Summary

- The market continues to hold its own despite dismal revenue and earnings growth so far in 2015.

- Equities are being buoyed by massive "financial engineering" on myriad fronts. However, the levels of current valuations have to be making value and fundamental investors a bit squeamish.

- Despite massive financial engineering supporting equities at this time, the fundamentals of the market are telling me this is a time for caution - not greed.

Chinese stocks also had big rally, but that had more to do with intervention from Chinese authorities than any change in direction for the fundamentals or economy in the Middle Kingdom. Today, markets were set to open much lower as the same Chinese authorities have decided to officially to devalue their currency to make their exports more competitive.

This is understandable from a couple of points of view. The yuan has lost some 10% against the euro since the European Central Bank started its own quantitative easing program late in the first quarter of this year. This has been a key factor in the dismal readings coming from China's export sector, where exports were reported as being down 8% year over year in the last report month. Imports were down even further, so the trade balance with the rest of the world still grew. But these negative readings leads to me to doubt China is growing anywhere near their "official" 7% GDP growth target. I think leadership knows this as well, which helps explain this latest currency move and the extraordinary measures taken to keep their stock market from falling any further.

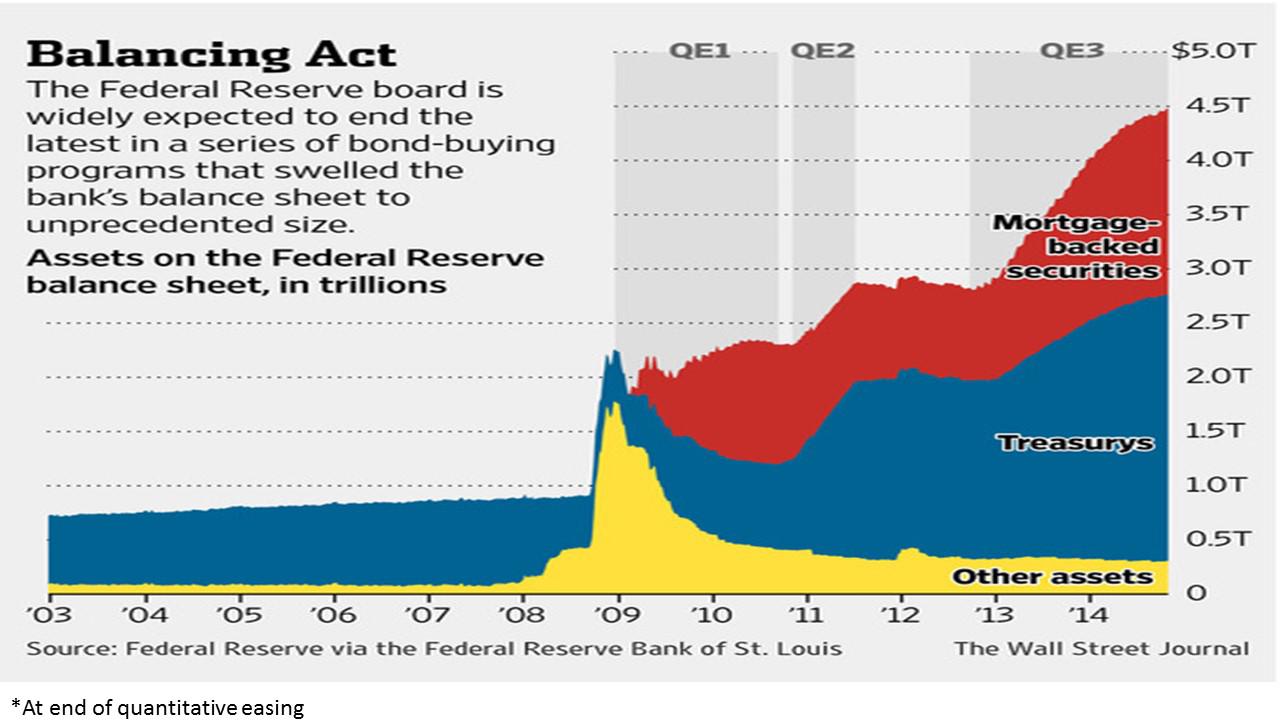

I think I must be getting old. I vaguely remember a time when the market was driven by such trivial things like earnings and revenue growth, valuation, and the prospects for accelerating GDP growth. It seems that since the financial crisis, the main focus has been on what this or that central bank may or may not do in the near future.

