Jun. 1, 2015 7:00 AM ET

Summary

- A test of the highs failed.

- Now we drift to the lows.

- Why the lows will fail too.

- What will move gold at this point?

- Divergences are the best clue - is that enough?

While gold is always in fashion, its value moves with sentiment.

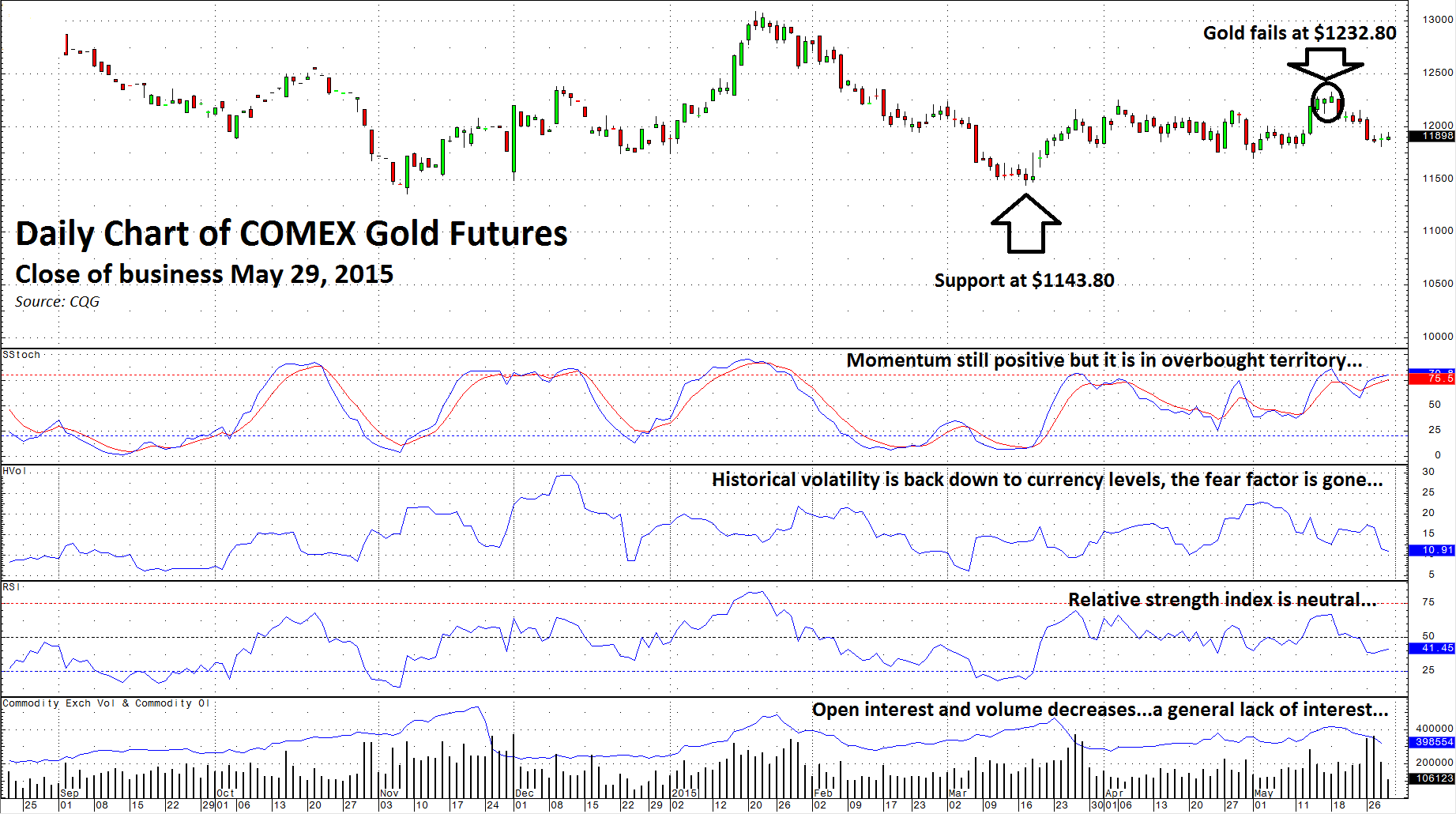

As with many assets, fear and greed often dictates price. Gold had a fantastic rally beginning in 2001, which took the price of the yellow metal from $255 all the way up to $1920.70 per ounce a decade later in 2011. Since then the price of gold have been grinding lower, settling on Friday, May 29 at $1189.80 on the active month COMEX August futures contract. Gold has been in a trading range since March, a recent rally breached upside resistance and vaulted it up to $1232.80 but gold failed to hold that level and moved lower.

A test of the highs failed

The recent failure of gold was significant. In many ways, it frustrated potential buyers and emboldened sellers.

(click to enlarge)

As the daily chart of COMEX August gold futures highlights, support for gold now is at the March 17, 2015 lows of $1143.80 per ounce. While the slow stochastic, a momentum indicator remains positive, it is in overbought territory. Historical volatility in gold has dropped as the market has been trading in a tight range. With volatility down to the 10% level, gold is trading more like a currency than a commodity these days.

