2015 Second Half Outlook: Quadrophobia

Jun. 29, 2015 5:55 PM ET

Summary

- The second half of 2015 promises to deliver an interesting ride for investors.

- After what was a relatively quiet first half, the capital markets are being confronted with a mounting set of challenges as we enter the back half of the year.

- At least four critically important issues have risen to the forefront for global investors to navigate as we progress through the remainder of the year.

Greece And The Eurozone

The second half of the year is getting underway with a livewire of a problem in Greece and its standoff with European creditors. Given that the unfolding dilemma in Greece has been well documented in a variety of sources, including several of my own recent articles, I will instead focus on the longer-term implications of the currently unfolding situation after a brief summary. Basically, Greece has the unsustainable problem of too much debt and insufficient growth to overcome these high and rising debt levels. The country has been reliant on support from European creditors in the eurozone to avoid default, but its new Syriza leadership has balked on accepting further austerity in order to receive more bailout funds. As a result, default and a potential departure from the eurozone are now presenting themselves as real possibilities for Greece.

The Greece situation alone leads to a quadruple dilemma for investors as we enter the second half of the year. The first is that negotiations remain ongoing. It is still very possible that Greece and its European creditors could end up striking a deal in the coming days, even though it appears that the clock is already striking midnight. The next critical date is July 5, when the Greece citizens vote on a referendum whether to accept or reject the austerity measures proposed by its European creditors. But even if Greek voters accept the deal and reject their Syriza leadership in the process, this does not mean that the Greece problem is solved and all is well. The country is sinking fast under the weight of its own debt. And while a deal may put the problem off until another day, the problem is only likely to be worse and more complex once that day finally arrives.

But suppose Greek voters reject austerity. This leads to the second dilemma for investors. Yes, European policymakers have been preparing for the last several years for the day when Greece finally defaults. And while policymakers may think that they have isolated the Greece problem and have constructed adequate firewalls around other at-risk eurozone members, we will not know what the true fallout effects will be once the event finally happens. For it is typically the unanticipated surprises that can shock capital markets into a correction. Such will be the persistent risk for investors for weeks and months after the fact.

The third dilemma for investors is that with Greece gone, the focus of the problem will naturally move up the line to the next at-risk segments. Portugal stands as the next logical target in line, but the much larger eurozone members in Italy and Spain are also in queue. These countries are not so neatly quarantined as Greece is today. And in the case of Italy and Spain, these are much larger economies with considerably larger debt burdens that will be far more difficult to contain if the situation begins to unravel. Thus, the risk monitoring process promises to become far more complex in the months ahead, regardless of how the situation in Greece plays out.

Lastly, what will be the potential allure for these at-risk nations to follow Greece and bolt from the eurozone at the end of the day? As of today, they all proclaim to varying degrees that they still want to be a part of the euro currency experiment. But what has been increasingly notable over the last several years is the drift toward separation across the region. This has included the rise of Podemos in Spain and other more fringe-oriented political parties across the European Union. It has also included referenda in the United Kingdom for Scotland's independence and ongoing British membership in the European Union. Such separatist inclinations are particularly problematic, for an economic and currency union requires a shift toward unity, not separation. With this in mind, suppose Greece decides to go its own way and leave the eurozone. And what if Greece's economic experience is better than expected? With the precedent now set for a country to leave the currency union, which country might next be inclined to follow?

These varying and complex issues are likely to unfold at different times and speeds as we progress through the second half of 2015 and into 2016. But these are problems that are not likely to go away, and instead, are likely to build.

The investment implications of the unfolding situation in Europe is the following. It is supportive of a stronger U.S. dollar (NYSEARCA:UUP) and a weaker euro (NYSEARCA:FXE), particularly as European policymakers unleash additional liquidity into the financial system. From an equity perspective, it should cause U.S. investors to bias more toward domestically-oriented firms in their stock (NYSEARCA:SPY) portfolios. It should also lead to gradually increasing risk aversion on the fixed-income side away from segments such as high yield (NYSEARCA:HYG) and senior loans (NYSEARCA:BKLN), and an inclination toward higher-quality safe-haven credits such as U.S. Treasuries (NYSEARCA:TLT). Precious metals such as gold (NYSEARCA:GLD) may also finally start to have their day under such a scenario, but liquidation pressures may weigh on the metal in the near term. Moreover, other factors must be considered before considering a long-term allocation to gold, including the direction of the dollar and other factors that have been recently unique to the precious metals market.

