off old debt, no matter how low interest rates are.

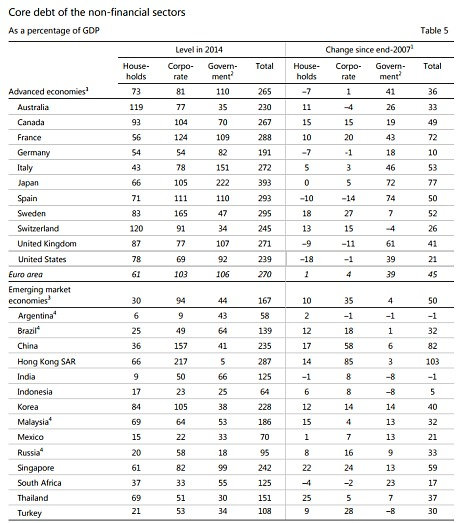

And indeed they did, as you can see in the following table from a BIS study:

A closer look at the table above shows that there really are only a few minus signs, indicating that, by and large, deleveraging has been few and far between.

The private sectors (households and corporate) in the US, UK, Germany and Spain did manage to deleverage, as did the private sector in South Africa. But that's about it. What strikes is the continuous increase in leveraging up at the aggregate (private + public sectors) basically everywhere.

There has been overall deleveraging.

Public sector leveraging, that is, a rise in the public sector/GDP ratio, has gone on unabated (apart from Turkey, India, Indonesia and Switzerland). To a large part, this is a reflection of lower economic growth and inflation affecting tax receipts (more especially in the eurozone).

Part of it isn't so worrying as when private sectors are deleveraging, the slack this creates in the economy has to be absorbed in order to keep the economy afloat, lest it succumbs to a Fisherian debt-deflationary vortex. One should also realize that the public sector is way more creditworthy, so it substitutes high-rate private debt for much lower-rate public debt.

This is Krugman's "debt is good" argument. This isn't a blanket pro-public debt argument, but circumstantial under the present conditions (interest rates at the zero lower bound, lowflation, considerable slack in the economy):

- Public debt can pay for good things like infrastructure, boosting production and the supply side at a time when interest rates are very low.

- Provide safe assets the markets demand and so ward off a destructive scramble for cash.

- Produce upward pressure on interest rates without slowing the economy.

However, it's also clear that this accumulation of debt, whether private or public, simply can't go on forever. There are simply enormous risks attached to that:

- Sudden stop in funding: acute financial crisis.

- The slow debt-deflationary grind, with eurozone countries, especially Italy as a prime example and risk.

- There will be no region left to absorb another shock, as emerging markets (especially China) did after the Lehman crisis.

- There will be no policy instruments left to absorb another shock.

- Problem will escalate when interest rates "normalize".

Financial crisis

The most immediate and biggest risk is that the rising debt will lead to financial crisis. Here is Martin Wolf from the FT:

Ruchir Sharma of Morgan Stanley argues that the 30 most explosive credit booms all led to a slowdown, often a crisis. A rapid change in the ratio of credit to gross domestic product is more important than its level. That is partly because some societies are able to manage more debt than others; it is partly because a sudden burst in lending is likely to be associated with a sudden collapse in lending standards.Indeed, this is what happened before the biggest financial crisis of them all:

In an update of work on debt and deleveraging, McKinsey notes that between 2000 and 2007, household debt rose as a proportion of income by one-third or more in the US, the UK, Spain, Ireland and Portugal. All of these countries subsequently experienced financial crises.In this respect, the 70-point rise in the debt/GDP ratio of China is particularly worrisome, not only in and of itself, but also for other aspects as well:

- China's economy is slowing down, which could lead the authorities to open the credit floodgates once more.

- Capital is flowing out of China, which is a worrying sign in and of itself, but it also automatically tightens domestic monetary conditions (the result of the PBOC buying its own currency in order to support it), which could lead to strains and default of debtors. Luckily a full-blown banking crisis isn't very likely in China as these are state owned or backed.

Capital outflows sink their currencies, which increases the (largely private sector) debt value in domestic currency. It forces selling foreign currency reserves, tightening domestic monetary conditions, which slows their economies further.

Many of these economies are already in trouble as a result of reduced demand for commodities and the subsequent crash in commodity prices. Such are the problems in emerging countries that it even prompted the Fed to hold off interest rate rises, given that emerging markets are now half of the world economy and provided it with much of the economic growth post Lehman.

While foreign currency levels are generally considerably higher and governments have borrowed less in dollars, another emerging market crisis like the Asian crisis or the Russian crisis of the 1990s cannot be excluded.

We are especially concerned about China, not because we think that it will suddenly implode, but simply because its size and its nexus to commodities and financial flows makes it especially important for the health of the world economy.