(click to enlarge)

Certainly, the liquidity provided by these institutions has been a key factor in driving up asset values all over the world -- whether in global stock markets, real estate, or even the art market.

It certainly has not been the economy, which has been stuck in the 2% growth range over the past six years. Europe and Japan have performed even worse despite the best efforts of their central banks.

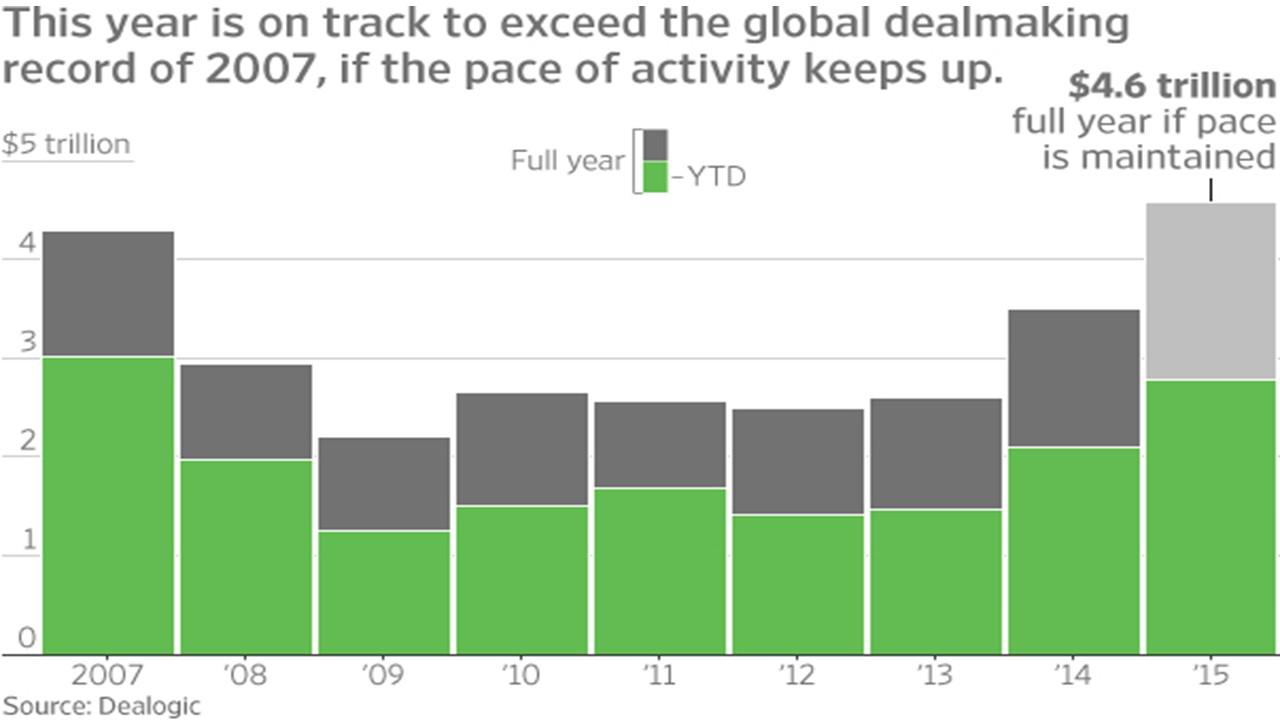

The "financial engineering" driving the market has now extended into the private sector.

Global M&A levels are expected to come in at just under $4.6 trillion at current run rates for 2015. This would be $300 billion over 2007's peak levels, which not coincidentally marked the last top of the cycle in the market.

