Andrew Smithers

Jun 10 05:32

World growth over the past three years has fallen below its five-year rate and below its very long-term one, as chart one shows. It seems therefore reasonable to assume that we are experiencing what is at least a cyclical downturn. But the chart also shows that the trend since 1980 or 1990 seems to be a rising rather than a falling one. It doesn’t therefore seem to me reasonable to assume that the world is about to experience of the sort of longer -term slowdown that can reasonably be described as secular stagnation, though of course this may happen.

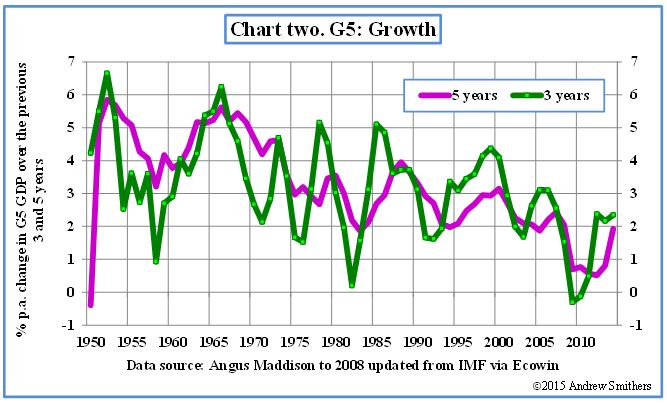

It is, however, sadly likely that the developed world is experiencing a secular decline in its growth as shown in chart two. The falling trend is common to all G5 countries and is driven by both demography and poor productivity.

Additional evidence is provided by the fall in unemployment that has made a major contribution to the mild recovery that has been achieved over the past five years and which appears to be unsustainable in that unemployment in Japan, the UK and the US has fallen to levels from which further declines are unlikely.

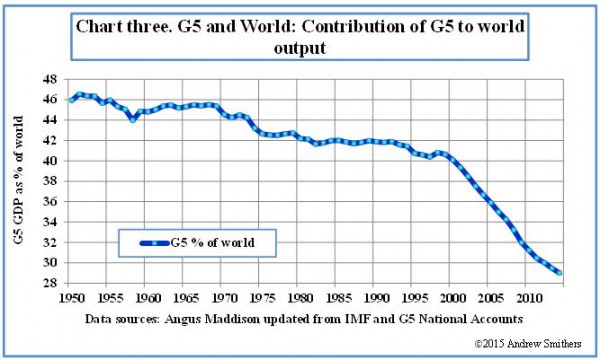

The contribution to world output from G5 countries has shrunk and has done so very sharply this century, as I show in chart three. A long-term slowdown in the developed world will thus have increasingly less impact on world growth. Even though it seems quite likely that growth will slow in the emerging economies, this will not necessarily slow the rate at which the world’s economy expands, because emerging economies are still growing rapidly and are becoming an ever more important constituent of the total increase in world output.

Interest rates seem likely to rise for cyclical reasons in the US, but it is widely expected that the rise will be mild and that real interest rates will remain low by historic standards, with secular stagnation being the fashionable explanation. This is, I think, a very dubious argument. While there is wide support for the idea that real interest rates are driven by growth rates, this theory only applies worldwide.

When economic theory is applied to forecasting interest rates in individual countries, the expectation is that slow-growing ones will have real interest rates that are above rather than below the world average. This is due to the Balassa-Samuelson effect, which holds that countries that have below-average productivity will have rising real exchange rates. Expected real short-term interest rates must be the same when measured in a common currency. So when measured in their domestic currencies, the real interest rates in slow-growing economies must be higher than those in rapidly growing ones to offset the profit that investors would otherwise obtain from owning the currencies of rapidly growing economies.

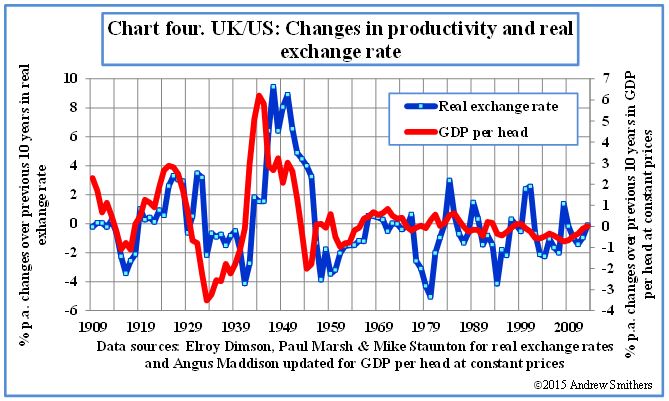

In chart four, I compare the changes in sterling/US dollar real exchange rate with those of the two countries’ relative productivities, with both series measured over the previous 10 years. (I measure productivity by GDP per head on the assumption that there has been little relative change in the ratio of employment to population.) The fluctuations in the two series move quite well together and thus provide evidence that the Balassa-Samuelson effect works in practice as well as in theory.

Even if we accept the theory that interest rates and growth are linked, the US will only have sustained low real interest rates if this is a worldwide phenomenon. If the US growth is poor but that of the rest of world is not, then real interest rates worldwide should not be depressed and those in the US should be above average.

The expectation that low growth in the US will keep down US short-term real interest rates does not therefore appear to have sound theoretical basis. Indeed, it would be more reasonable to assume that US productivity will be below world levels and thus have relatively high real interest rates.

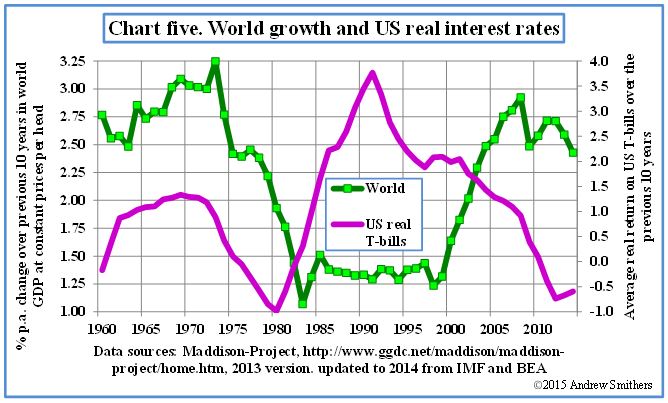

In practice, however, experience suggests that growth either in US or world terms will have little if any impact on US real interest rates. As I illustrate in chart five, there has been no apparent relationship between US real T-bills returns and the growth of world GDP per head, nor in terms of the growth of the world measured in total GDP.

In practice it seems probable that US real interest rates will be determined by the Fed’s attempts to contain inflation. The weaker the monetary policy, the greater the risk that inflation, and expectations for it, will increase and the more real interest rates will then have to rise. A prolonged period of sustained low interest rates is thus more likely if the Fed increases interest rates son.

0 comments:

Publicar un comentario