Fed Rate Tale Needs a Growth Story

The Federal Reserve is on course to raise rates later this year without a good sense of how fast the economy can grow.

By Justin Lahart

June 14, 2015 12:46 p.m. ET

As it prepares to raise rates later this year, the Federal Reserve still lacks something crucial: A clear idea of how quickly the economy can grow.

There is now little doubt headwinds that hit the economy in the first quarter were mostly transitory. On the back of strong May jobs and retail sales reports, economists have lifted estimates for second-quarter gross domestic product growth. Coming data—expected to be strong—and a Commerce Department review of how it adjusts for seasonal quirks, suggest first-quarter GDP will be revised upward. None of this changes the outcome of the Fed meeting ending Wednesday: Rates will stay near zero. But a September increase is likely, and bond-market action shows investors are preparing for it.

Fed policy makers also will update their projections. While the main event will be where they think overnight rates should be at year-end, forecasts for how quickly the economy will grow in years to come bear watching. These have shifted substantially.

At the March meeting, policy makers’ longer-run GDP growth forecasts—their assessment of how rapidly the economy can grow annually without pushing inflation too high—were centered on 2% to 2.3%. That is half a percentage point lower than where they were four years ago. And it is far slower than 3%-plus growth in each decade from the 1940s to the 1990s.

The downgraded longer-run GDP forecasts may be backward-looking: Having been disappointed by growth of late, policy makers expect to be disappointed. But there are reasons to think the economy might not support as much growth as it did in the past.

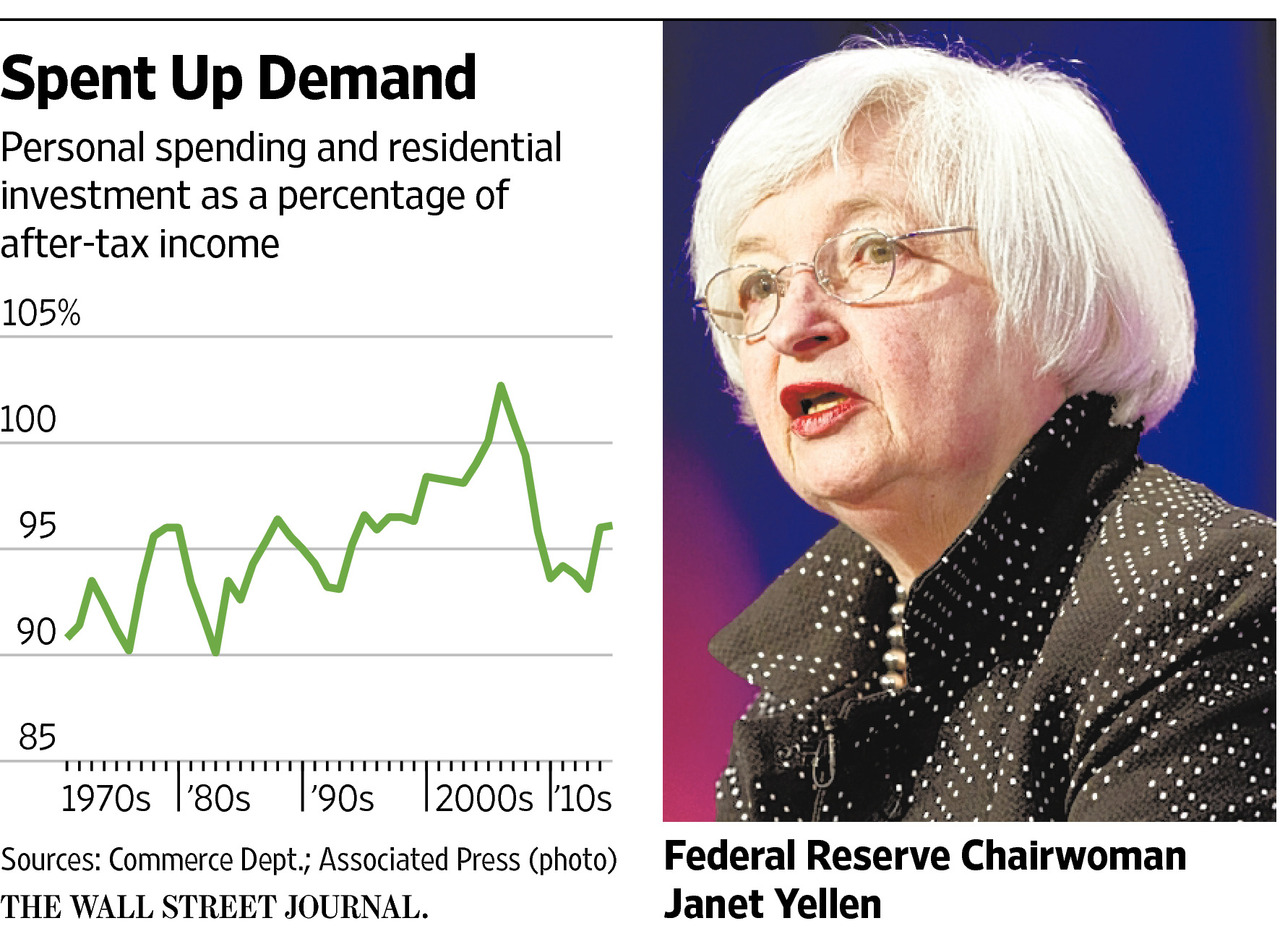

First, spending by U.S. households probably can’t drive growth as it once did. From 1980 to 2005, consumer spending and residential investment (mostly on new homes) went from 94% to 103% of after-tax income. That has since fallen to 96% and, as Legacy Private Trust Company economic adviser Paul Kasriel points out, seems unlikely to expand again. With households and

lenders more cautious, and regulators watching credit more vigilantly, consumer spending can probably only grow as rapidly as incomes.

Second, gains in productivity, as measured by how much the average U.S. worker can produce in an hour, have slowed—perhaps because companies have reined in capital spending. When productivity gains are low, the economy struggles to grow faster than its workforce grows.

And third, in an aging society, it will be difficult for the workforce to grow briskly. The United Nations projects the U.S. population aged 20 to 64 will grow by 0.2% annually over the next 10 years versus 0.8% over the past decade.

But while the slow-growth story could be true, that doesn’t mean it is. The real way to figure out the economy’s speed limit will be to test how fast it can grow without pushing inflation too high.

The Fed may start taking its foot off the accelerator in September, but it is a long way from slamming on the brakes.

0 comments:

Publicar un comentario