Jun. 1, 2015 12:15 PM ET

Summary

- There is not enough registered gold to fulfill this month's COMEX delivery obligations.

- About 375,000 registered ounces face 550,000 worth of delivery claims.

- Few, if any, COMEX clearing members are likely to default, but increasing tightness in the physical gold market makes physical gold and gold mining companies excellent long term investments.

The buyer must deposit the full cash value of the entire gold contract, or 100 ounces of gold, into his brokerage account. At the current price, that means depositing approximately $120,000 in your account for each contract you own.

In practice, most COMEX long investors are hedge fund managers who can and do pile up to 32 to 1 leverage in the hope of getting rich quick. They are usually gambling with other's people's money. A heavily leveraged COMEX trader, therefore, can control 100 troy ounces of gold in exchange for a mere $3,750 of US dollar cash. Nowadays, about 2% of the maximum number long buyers actually stay on long enough to take physical delivery. The number of ounces delivered every two months hasn't changed a great deal.

To keep COMEX the single most important gold price setting mechanism in the world, the exchange maintains a fiction that all its futures contracts are potentially "deliverable". That, of course, is nothing but smoke and mirrors. The fiction is maintained by the fact that buyers are mostly gamblers, who don't have the money to buy the gold. Similarly, sellers don't have the actual gold to sell. If a large group of real buyers ever tried to force deliveries from COMEX, the exchange would be forced into cash settlement.

To maintain the fiction of deliverability, various warehouses are licensed to store so-called "good delivery" gold bars. These bars are often referred to as COMEX "inventory". "Good delivery" means that the bars were manufactured by a recognized refiner, are assayed to 99.5% pure gold, and are either 100 ounces or 1 kilo each. A full contract delivery can be made by delivering either a 100 ounce bar of gold or three bars weighing one kilo each.

Good delivery gold is divided into two categories, "eligible" and "registered". Most gold bars in the warehouses are "eligible" because they have all the necessary prerequisites to meet the "good delivery" standard, but are not registered. Their owners don't want to sell them and that is why they are not registered. "Registered" gold are bars that have been earmarked for use by the exchange clearing members to meet delivery requirements.