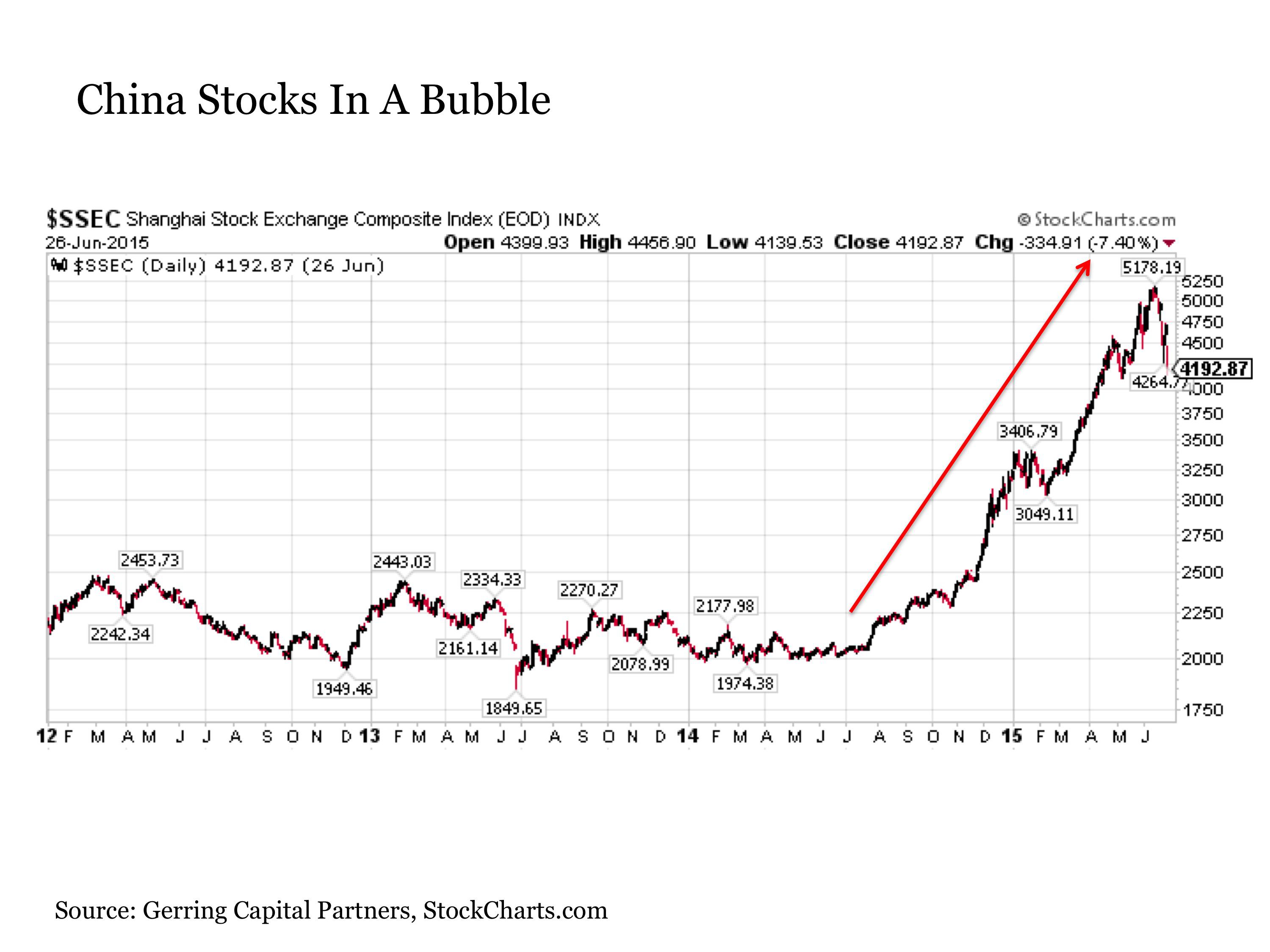

The China Bubble

While the word "bubble" gets thrown around way too much in the financial media nowadays, the Chinese stock market (NYSEARCA:GXC) is currently in what can truly be described as a bubble. A look at a chart of the Shanghai Stock Exchange Composite shows why.