Therefore, gold is likely to take directional clues from another currency that has been dictating direction for many markets, the U.S. dollar. The dollar recently held lows and has moved higher, this is not a positive development for the price of the yellow metal. While the relative strength index in gold is neutral, open interest and volume in gold has dropped since it could not sustain the $1230 level. Open interest, the total number of long and short positions on COMEX gold futures, has moved from 430,674 on May 18 to 398,554 contracts on May 29 -- a decrease of 7.5% while the yellow metal itself only declined by 3.5% over the same period.

The decrease in volume and open interest as gold prices dropped is not inherently bearish on a technical basis however; it does indicate that interest in the gold market is waning. The drop in historical volatility tells me that the fear factor in gold is gone today and that could mean gold is heading to test support.

Now we drift to the lows

We tried the highs in gold on May 18; the failure could mean that the yellow metal now needs to test the low end of the range at just over the $1140 level. With the close at the end of May, gold is now stands in the middle of the trading range. Unless the fear factor returns to the yellow metal, a test of the low end of the range seems inevitable. However, given recent trading action in the yellow metal do not expect too much from gold on the downside.

Why the lows will fail too

The highs in gold failed, and chances are so will the lows. You can be sure that as gold approaches the $1140 level, the bears will come out of the woodwork with a myriad of reasons why gold is nothing more than a barbarous relic of years gone by. They will be calling for prices to plunge to $1000 or below. The bulls will retreat, however if we have learned anything yet from trading action in markets in 2015 we know that it is a year for trading rather than for trends. That is why the high-odds play in gold is a failure to break down when support is tested.

Although the fear factor is out of gold along with participant interest for now after the recent upside failure, the world remains a dangerous and unstable place. An event could cause a flight to quality in a heartbeat given the current global landscape. Additionally, over the long-run cheap and artificially low interest rates around the world in order to stimulate economies has a price. The price will be inflation and whether it rears its ugly head in a few months or a few years gold, the ultimate store of value, will quickly adjust its price to an inflationary environment. In the short-term, issues around the world could ignite the price of gold in the blink of an eye.

What will move gold at this point?

So many issues could move the price of the yellow metal at this point. The never-ending saga of turmoil in the Middle East always provides the potential for a rally in gold. Intransigence and aggressive actions by the Russian leader, Mr. Putin, could bring the fear factor back to markets. In Asia, the aggressive posture of China with regard to sovereignty issues in the South China Sea and relations with Japan and the United States is a potential catalyst for gold. Not to mention the nuclear program of North Korea and their continued prodding of perceived enemies, South Korea, Japan and the U.S. could increase world tension and the price of gold.

At this time, as we move into the summer vacation season, it seems that only a real shock would bring investment demand back to the gold market. Investment demand and the perception of fear is a make or break factor for the yellow metal.

Divergences are the best clue - is that enough?

While gold remains in a trading range, divergences provide some clues as to the future price direction of the precious metal. Prices for industrial precious metals continue to be under pressure. At the end of May, both the platinum-gold spread and the silver-gold ratio continue to diverge from normal historical levels.

On a long-term basis, platinum should trade at a premium to the price of gold. Platinum is rarer, there is only around 250 tons of production each year. Annual gold output is around 2,800 tons. There are many more aboveground stockpiles of gold than platinum. The production cost for platinum is higher. Platinum production primarily emanates from two countries, South Africa and Russia while gold production is ubiquitous.

On an ounce-produced basis, there are far more industrial applications for platinum than for gold. On a multi-decade basis, platinum has traded at an average of a $200 premium to the price of gold. In 2008, that premium peaked at over $1200 while in the aftermath of the global financial meltdown platinum fell to a $200 discount to gold. At end of May, platinum stood at $78 below the price of gold. Given the fundamentals for platinum, the downside is limited and upside is explosive once the global economic landscape improves.

The silver-gold ratio closed May at the 71.2:1 level. This relationship has a long-term average level of 55:1. On a historical basis, gold has outperformed silver recently but over many decades, this price relationship tends to return to long-term historical levels. When it comes to both the platinum-gold spread and silver-gold ratio; both say that either the industrial precious metals are too cheap at current levels or gold is too expensive on a historical basis. Given recent action in the gold market, I continue to believe that gold is too expensive relative to these two other precious metals.

Gold looks awful after failing on the upside on May 18. Divergences between gold and other precious metal prices portend lower prices for the yellow metal based on historical norms.

However, 2015 has been a year for trading rather than for long-term trends in many markets.

While I believe that gold will eventually move lower, for the coming weeks it is likely to stay within the current trading range. When gold looked great two weeks ago, the right trade was to fade the rally and sell. It is likely that when the price inevitably trades down to support and looks really ugly it will hold.

For now, look at gold as a trading instrument rather than looking for a big trend to emerge.

Buying dips and selling rallies could be the only profitable trading strategy in gold until some exogenous shock moves the market out of the current trading range. Therefore, this year when gold looks awful, bite your lip and buy.

0 comments:

Publicar un comentario