“Lowflation” forever in the US?

Gavyn Davies

Jul 26 15:38

Although inflation in the US has been low and stable for many years, it still tends to dominate policy discussions at the Federal Reserve. At Janet Yellen’s latest press conference, “inflation” was mentioned 40 times, while “unemployment” or “employment” were mentioned 28 times. Both sides of the dual mandate are obviously given great attention, but many observers think that the Fed is too conservative in its approach to inflation, while refusing to take any risks to stimulate employment or output growth.

This judgment about the balance of risks is coming to a head now that the FOMC seems fairly likely to announce lift off for US interest rates in September. The GDP growth rate, and the strengthening in the labour market, seem consistent with an early rate rise. But the inflation rate remains well below the Fed’s 2 per cent target for headline PCE inflation, and the FOMC says it needs to be “reasonably confident” that inflation will return to target over the medium term before they can raise rates.

The FOMC will release its next policy statement on Wednesday. Since its last meeting in June, reported inflation data have barely changed, but there has been a drop of about 19 per cent in the price of oil, and a rise of about 2 per cent in the dollar exchange rate. These two variables were specifically identified when the Fed decided to delay interest rate rises earlier in the year, and the fixed income markets are beginning to think that the same might happen again in the run up to the September meeting.

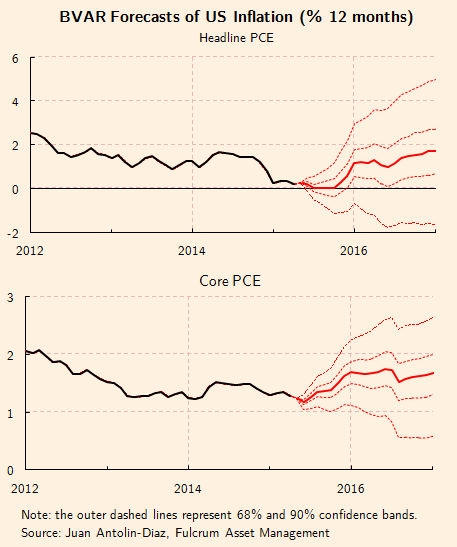

In the last 12 months, fluctuations in headline inflation have been driven almost entirely by the collapse in oil prices and the uptrend in the dollar. Core inflation has been less affected, but has not been entirely immune from these oil and dollar effects. My colleagues at Fulcrum have estimated a VAR model that tracks the effects of oil and the dollar on reported inflation, and we use this model to predict the future path for inflation, given the recent renewed decline in oil prices (which was not built into the Fed’s June forecast). Here are the results:

This model is not suitable for analysing long-term shifts in underlying inflation because it does not include deep fundamentals like the state of the labour market, and the formation mechanism for inflation expectations. But it should do a reasonable job in making short-term predictions when the oil price and the dollar are moving a great deal, as they are now.

The model suggests that headline PCE inflation will remain around zero until October, 2015 and will then rise to almost 2 per cent by the end of 2016 (mainly because the oil price is expected to stop falling). The core PCE inflation rate, meanwhile, rises gradually from its current level of 1.2 per cent, reaching 1.4 per cent in September and 1.6 per cent at the end of 2015, staying there for much of 2016.

The issue is whether these subdued paths for headline and core inflation are sufficient to enable the FOMC to say that it is “reasonably confident” that inflation is returning to target. On balance, I expect that they will be.

Lately, Janet Yellen has openly accepted that headline inflation will stay close to zero for a while, saying that this is due to temporary oil and dollar effects. So she is unlikely to be surprised by headline inflation prints close to zero during the summer. Meanwhile, she has focused very specifically on the strengthening in the labour market, and not on actual inflation data, as the key for policy:

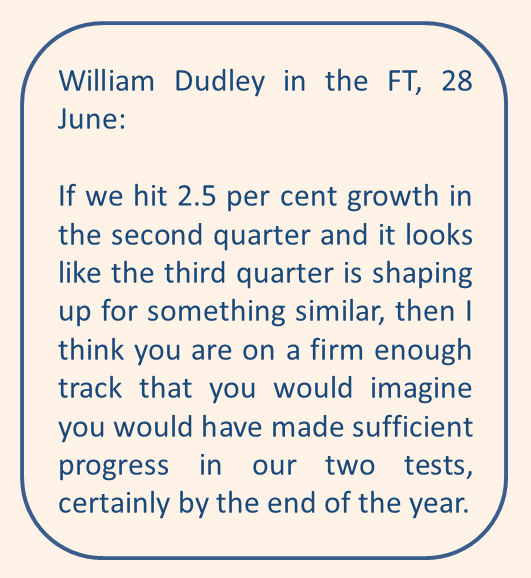

Elsewhere, other important members of the FOMC like William Dudley have also suggested that they will become more confident about a September rate increase if real GDP continues to grow at about the 2.5 per cent rate that has been in place since the spring. All this suggests that it is reported economic activity and employment releases, rather than the next few months of inflation data, that will critically influence the Fed’s decision in September.

This raises one more question, which is why the Fed considers the labour market to be so important in determining future inflation, given the fact that there has been relatively little connection between them for many years now. A clue to this came in the embarrassing and unintended release of the Fed staff ‘s economic forecasts after the June FOMC meeting.

These forecasts, which are usually kept confidential for five years, showed that the Fed’s economic staff believes that the output gap is now very narrow, at only 1.04 per cent, and that it will disappear almost entirely in 2016. This is based on their estimate that the natural rate of unemployment is 5.2 per cent, only 0.1 per cent below today’s actual unemployment rate.

