The Big Mac index

A few dollars less

Our burger benchmark finds that the greenback is too dear

Jul 18th 2015

.

IN NOVEMBER the McDonald’s restaurant in Pushkin Square in Moscow reopened following a three-month closure ordered by local health inspectors. The penalty was widely seen as retaliation for Western sanctions against Russia. The restaurant was a predictable target.

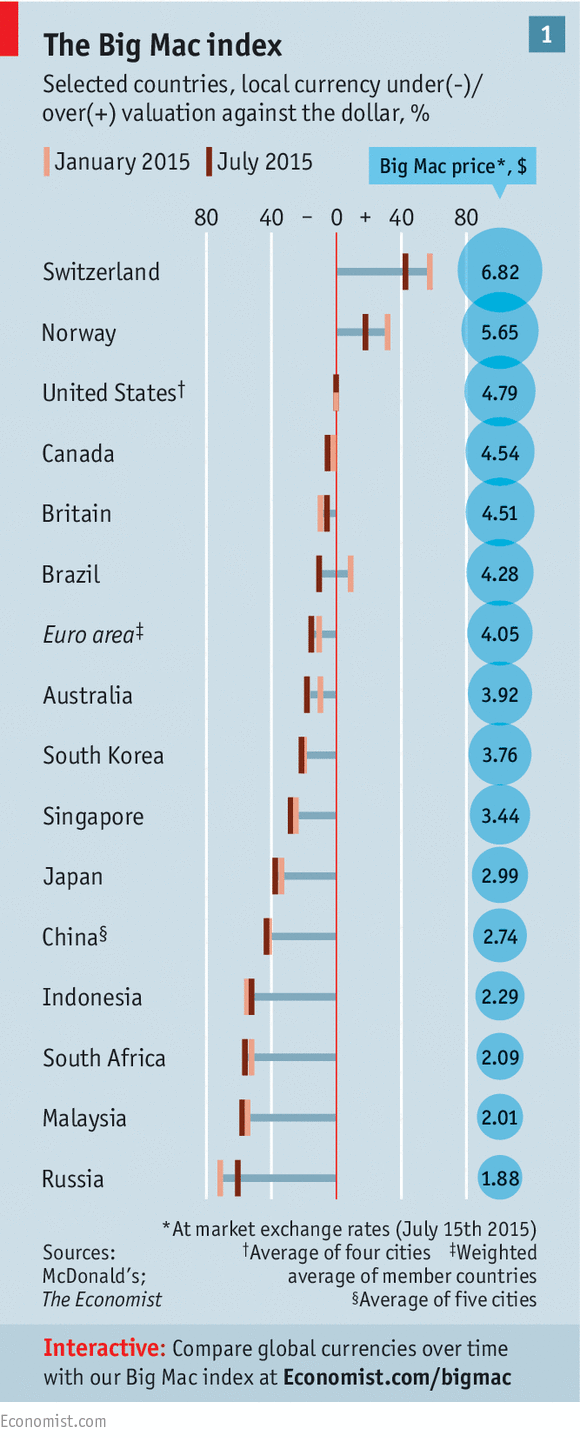

When it first opened in 1990, it symbolised the triumph of American capitalism over a crumbling Soviet Union. Now it holds up a mirror to another American economic victory: the resurgence of the dollar. All but four currencies in our Big Mac index look cheap compared to the greenback. The rouble is the cheapest of all.

The index is based on the idea of purchasing-power parity, which says exchange rates should move towards the level that would make the price of a basket of goods the same in different countries. Our basket contains just one item: a Big Mac hamburger. If the local cost of a Big Mac converted into dollars is above $4.79 (its price in America), a currency is dear; if it is below the benchmark, it is cheap. In Pushkin Square a Big Mac costs 107 roubles, or $1.88 at the current exchange rate, two-fifths of the average price in four American cities. That in turn implies that the rouble is undervalued by 61% (see chart 1).

Purchasing-power parity holds only in the long run. Over shorter periods, currencies are often pushed far away from such fair-value yardsticks by international capital flows, which in turn are driven by broader trends in the global economy. Exchange rates are currently being buffeted by the euro crisis, the growing likelihood of a rise in interest rates in America, China’s slowing economy and the sharp drop in the oil price, one of the drivers of the rouble’s slump.