(click to enlarge)

Buoyed by low financing rates and the dearth of any organic growth opportunities, I expect M&A levels to be robust until something causes the music to stop. Even the Oracle of Omaha can't resist a big deal as Berkshire Hathaway (NYSE:BRK.A) snapped up Precision Castparts (NYSE:PCP) for better than a 20% premium on Monday. At over $37 billion, it was by far Buffett's largest purchase ever. Venture capital funding levels in 2015 are also at levels not seen since just before the Internet bust. For instance, Uber (Pending:UBER) was recently valued at over $50 billion during its last funding round, despite generating less than $500 million in revenues over the prior 12 months and being years away from being profitable.

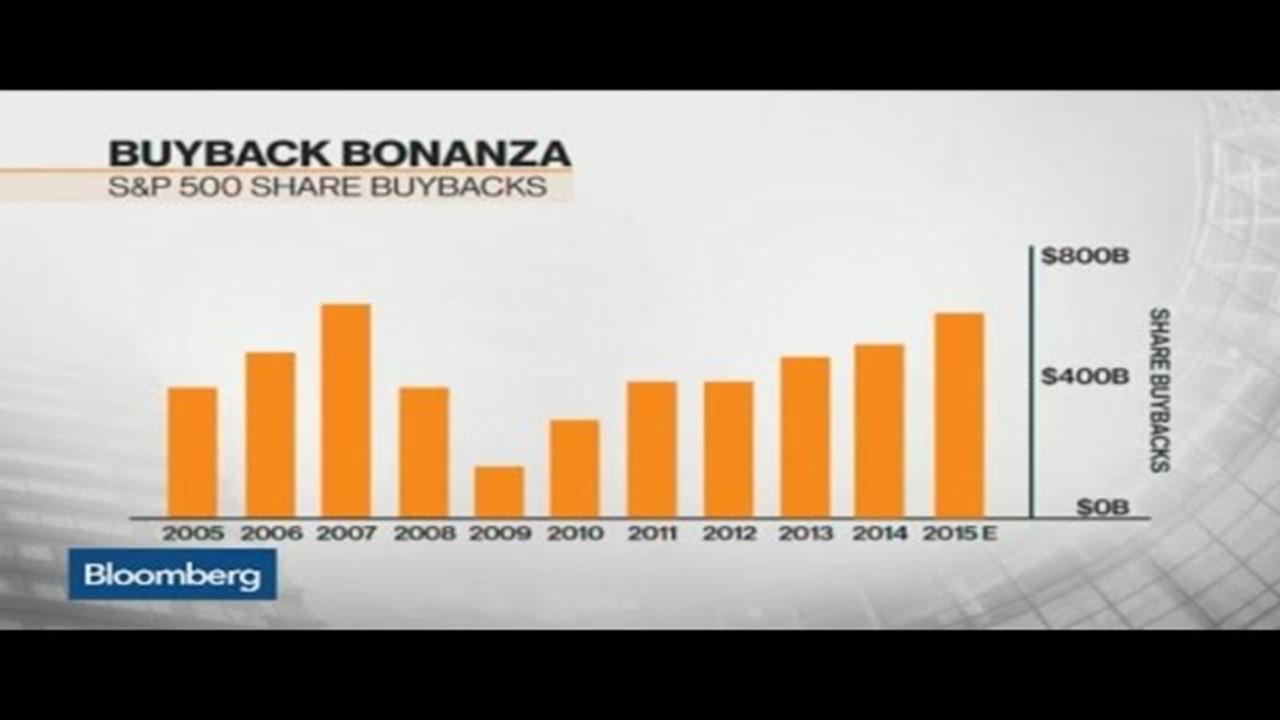

Not to be left out, corporations are spending record amounts on stock buybacks with over $140 billion in stock repurchase authorizations announced in April alone. This is happening even as business investment levels remain tepid, a key factor behind an economy that continues to struggle to achieve more than 2% growth. As can be seen below, the number of buybacks expected to executed in 2015 is rapidly approaching 2007's peak levels.