Furthermore, the staff believes that potential output growth is now only 1.6 per cent, which is well below the current GDP growth rate in the economy. In other words, economic slack is disappearing fast and, on this assessment, the US will not achieve “lowflation forever” unless GDP growth slows down, and unemployment stops falling, in the near future.

It is clear that this unexpectedly pessimistic assessment of the supply side of the economy is the main reason why FOMC members believe that an increase in rates will shortly be necessary. Admittedly, the staff’s economic forecast shows that GDP growth will slow to an average of only 2 per cent after 2016, and they expect that this anaemic growth rate will keep inflation within the 2 per cent target. They also believe that this slowdown will be achieved with only one rate rise this year and with a lower trajectory for rates over the next three years than appears in the FOMC’s famous “dots” plot.

But the “dots” show the view of the official policy makers on the FOMC and they seem to believe that more insurance is needed to maintain a “lowflation” outcome, given the weakness of the supply side in the US economy.

It is the FOMC members more hawkish view, not the staff’s interest rate forecast, that ultimately counts for policy decisions

This judgment about the balance of risks is coming to a head now that the FOMC seems fairly likely to announce lift off for US interest rates in September. The GDP growth rate, and the strengthening in the labour market, seem consistent with an early rate rise. But the inflation rate remains well below the Fed’s 2 per cent target for headline PCE inflation, and the FOMC says it needs to be “reasonably confident” that inflation will return to target over the medium term before they can raise rates.

The FOMC will release its next policy statement on Wednesday. Since its last meeting in June, reported inflation data have barely changed, but there has been a drop of about 19 per cent in the price of oil, and a rise of about 2 per cent in the dollar exchange rate. These two variables were specifically identified when the Fed decided to delay interest rate rises earlier in the year, and the fixed income markets are beginning to think that the same might happen again in the run up to the September meeting.

In the last 12 months, fluctuations in headline inflation have been driven almost entirely by the collapse in oil prices and the uptrend in the dollar. Core inflation has been less affected, but has not been entirely immune from these oil and dollar effects. My colleagues at Fulcrum have estimated a VAR model that tracks the effects of oil and the dollar on reported inflation, and we use this model to predict the future path for inflation, given the recent renewed decline in oil prices (which was not built into the Fed’s June forecast). Here are the results:

This model is not suitable for analysing long-term shifts in underlying inflation because it does not include deep fundamentals like the state of the labour market, and the formation mechanism for inflation expectations. But it should do a reasonable job in making short-term predictions when the oil price and the dollar are moving a great deal, as they are now.

The model suggests that headline PCE inflation will remain around zero until October, 2015 and will then rise to almost 2 per cent by the end of 2016 (mainly because the oil price is expected to stop falling). The core PCE inflation rate, meanwhile, rises gradually from its current level of 1.2 per cent, reaching 1.4 per cent in September and 1.6 per cent at the end of 2015, staying there for much of 2016.

The issue is whether these subdued paths for headline and core inflation are sufficient to enable the FOMC to say that it is “reasonably confident” that inflation is returning to target. On balance, I expect that they will be.

Lately, Janet Yellen has openly accepted that headline inflation will stay close to zero for a while, saying that this is due to temporary oil and dollar effects. So she is unlikely to be surprised by headline inflation prints close to zero during the summer. Meanwhile, she has focused very specifically on the strengthening in the labour market, and not on actual inflation data, as the key for policy:

So I think we need to see additional strength in the labor market and the economy moving somewhat closer to capacity—the output gap shrinking—in order to have confidence that inflation will move back up to 2 percent, but we have made some progress (June FOMC press conference).This indicates that the FOMC will be willing to announce lift off even in the presence of very low inflation prints, provided that the labour market continues to improve.

Elsewhere, other important members of the FOMC like William Dudley have also suggested that they will become more confident about a September rate increase if real GDP continues to grow at about the 2.5 per cent rate that has been in place since the spring. All this suggests that it is reported economic activity and employment releases, rather than the next few months of inflation data, that will critically influence the Fed’s decision in September.

This raises one more question, which is why the Fed considers the labour market to be so important in determining future inflation, given the fact that there has been relatively little connection between them for many years now. A clue to this came in the embarrassing and unintended release of the Fed staff ‘s economic forecasts after the June FOMC meeting.

These forecasts, which are usually kept confidential for five years, showed that the Fed’s economic staff believes that the output gap is now very narrow, at only 1.04 per cent, and that it will disappear almost entirely in 2016. This is based on their estimate that the natural rate of unemployment is 5.2 per cent, only 0.1 per cent below today’s actual unemployment rate.

Furthermore, the staff believes that potential output growth is now only 1.6 per cent, which is well below the current GDP growth rate in the economy. In other words, economic slack is disappearing fast and, on this assessment, the US will not achieve “lowflation forever” unless GDP growth slows down, and unemployment stops falling, in the near future.

It is clear that this unexpectedly pessimistic assessment of the supply side of the economy is the main reason why FOMC members believe that an increase in rates will shortly be necessary. Admittedly, the staff’s economic forecast shows that GDP growth will slow to an average of only 2 per cent after 2016, and they expect that this anaemic growth rate will keep inflation within the 2 per cent target. They also believe that this slowdown will be achieved with only one rate rise this year and with a lower trajectory for rates over the next three years than appears in the FOMC’s famous “dots” plot.

But the “dots” show the view of the official policy makers on the FOMC and they seem to believe that more insurance is needed to maintain a “lowflation” outcome, given the weakness of the supply side in the US economy.

It is the FOMC members more hawkish view, not the staff’s interest rate forecast, that ultimately counts for policy decisions

0 comments:

Publicar un comentario