May. 17, 2015 11:27 PM ET

Summary

- The investment world is a place where sensible thinking can sometimes get completely turned upside down.

- This is absolutely true when it comes to holding cash.

- The conventional wisdom among most investors is that you must be fully invested at all times.

- This stubborn thinking defies rationale in many ways.

- Cash is king for a reason, and this holds true when it comes to investing in capital markets.

Expectations About Future Prices

The conventional thinking of why you should hold virtually no cash (NYSEARCA:BIL) and be fully invested at all times is based on a basic premise. People simply cannot justify keeping their money in a bank account earning less than 0.01%. Not only are they forgoing the long-term growth opportunities associated with investing in capital markets, such as stocks and bonds, but this money is also losing its purchasing power, since it is not even increasing in value enough to keep up with the rate of inflation. In this regard, the point makes sense.

But who said that just because you are holding cash today, you have made a commitment to keep it in cash permanently into the future? Perhaps instead, you are holding your money in cash to wait for a better deal to come along. For if the price of the item on which you intend to spend you cash deflates in value the near future, perhaps by going on sale or being liquidated, suddenly the purchasing power of your cash has been increased dramatically. All of the sudden, sitting on cash may not be such a bad idea.

The thinking behind using your hard-earned money, or cash, to purchase a stock should be no different than it is when considering spending on just about anything. Let's break this point down to its basics. Suppose you decide that you wanted to go out and buy a television set. Do you simply run out to the store immediately and buy one? The rational consumer likely would not. Instead, they would comb the weekly ads from the likes of Best Buy and H.H. Gregg, as well as cross-reference prices on Amazon.com, all in the effort to get the best deal. And if there is a particular television that the consumer decides that they want, they will often wait to make the purchase and hold on to their cash until such time in the future that the television goes on sale. Then they go out and buy the TV.

Now some might immediately make the argument that a television is not an asset that is going to appreciate in value over time, unlike a stock. Fair enough. With this in mind, let's then assume that you decide that you want to go out and buy a house in which to set up your new television and pass your days into the future. Once again, do you simply call up a realtor and buy a house on the first day of home shopping? Most of us do not. Instead, we wait spending months and months, holding our money in cash and visiting properties until we find the right house at the right price. And hopefully, the house we purchase will not only provide us with a nice living arrangement, but also greater capital appreciation over time to reward us for the patience and diligence in waiting until we landed the best deal.

In short, if we believe that we can buy the item that we want for a lower price at some point in the future, we are going to forgo buying that item today and will keep our money in cash in the meantime as we wait. For by waiting until we have discovered that lower price in the future, our purchasing power has been enhanced in the end as a result.

If this principle is true for everything else, why then should it not hold true for the stock market?