(click to enlarge)

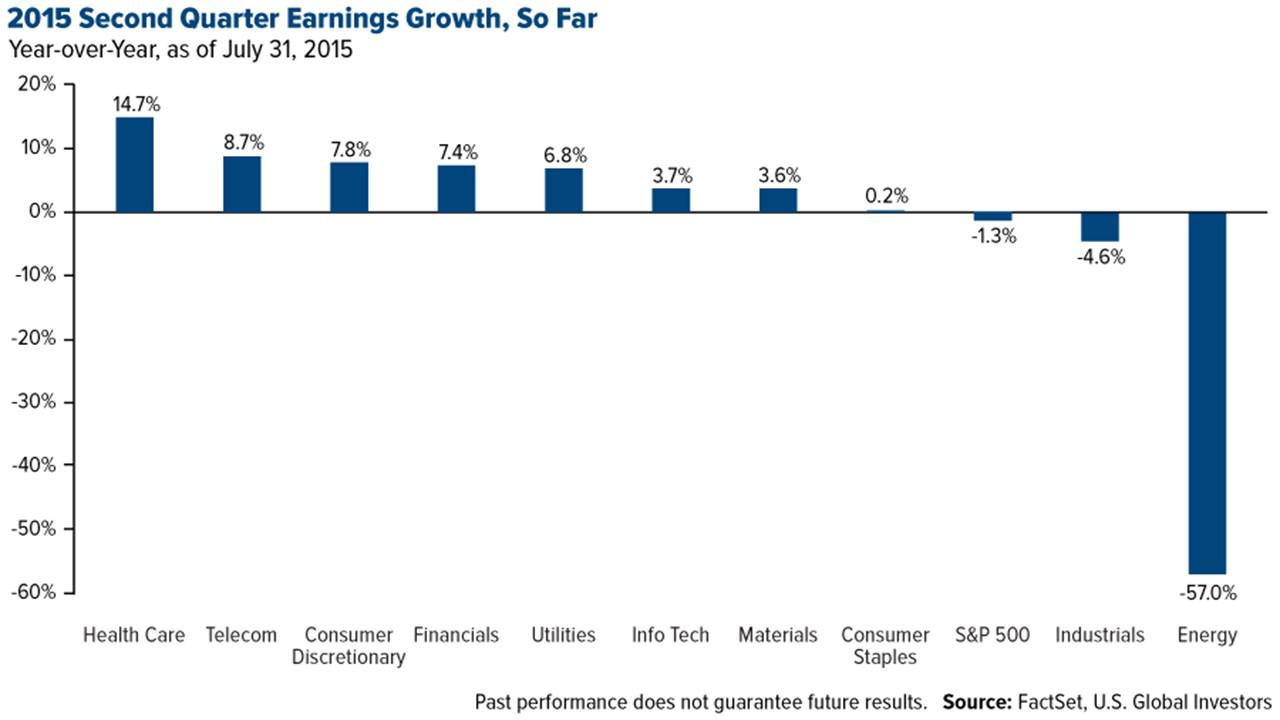

These levels of various forms of "financial engineering" have managed to keep the market just above flat line for 2015, which is by far equities' worst annual performance since the recession ended in 2009. However, if an investor actually looks at the fundamentals of the market right now, it is hardly encouraging. Revenues year over year are down for the S&P 500 so far in the first two quarters of 2015.

(click to enlarge)

Earnings are slightly down this quarter, helped even as they have been helped considerably by stock buybacks as the collapse in profits in the energy sector and a poor performance from industrials take their toll. Equities basically trade at the same ~18 times trailing earnings that they did to start the year, as there has been no earnings growth. Factset thinks these dismal earnings numbers will persist into the third quarter as well, with its forecast of an approximate 2% year-over-year decline in profits in the upcoming quarter.

It's hard to get excited about the market given these poor fundamentals, despite the robust financial engineering that is continuing to support the market. I continue to lean toward the cautious side and have some 30% of my portfolio in cash, as it's hard to see the market breaking out through year-end -- and the danger of a 10% correction seems to be increasing by the day. I will use any significant dips in the market to incrementally put some of my "dry powder" to work if that decline does occur. My strategy for this deployment will be pretty much along the lines of what I plan to do in the biotech sector, which I outlined the other day.

I wish I could be more sanguine on the market. However, despite massive financial engineering from myriad sources, the fundamentals of the market are telling me this is a time for caution, not greed.

0 comments:

Publicar un comentario