(click to enlarge)

China was a stock market that was adrift in a sideways pattern for several years. But suddenly last summer, it began erupting to the upside. And over the past year, it increased by over +150% in value, before recently falling back by more than -20% in recent days. China stocks have made this remarkable advance not because their economy has been performing so well, but instead, it has taken place despite the fact that the country's economy continues to slow. For in a story that is all too familiar to first United States then Japanese and now European investors, Chinese policymakers - including the People's Bank of China - have created financial market conditions that have been conducive to artificially inflating asset prices, including stocks, beyond all reasonable recognition.

The only difference here is that China has done so far more aggressively over the last year, and unlike beleaguered investors across much of the rest of the globe who are still licking their wounds from other major bear markets that have taken place in recent years, many Chinese investors are relatively new to the stock market game. As a result, the rise in Chinese stocks has been accompanied by many of the classic signs of bubble behavior, including inexperienced retail investors borrowing money they do not have to get leveraged to the hilt in stocks and corporations shutting down more productive activities so that they can divert capital into the stock market. Such bubble-like conditions never end well, and China, more than the rest of the world, is currently caught up in such a mania.

Thus, the fate of the Chinese stock market also warrants close attention as we progress through the second half of 2015. Indeed, the opening of the mainland China market to foreign investors may ultimately justify the recent rise in Chinese stock prices, but given that the market has come so far so quickly in so many unhealthy ways, some extended periods of extreme volatility and pain should now be expected going forward.

As for the references that Chinese stocks have now entered a bear market, this may be technically true, given that the market is now down -20% from its recent highs. However, what makes a bear market a true bear market is not only the magnitude of the decline, but also the duration. If a stock market drops by -20% over the course of a few weeks and quickly recovers this decline, this is not really a true bear market, because investors did not feel any prolonged pain (for example, if it's something that you could have missed while on vacation, it's not a bear market). But if it's something that drags on seemingly relentlessly over time, then that is a bear market in the truest sense.

But what are the implications of a Chinese stock market bubble bursting for investors in other parts of the world, including the United States? First, global investment markets are now highly interconnected. Thus, a major liquidation of assets in one part of the world will almost certainly have spillover effects on the rest of the globe that have the potential to play out over time and in potentially unpredictable ways.

To highlight this point, it is worthwhile to reflect on the so-called "taper tantrum" of May and June 2013. While the market sell-off at the time was largely attributed to the U.S. Federal Reserve beginning the conversation about scaling back on QE3 asset purchases, another more destabilizing and destructive force was playing out underneath the market surface at the same time that few in the media chose to recollect or even remember today. For at the same time that then Fed Chairman Ben Bernanke was taking to the podium to talk about scaling back asset purchases in May and June 2013, Chinese policymakers, including the People's Bank of China, were cracking down on activities in their shadow banking system. This caused liquidity across the Chinese financial system to dry up, as reflected by a dramatic spike in the seven-day Shanghai intrabank offered rate (SHIBOR) to over 12% (by comparison, it is currently below 3% today). In short, financial institutions across China did not have access to necessary daily liquidity at the time (remember the post-Lehman Brothers period in the U.S.) and were forced to fire-sell assets to raise cash to fund operations (once again, remember the post-Lehman Brothers period in the U.S.). What were these Chinese financial institutions selling at the time?

Among other things, the holdings that were most liquid, which included U.S. stocks, U.S. Treasuries and gold. Thus, if a bursting of the Chinese stock bubble causes liquidity conditions to seize, do not be surprised if assets across the board in the United States find themselves coming under pressure.