Cash Is King

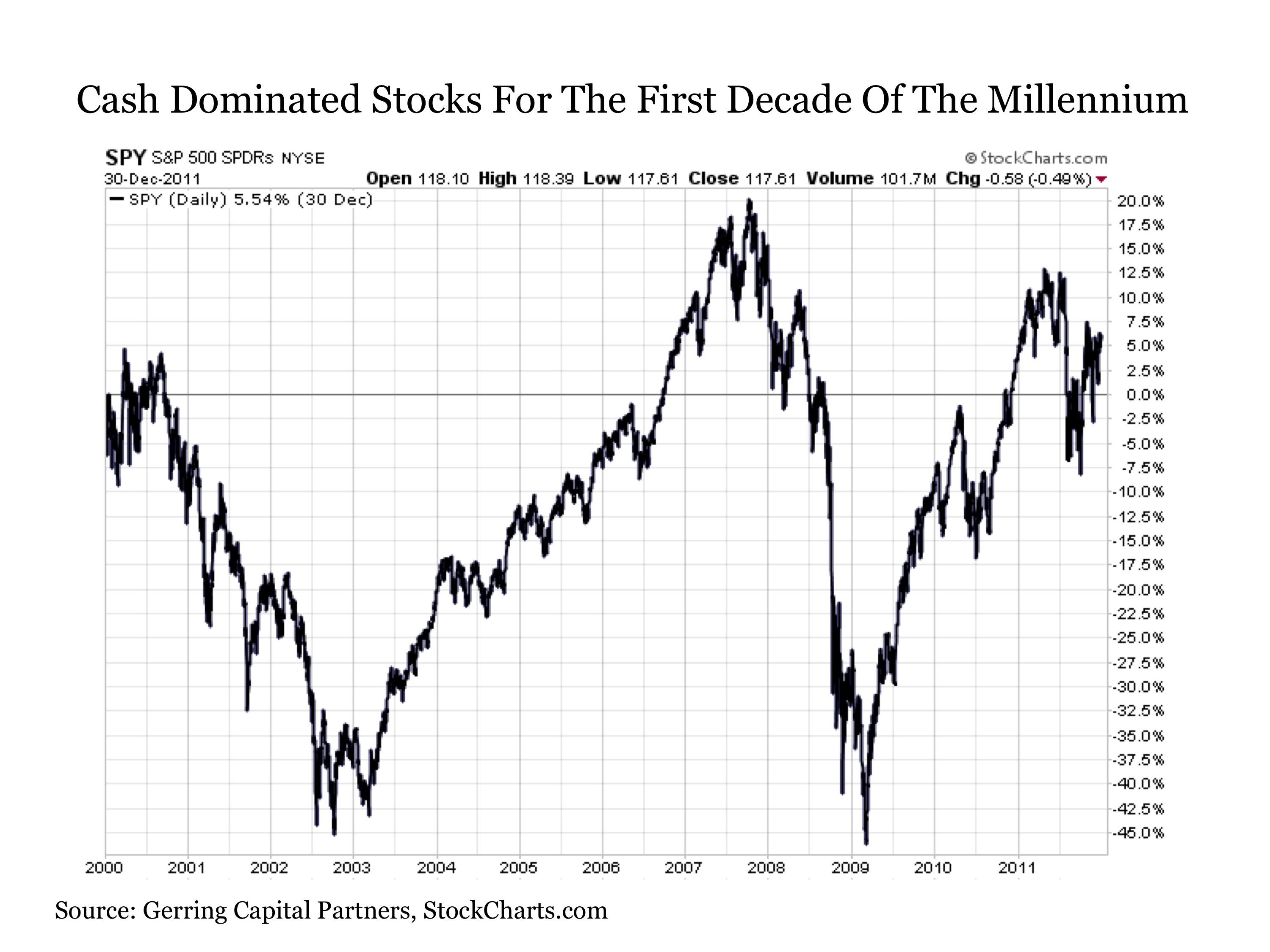

Let us now consider the stock market, in which, according to many, investors should supposedly be fully invested at all times. Suppose you had a big pile of cash at the exact start of the new millennium, and had two choices with which to allocate this money. You could either invest it entirely in the stock market as measured by the S&P 500 Index (NYSEARCA:SPY), or you could hold it in a checking account that earned no interest whatsoever. The following would have been your investment experience over the first decade of the new millennium.

(click to enlarge)

This choice would have left you with four possible outcomes. How could this leave you with four, you might ask? Because we do not live in a world where decisions made at any given moment in time are permanent. Instead, we have the ability to react and adapt along the way. With this in mind, the following are the four outcomes listed below.

- Go fully invested into stocks. Maybe you were already mostly invested, but decided to deploy the rest. Maybe you were all in cash. Regardless, you have decided to follow the mantra of being fully invested at all times. What is your subsequent experience? You see the value of your investment after dividends decrease by nearly half twice. And despite all of that stress, the nominal value of your investment twelve years later at the end of 2011 is essentially the same as it was at the start. The only problem is that the real value of your investment is still deeply underwater, as prices have cumulatively increased by more than 30% over this same time period. You have to wait another two years into 2013 before finally clearing that hurdle.