If and when the Fed does decide to tighten monetary policy, the fallout in emerging markets could be considerable, given that they already suffer from capital outflows and sinking currencies. This could easily accelerate when US money is repatriated on higher rates and dollar appreciation expectations.

We're hardly alone in pointing out the problems here (per CNBC):

The U.S. Federal Reserve risks triggering "panic and turmoil" in emerging markets if it opts to raise rates at its September meeting and should hold fire until the global economy is on a surer footing, the World Bank's chief economist has warned.The IMF has issued similar warnings, and the Fed has obliged.

The slow grind

There is another, less visible, but equally disturbing debt crisis, which is mainly the result of low growth and "lowflation." This pincer produces a ratcheting up in debt ratios through the "denominator" effect (where debt/GDP increases as a result of stagnant nominal GDP).

The prime example here is Italy, and this is a dangerous situation (as we explained in much greater detail here) because:

- Italy's public debt ratio is already very high at 130%+ of GDP.

- Italy isn't the master of its own currency; its debt is basically in a foreign one over which it has no control.

- Italy has few instruments at its disposal to revert the situation; it's unable to reflate by monetary, fiscal, or currency means.

The next slowdown

There isn't much room for countercyclical policies when economies which already experience high public debt levels and zero interest rates face another recession.

We were quite lucky that emerging economies (very much including China) buffered the economic impact of the 2008 financial crisis, being responsible for most of world output growth since. However, there doesn't seem to be a region left that could absorb or at least mitigate another economic shock.

Private debt

Many blame the debt explosion on public sector largesse. However, here is Martin Wolf of the FT again:

Start with the sources of vulnerability. In economies with liberalised financial sectors, the driver towards disaster is far more often private than public imprudence.Now, many then blame the Fed for the low interest rates, but as we argued extensively (here), the rates that matter most (bond yields) have been low with or without the Fed, and the Fed has limited influence over these in any case.

If there was any doubt about this, then the introduction and end of massive QE programs demonstrated this point with force. Rates haven't collapsed as a result of asset buying and neither have they exploded when these were stopped.

This doesn't mean that public authorities and central banks can be entirely exonerated from the rising debt binge. While we firmly believe that interest rates should be set with respect to the state of the economy, authorities can do a lot to prevent debt bubbles from emerging:

- Fiscal policy should be countercyclical, that is, during boom times debt should be repaid.

- Central banks shouldn't hesitate to intervene with macroprudential policies where credit growth is excessive.

How to deal with the debt?

Historically, high debt levels have either been written off, or the real burden of debt has been eroded by a steady dose of mild inflation and economic growth. The latter increases nominal GDP, which is probably the least painful way to reduce real debt burdens.

Write-offs might still happen in isolated cases (Greek public debt?), but it's the growth of nominal GDP that seems to be lacking. The problem here is that in order to get higher growth, most countries have relied on monetary policy. However, this hasn't been very successful. See for instance the massive actions taken by the Japanese central bank, the BoJ, which hasn't been able to break Japan free from deflation.

That might still happen, as the tax hike and the commodity crash have considerably complicated things for Japan, but it shows how difficult it is in the present circumstances to create nominal growth.

Inflation is also very low in the US and the eurozone, and one has to keep in mind that inflation doesn't actually have to be negative to produce the damaging debt dynamics and other problems (per the IMF). Considering the difficulties of creating even some inflation, there is an increasing chorus of economists that argue for something bolder, especially if the world plunges into another recession and/or deflationary bout.

The bold policy is "helicopter money," an old idea from Milton Friedman (borrowing from an older Chicago tradition) where central banks directly finance public expenditures or tax cuts (or both). It has the advantage over QE as it injects money directly into the veins of the economy, rather than depending on financial markets or the creation of new debt.

We also know it works; this is mainly how Japan got out of the depression in the 1930s. It is also more likely to create the growth and mild inflation as to stabilize, and even starting to dent the existing debt mountains. However, it's not without risk. It compromises central bank independence and inflation can get out of hand.

The latter isn't a serious risk as interest rates can be increased and/or the bond portfolios of central banks (product of earlier QE policies) can be sold off. The main risk is politicians getting used to free money, so the instrument should be firmly in hands of the central bankers, deciding on quantities.

And, of course, like any policy avenue, its effectiveness, advantages and disadvantages should be judged against real-world alternatives. The real world alternative is low growth, lowflation, and ever increasing debt levels.

Conclusión

Much of the world is drowning in debt. In the present economic environment of modest (and decelerating) growth and lowflation, this is likely to get worse, not better. The only alternatives seem to be debt write-offs and/or some form of direct monetary financing of spending. Bold, yes, but there isn't much of an alternative.

0 comments:

Publicar un comentario