The investment implications of what is taking place in China are the following. First, any direct investments in China (NYSEARCA:FXI) or closely related markets such as Hong Kong (NYSEARCA:EWH) may best be avoided, or at a minimum, should be undertaken with great care by those with the experience to navigate these markets. As regards those not directly exposed to China, they can ill afford to ignore how events are unfolding. For if market conditions begin to accelerate more sustainably to the downside, liquidation pressures are likely to eventually find their way to U.S. shores across all asset classes, including stocks, bonds and precious metals. Liquidation episodes are often followed by attractive buying opportunities, but they can bring second and third derivative spillover effects that must also be evaluated. Lastly, if a market correction in China starts to measurably erode business activity in the country, this has the potential to have adverse effects on the many companies in the United States that rely on China as a low-cost supplier of inputs for production.

In short, keep a close eye on China, and be ready to adjust portfolio allocations as necessary if conditions look like they are starting to unravel in a more meaningful way.

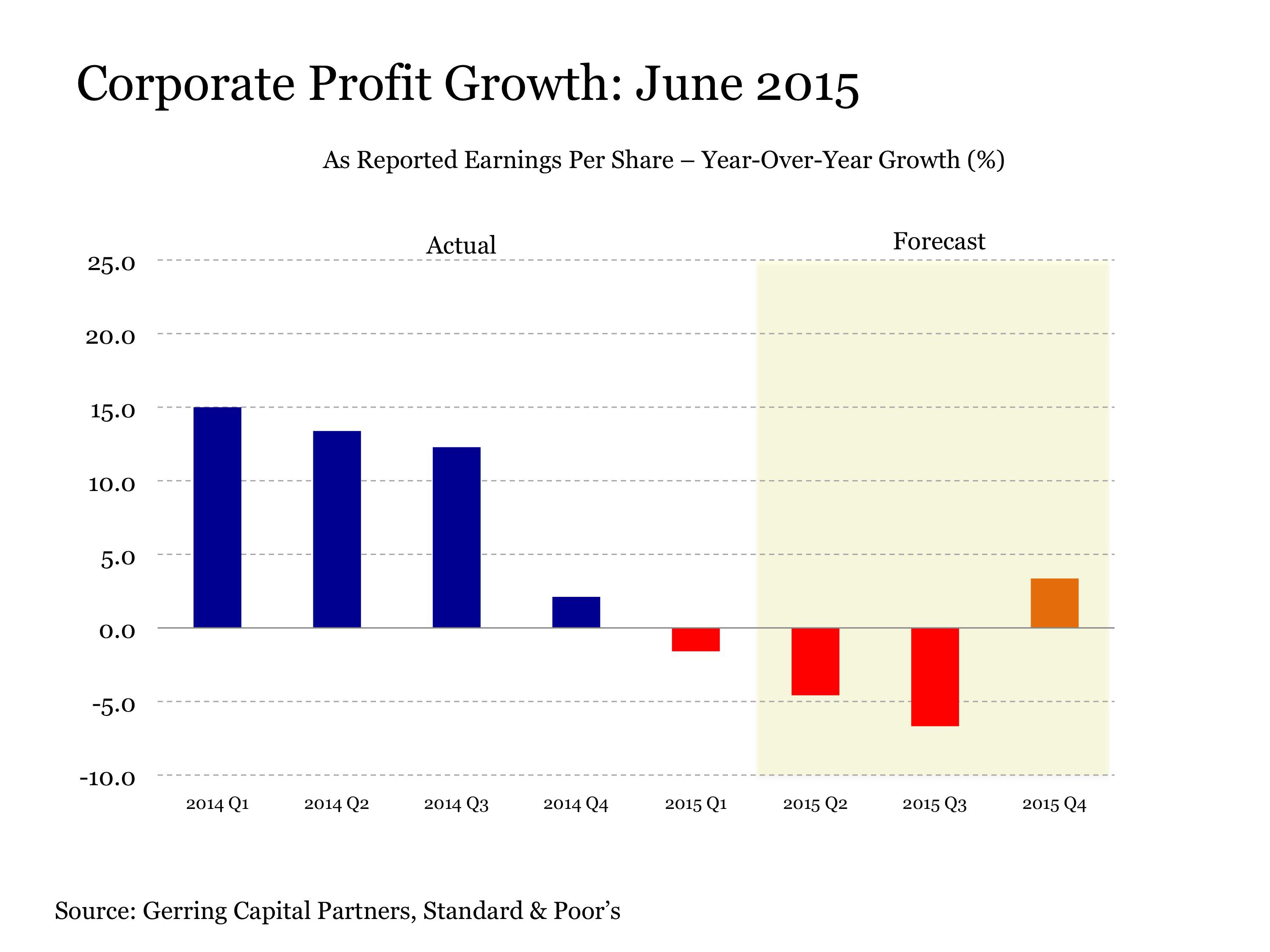

Deteriorating Corporate Earnings

The growth of corporate earnings is the lifeblood for stocks in a fundamentally driven market environment. And throughout the post-crisis period, a key tailwind for stocks has been the fact that corporate earnings have been steadily rising both on a quarter-over-quarter and year-over-year basis since the 2009 lows. But as we continue into the second half of 2015, investors will increasingly be seeing a market where the growth in corporate earnings, in many cases, will instead be falling on both of these measures.

Such was not supposed to be the case heading into 2015. At the end of last year, corporate earnings were projected to rise each quarter at a healthy double-digit pace on a year-over-year basis between 15% and 25%. Knowing that stock prices are predictive mechanisms that derive their value in part from expectations about future earnings, this optimistic forecast would presumably help explain the positive returns for stocks in 2014.

(click to enlarge)

But what has actually taken place so far in the first half of 2015 has been anything but robust.