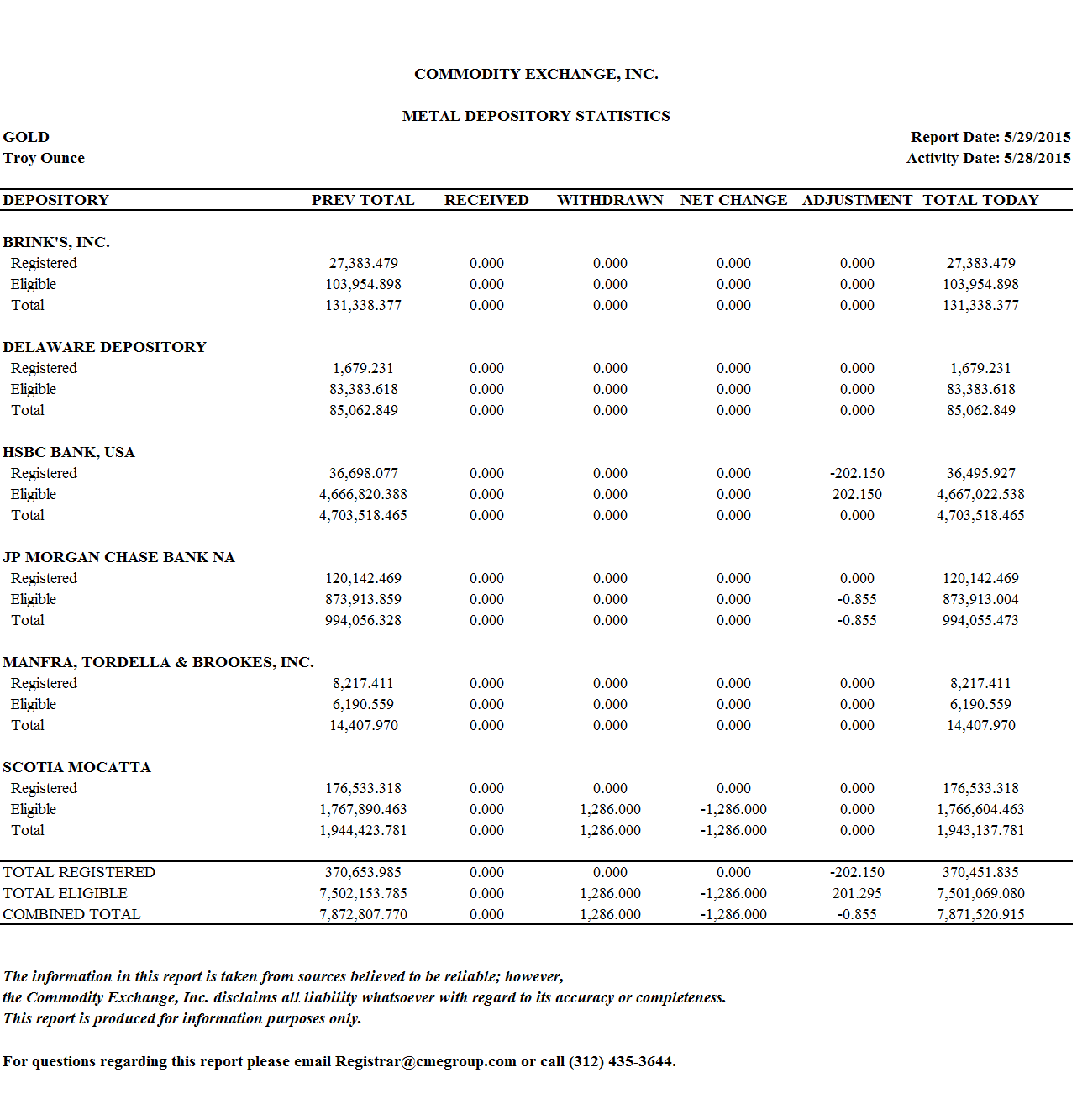

The following spreadsheet illustrates the current stockpile situation at the COMEX licensed warehouses, as of May 29, 2015.

(click to enlarge)

COMEX gold futures contract mature on the last day prior to the 1st business day of their designation month. Thus, the June gold futures matured on May 29th, 2015 because it was the last working day of May. About 5,500 long contracts remain outstanding, out of an original total that reached its top at more than two hundred thousand.

To "stand" for delivery, the buyers of those contracts needed to fill their brokerage accounts with enough cash to pay for the entire cost of the gold. About 550,000 troy ounces of gold must be delivered for the June contract. This is not an unusually large amount of gold. About 5,400 contracts stood for delivery on March 31st, the maturity date of the April futures contract. What is different is that COMEX warehouses are only storing 370,452 troy ounces of registered gold. For the first time I can remember, COMEX has a net shortfall of about 170,000 ounces or 5.29 tons. That is a lot of gold.

While it is possible that a situation like this has happened before, I cannot remember it. There simply isn't enough registered gold at COMEX to meet the delivery demand. That does not necessarily mean there will be a major default. COMEX clearing members can and do get gold in many other ways, outside the exchange. Even in normal months, sources outside the exchange are used to meet delivery requirements. A high degree of leverage facilitates moving paper prices up and down without much risk. Some believe that an intentional effort is made, in the early days of every delivery month, to artificially reduce world gold prices so that the dealers can buy deliverable gold on the cheap.

Mining companies and most others generally accept COMEX-derived prices as the "official" world gold price, even though the price reflects mostly gambling, rather than supply and demand. Even when supplies of real gold are tight, miners and refiners almost always sell production at something very close to the COMEX price. Paper market imaginary gold, therefore, is able to change the price of real gold.

In this situation, however, no one can guess exactly what happens next. However, it seems to me that COMEX clearing members will manage to scrape up enough gold to make this month's delivery.

That's because a widespread default by a large number of COMEX clearing members would cause the exchange to lose its status as the world's most important price setting forum. A big default would also send gold prices suddenly soaring, putting hundreds of billions of dollars worth of off-exchange derivatives at risk of imploding.

The first place clearing members will go to source new gold bars is the London commercial market, otherwise known as the LBMA. This was formerly the biggest physical gold market organization in the world, and may still be. But, London based traders warn that it has become increasingly illiquid. Volume and trading of real gold has moved east to the Shanghai Gold Exchange in China. Chinese law forbids the export of gold bars, so there can be no help from there.