By showing how much these forces have driven different currencies off course, the Big Mac gives a flavour of what may be to come.

Start with the dollar’s revival. It began in earnest in May 2013 when Ben Bernanke, the chairman of the Federal Reserve at the time, dropped a hint that the Fed’s purchases of bonds using newly minted money (“quantitative easing” or QE) might soon tail off. The prospect, however distant, of higher interest rates in America prompted a sell-off in emerging-market currencies. As the Fed moved slowly towards a tighter monetary stance, policy became looser in other rich economies. The yen is 38% below its fair value in burger terms, in large part because of the Bank of Japan’s expanding QE scheme. When the European Central Bank eventually resorted to QE, the euro dropped like a stone from $1.30 to $1.05. It has since rebounded to $1.10, but that still leaves it 15% undervalued on the Big Mac gauge.

.

Yet the dollar’s broad-based rise appears to have run out of steam. It ticked up against the euro and yen on July 15th after Janet Yellen, the Fed’s new boss, told Congress that interest rates were likely to rise later this year, as expected. But she also said that the pace of interest-rate increases would be gradual. The Fed’s caution will probably prevent the dollar rising much further, at least against the main currencies of the rich world. Japan’s current-account surplus is growing thanks to burgeoning income from the country’s huge holdings of foreign assets, according to analysts at Morgan Stanley. The euro area’s large current-account surplus is a similar bulwark against further depreciation. “It can’t keep on going down every day on the back of bad news that everyone expected,” says Kit Juckes of Société Générale, a bank.

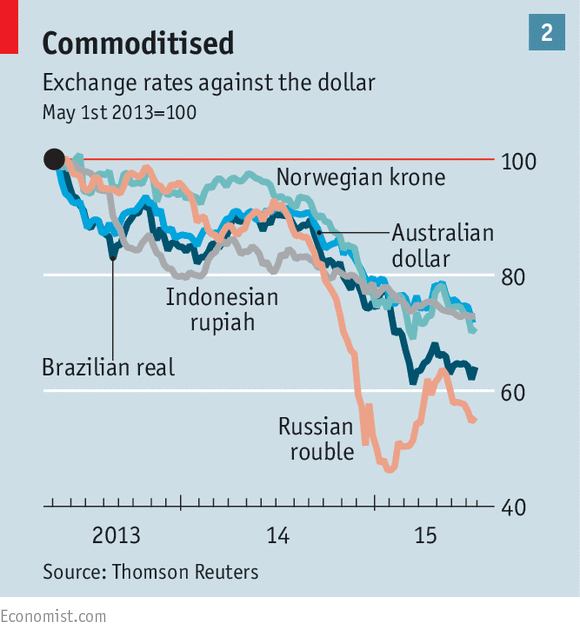

For emerging-market currencies, cheap Big Macs are not necessarily a sign of an impending appreciation. That is because the cost of a burger depends partly on untradeable inputs, such as rent and wages, which tend to be lower in poor countries (gauges based on purchasing-power parity work best when comparing countries with similar income). But not all emerging markets are equal: the countries whose currencies have fallen furthest recently are commodity producers. In fact, China’s waning hunger for raw materials is afflicting rich and poor exporters alike (see chart 2).

.

The prices of oil and of some industrial commodities, such as iron ore, are falling again. That leads to cuts in investment and weaker GDP. The debts run up to pay for mines and wells also look more onerous. Brazil is a big commodity exporter, and the real looks overvalued relative to its peers, but Brazil’s high interest rates make it costly for speculators to sell it short and are a lure to yield-hungry investors. The Malaysian ringgit, in contrast, is second only to the rouble in terms of value on our gauge. Yet it is likely to get cheaper still, reckons George Papamarkakis of North Asset Management, a hedge fund, because of its exposure to raw materials and because lots of flighty foreign investors own Malaysian bonds. The Canadian dollar is close to fair value on the Big Mac index but it should perhaps be cheaper. A slump in the country’s oil-sands industry, among other ills, prompted the Bank of Canada to cut interest rates to 0.5% on July 15th.

Eventually currencies that have fallen hard will become cheap enough to attract buyers. There is a price for everything—even currencies such as the South African rand and the Russian rouble, which investors currently see no merit in. Who can resist a 60% discount?

0 comments:

Publicar un comentario