In fact, it has been fairly ugly. Corporate earnings growth was not double-digit positive on a year-over-year basis in the first quarter of 2015. In fact, it was not positive at all. Instead, earnings declined by more than -1%. And for the second-quarter earnings season that is soon to get underway, earnings are now projected to fall by nearly -5% on a year-over-year basis. Even if they come in "better than expected", as they always do, they will still be a far cry from the +20% earnings growth predicted only a few months ago. And earnings growth is only expected to get worse in the third quarter before they are somehow supposed to start improving in the fourth quarter (let's see where this number stands in a month or two, as it was close to 10% only a couple of months ago).

(click to enlarge)

Now some rightfully point out that a good portion of the drag on corporate earnings is being sourced from the energy sector (NYSEARCA:XLE) that was badly bruised by the roughly 60% drop in oil prices since last July. But this overlooks the fact that the economically sensitive industrial sector (NYSEARCA:XLI) is also seeing earnings slip by double-digits on a year-over-year basis, undoubtedly in part due to the challenges from the energy sector. Earnings in the materials sector (NYSEARCA:XLB) are also flattening, while consumer staples (NYSEARCA:XLP) have been edging lower for several quarters. And the temporary boost to the overall earnings number from the telecom services sector (NYSEARCA:IYZ) that occurred from 2013 Q4 to 2014 Q3 is also now fading away.

So putting this all together, what we have here is a market that moved solidly higher in 2013 and 2014, based in part on strong earnings growth expectations that never fully materialized in 2015. Yes, certain sectors are still holding up well, but not so for the market in aggregate. Under normal market conditions, such would be the conditions for a measurable correction, particularly given that stock valuations are currently at the high end of historical ranges, both on an as-reported trailing 12-month and a 10-year cyclically adjusted price-to-earnings ratio basis.

Thus, the investment implications in a normal market environment would be to look to lighten up on stock allocations. But stocks can defy rational expectations in an environment of perpetually easy monetary policy, where interest rates are locked effectively at 0% by central banks such as the U.S. Federal Reserve. This leads us to our next critically important issue for investors to consider in the second half of 2015.