- Go fully invested into stocks initially. Investors can all talk a great game about how they will stick to their investment discipline and stay the course with their allocations, no matter what. This is easily said when the market is steadily rising and all of the news is good. But it is much more difficult when you have already seen nearly 50% of your portfolio value evaporate over the course of a couple of years, and much of the news in the mainstream business media suggests that more losses may be ahead. There is a reason why investors complain about buying high and selling low, and times like these are why, as investors remain fully invested, only to panic and exit positions after sustaining a meaningful loss, and to miss out on the subsequent upside.

- Stay in cash. Yes, the potential investor at the start of the new millennium may have decided that the stock market was not for them, simply kept the money in a checking account, and settled in Rip Van Winkle-style for a long nap. Awakening more than 11 years later, this same potential investor would have the opportunity to buy into the stock market at effectively the exact same price, and would have missed out on all of the excitement and agony that had taken place along the way.

- Stay in cash initially. Of course, the potential investor could have also decided at the start of the new millennium to stay in cash for now. Or maybe they decide to put some money to work in the market, but hold the rest back in cash to see how events unfold. Perhaps they think they may be able to get a better price a few years down the road, which, of course, they would end up having ample opportunity to buy in at much lower prices in about nine of the next twelve years.

Yeah, But...

The natural counterargument to this point is the following. Yeah, someone might say, one can see these opportunities in hindsight, but you've cherry-picked the starting point to make your argument. And to that I would say, this someone would be absolutely right. For I would presume that investors under this mindset would have less of a cash allocation after the market has dropped by 30-50% or more, because by then, they would have deployed their cash to purchase at least some of the stock items they wanted to buy as they went on a BOGO sale.

In fact, my reasoning for picking the start of the new millennium is that it was of only four times in history that stock valuations have been around as high as or higher than they are today. In short, stocks are expensive right now. And just as the sensible consumer does not run out and spend all of their money buying a television or a house when they are expensive, nor should they necessarily do so when stocks are expensive. Instead, the sensible consumer waits until the future, when these items go on sale before going out to buy. In the meantime, they hold cash while they wait.

What about those past four instances when stocks were roughly just as expensive, if not more so, than they are today? The most recent has been documented above, but what about the other three in 1901, 1929 and 1966?

In 1901, an investor could have waited until 1924 and still had the opportunity buy into the market at the same nominal price.

In the granddaddy of them all, an investor from 1929 could have waited more than a couple of decades until 1954 to buy into the market at the same nominal price.

In 1966, an investor could have returned more than twelve years later in 1978 and bought back into the market at the same price, even after including all of the dividends paid along the way. And this ignores the massive inflation that is taking place at the time as well.

In short, stocks are expensive right now. And when they have been this expensive in the past, the market has provided sale opportunities at some point in the future to buy at a better price.

Bottom Line

Maintaining a cash allocation in an investment portfolio can provide great value. For if it is your expectation that stock prices may be lower at some point in the future, the purchasing power of your cash will be increased once this sale finally arrives. And such a sale does not need to be across the entire market. It may simply occur for a specific sector or particular security. But by holding cash, you maintain the flexibility to seize the opportunity to purchase stocks on sale once the time comes.

Moreover, by holding cash, you are not forced to sell something else in your portfolio that you might otherwise be inclined to keep.

To this point, I am not suggesting that investors should sit fully on cash. Nor am I suggesting that they must hold a meaningful allocation to cash at all times. After all, it is when the market goes on sale that you want to put this cash to work. But by indicating that investors can derive great value by holding a meaningful allocation to cash for at least some of the time, it debunks the notion that investors must remain fully invested all of the time. For just because cash may only paying you a 0.01% interest on your savings today does not mean that it will not provide you with far more meaningful value in terms of purchasing power down the road once the stocks you desire are suddenly on sale.

0 comments:

Publicar un comentario