Wells Fargo: Banking Is a Drag, Drag, Drag

Second-quarter results from Wells Fargo show the continued toll of superlow interest rates

By David Reilly

July 14, 2015 12:21 p.m. ET

Like every other bank, Wells can’t fight the superlow interest-rate environment brought about by the Fed. Above, a Wells Fargo sign in California. Photo: Justin Sullivan/Getty Images

Like every other bank, Wells can’t fight the superlow interest-rate environment brought about by the Fed. Above, a Wells Fargo sign in California. Photo: Justin Sullivan/Getty Images Even the strongest swimmers have a tough time pulling against the tide. That is especially true in banking, as Wells Fargo ’s second-quarter earnings show.

Wells is highly regarded by investors among big U.S. banks. This is due to confidence in its management, its crisis track record, its U.S.-focused business and the fact that, while huge, it is seen as the least too-big of the too-big-to-fail banks, thanks to a small derivatives book. For all that, Wells has been rewarded with the highest valuation of the big six U.S. banks.

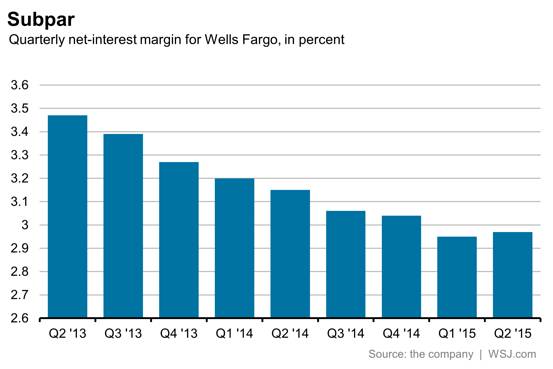

Even so, like every other bank, Wells can’t fight the superlow interest-rate environment brought about by the Federal Reserve. Although the era of near-zero rates is likely to come to an end later this year, it has taken a toll on banks. This is seen in the grinding down of Wells’ net interest margin, or the difference in what it makes borrowing and lending money. Although this stabilized in the second quarter, it remains below 3%, an unusual occurrence for Wells.

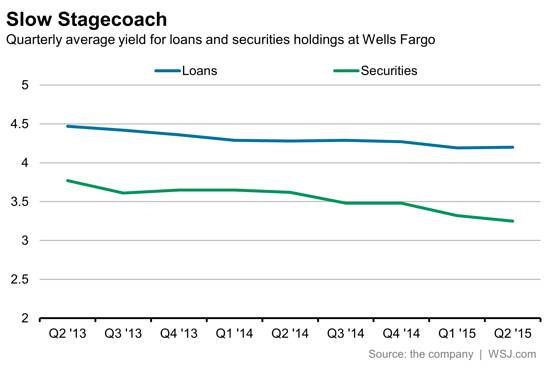

The net interest margin is hit by a combination of factors. First, superlow yields mean Wells, like other banks, is lending money at lower rates. And it is also reinvesting maturing debt securities at lower levels as well. Meanwhile, with its funding costs already at rock-bottom levels, it can’t get that side of the equation lower. And that is how it and other banks get squeezed. This is happening even as Wells, like other banks, is trying to lend more. Indeed, its loan book has grown by nearly 10% over the past two years to about $870 billion at the end of the second quarter. But that isn’t enough to make up for the lower yields and increased competition among lenders that also keep pressure on pricing.

And lower net interest margins along with a tougher overall banking environment have taken a toll on Wells Fargo’s return on equity. Although this is still above its theoretical cost of capital of about 10%, the return has been whittled down. The most recent quarter marked the second out of the past three where the return was below 13%.

Fortunately for Wells Fargo, higher interest rates will cause its horses to gallop. The prospect of a move by the Fed later this year already has caused the stock to outperform this year. Wells Fargo’s shares are now trading at their highest level relative to the S&P 500 in the past three years. The trick in the coming two quarters, will be to post performance that warrants this. Otherwise, that outperformance may not last.

0 comments:

Publicar un comentario