A Fed Determined To Raise Interest Rates

Since the outbreak of the financial crisis in 2007, the U.S. Federal Reserve has known only one policy stance. It was first to cut interest rates. But once interest rates had been lowered effectively to 0%, the next step was to engage in large-scale asset purchases as part of its quantitative easing programs (QE) to provide even more stimulus to the economy and financial markets. But after so many years of zero interest rate policy (ZIRP), the Federal Reserve is determined to raise interest rates, if at all possible, before the year is out. This represents a major shift not only from a policy perspective, but also as it relates to the financial markets.

While it can be clearly argued that monetary policy has actually been getting tighter since not long after the Fed began tapering QE3 well over a year ago, the financial markets have not had to deal with monetary tightening that included a Fed funds rate that was higher than the zero bound for many years. Although it seems like a small move to raise interest rates from essentially 0% to 0.25% or 0.50%, it is a major shift from a statistical and modeling perspective.

Investors should be prepared for increased stock market volatility the closer we get to the next phase of the Fed tightening cycle. Long gone are the days when the Federal Reserve would show up with its daily liquidity injections into financial markets totaling billions of dollars in the form of U.S. Treasury purchases. This helps explain why the stock market is not that much higher today than it was back in November 2014, when the Fed finished its QE3 stimulus program. But at least money from the Fed was still effectively free from an interest rate cost standpoint. But this will also soon change, assuming the Fed is able to follow through with its planned interest rate increases in the coming months.

Investors should be prepared not only for greater stock market volatility, but also for more sustained movement to the downside. This is because interest rates are expected to rise, and because of the conditions under which the Fed is seeking to raise interest rates. For under normal conditions, the Fed would be raising rates because of the economy, with the intent of slowing it down. But today, the Fed is raising rates despite the economy and the fact that it remains sluggish so many years into the recovery. So why then is the Fed looking to raise interest rates? At least in part because they want the policy flexibility to be able to lower interest rates by the time the next recession rolls around. And given that they are seeking to do so with valuations at historical highs and corporate earnings already trending lower suggests that stocks could come under increasing downside pressure as we move through the second half of the year.

So exactly when should we expect the Fed to begin raising interest rates? September is the period most widely discussed by Fed members in recent dialog, but whether this comes to pass will be both data and market dependent. After all, these same policy members once talked about June as a possibility, and that did not come to pass. But if the Fed were to raise rates in September, the next logical step would be a potential second-quarter point rate hike in December. But a good deal of time exists between now and then.

The investment implications of higher interest rates from the U.S. Federal Reserve are the following. The third-longest stock bull market in history remains ongoing to-date, but it may soon start to come to an end in the coming months. As a result, investors should seek to be more selective and defensive in their equity allocations than they may have been in the past. The time may finally arrive in the second half of the year to selectively and carefully consider selected inverse strategies that are designed to perform well during periods when the stock market is falling. This could be as simple and conservative as an allocation to intermediate-term U.S. Treasuries (NYSEARCA:IEF), or many other options that are more assertive in this regard.

Holding an increased allocation to cash (NYSEARCA:BIL) is also a prudent approach in such an environment. For whenever one wishes to go shopping, it is always beneficial to wait for the items you wish to buy to go on sale to help get the most out of your dollar.

Bottom Line

It promises to be an exciting and eventful second half of 2015. Four critical market events have been explored here, and this list does not even include the unfolding debt crisis in Puerto Rico or the ongoing geopolitical threat that also loom as potential risks for the markets in the months ahead. And when considering the convergence of these various forces mentioned above, we could be entering a stretch in time for capital markets where virtually any major asset class could come under sustained pressure for a measurable period of time. But in aggregate, stocks are at the greatest risk of a sustained downside correction, given the various forces at work.

Right now, the uptrend in stocks remains intact, and it should be respected. But this could change at any time at this point. As a result, investors should be ready to act accordingly to protect their portfolio value if and when conditions warrant.

More than ever before, the coming months will not be a time for investor complacency. It will be important to maintain a close watch on capital markets and to have an action plan at the ready not only navigate the downside risks, but also to capitalize when the time is right for meaningful upside opportunities will also present themselves along the way and will be there for the taking for those that are prepared and at the ready.

0 comments:

Publicar un comentario