A best bet may end up being the US Treasury and/or the Bank of England. If conspiracy theorists, like those at GATA, are correct (and I think they are), the worst case scenario would be a stealth government bailout. It is relatively easy to set up "location swaps", where gold bars owned by the government are promised in exchange for gold bars in the eligible bar category at COMEX warehouses. People could be persuaded to put their physical gold into play, in the registered category, if a government guaranty on return of the actual gold, along with a thick "envelope" of Benjamin Franklins, is thrown in as a sweetener.

A government bailout would put US gold reserves at risk. However, the possibility that the gold will never be repaid hasn't stopped the government in the past. In 2009, writing on behalf of the FOMC, Fed governor, Kevin Warsh, admitted that the Federal Reserve's gold is subject to swap liens. J. Virgil Mattingly, the Fed's highest ranking lawyer during the 1990s, had admitted it in recorded minutes of an FOMC meeting, all the way back in January 1995.

However, by 2001, he was busy denying it, claiming he had never said that. Confirmation by Kevin Warsh, therefore, was very important. Knowledge that US gold has already been made subject to swap liens helps us understand what happens, behind the scenes, in the gold market.

The Fed directly controls only the gold in its basement vault underneath NY Fed at 33 Liberty Street. Ninety five percent of that, however, is owned by foreign nations. Hopefully, swap liens haven't been placed against that gold without consent of the nations involved. But, although the US gold reserve is still managed by the Treasury, all American gold was legally transferred to the Federal Reserve years ago, in the form of "gold certificates". The swapped gold, therefore, must be a part of the US gold reserve. It may not have been physically removed yet, from Fort Knox, but gold there and/or at other official repositories is encumbered by the claims of third parties.

In fact, by 2007 so many bars of gold had apparently been "swapped" that the US Treasury changed its description of the US gold reserve, for accounting purposes. The entry was altered.

The asset was once described as simply "gold bullion". But, then, it was changed to "gold bullion, including gold deposits and, if appropriate, gold swapped". Thus, it is abundantly clear that the US gold reserve is already encumbered. In light of that fact, why not swap out a few more bars? If it means saving COMEX, it seems a given that the government will bail out the short-selling clearing brokers, if necessary.

On the other hand, a COMEX bailout may no longer be in America's best interest. It also might not be in the best interest of the big banks. Most of them are also big clearing brokers at COMEX. But, the hot money hedge funds are the ones who have been doing most of the short-selling lately. Many of these use smaller clearing brokers, rather than entities like Goldman Sachs and JP Morgan. The big banks may be net long COMEX gold by now. Yet, a sudden big rise in gold prices could weigh on hidden OTC derivative obligations we can know nothing about. Thus, a COMEX default might or might not be in the interest of the big banks.

If you are a believer in Keynesian economics, a large scale COMEX gold default might seem like good medicine for the US economy. Given the ongoing fear that the Euro will collapse, the US dollar has been soaring lately, in spite of a very weak US economy. Downward dollar pressure from a big COMEX gold default could be a welcome event. The dollar would take a downward hit, helping US products become cheaper in world markets. The resulting inflation may be exactly what the statists say we need. A COMEX default might provide a more powerful way to inflate the nation out of its unsustainable debt load, than QE money printing.

At any rate, regardless of this month's unusual gold deficiency, I do not believe that there will be a big default at COMEX. If you are an institution, a government or anyone else seeking a large quantity of physical gold, buying at COMEX is probably still a safe bet. You could buy COMEX June futures and take delivery this month. The worst that could probably happen is you get your cash back before the end of the month, in addition to a premium. More likely, however, you'll get your promised gold bars. The dealers may find enough gold on their own to complete deliveries. If not, they will probably get a government bailout.

The main point you should take back with you, however, is that real world gold supplies are increasingly tight. This is in spite of what appears to be lackluster paper prices at COMEX and other paper-based markets. The situation at COMEX shows that those who own real physical gold are not inclined to part with it. That's why there is so little gold in the COMEX registered category. The liquidity problem in London has spread to New York.

A situation like this cannot go on forever. The paper price of gold must be allowed to rise significantly. If not, there will be more and bigger supply problems in New York and London.

The current market tightness would get much worse. That means that the price of physical gold must eventually break strongly upward. The yellow stuff itself, and the companies that produce it are now very good long-term investment opportunities.

0 comments:

Publicar un comentario