Gold - More Of The Same

May 26, 2015 7:15 AM ET

Summary

- The rally failed.

- Divergences weigh on price.

- A bearish technical factor.

- Who cares?

- Interest rate increases will eventually push gold lower.

The rally failed

While the gold market looked great on Monday, Tuesday May 19 was an entirely different story.

Gold once again did what it has been doing since March, it looked like it was going to break out of the trading range but it did not and the rally failed. On Tuesday, gold fell by over $20 and now sits in the middle of the trading range as it settled on Friday, May 22 at $1204. Although it made a marginal new high at $1232 the failure last week to make new highs above that level or at the very least hold over the top end of the trading range does not bode well for the precious metal. One of the key reasons for the negative outlook continues to be divergences between the price of gold and other precious metals, which continue to weigh on its price.

Divergences weigh on Price

There is always more to the story when it comes to the nominal price of a commodity. A price of gold at the $1200 level is an indication of value however, that indication is only superficial.

When trying to determine whether gold is cheap or expensive at the $1200 level the analysis must be deeper. One of the tools that I find helpful in determining value for a commodity is the historical price relationship between the commodity in question and other commodities that are substitutes or similar in nature to the one being analyzed. When it comes to the price of gold, I like to look at the price or value relationship between the yellow metal and platinum (aka rich man's gold) and silver (aka poor man's gold).

The platinum-gold spread closed on Friday, May 22 at minus $55 -- gold is at a $55 premium to the price of platinum. Both metals are precious, however platinum is rarer than gold with only 250 tons produced each year compared to 2,800 tons for gold. Platinum has a higher production cost, the vast majority of annual production comes from South Africa and Russia and platinum has a myriad of industrial uses. On a per ounce produced basis, industrial applications for platinum far outweigh those for gold. Both metals thrive on investment demand however since 2011; both have been in bear markets making a series of lower highs and lower lows. For the reasons stated, platinum should always trade at a premium to the price of gold however today that is simply not the case.

(click to enlarge)

This weekly chart of the platinum-gold spread highlights the price action in the inter-commodity relationship. Platinum traded at over a $1200 premium to the price of gold in 2008, since then it has been a one-way street lower. In 2012, in the wake of the global financial crisis and during the period of quantitative easing in the United States, platinum went to all-time lows against gold trading down to a $200 discount to the yellow metal.

I believe that when platinum trades at a discount to gold, it is flashing a long-term signal that either platinum is too cheap or gold is too expensive on a relative basis. Over decades, platinum has traded at a premium to the yellow metal and today's discount is an important value consideration for gold when analyzing its price.

Moreover, gold's relationship with silver is an even more stark example today of the divergence between gold and other precious metal prices. The long-term norm (over the past four decades) for the silver-gold ratio is the 55:1 level. This means that there are 55 ounces of silver value contained in each ounce of gold value as a historical norm. As of Friday, May 22, the silver-gold ratio stood at 70.70:1. The higher the ratio goes the cheaper the price of silver is relative to the gold price.

(click to enlarge)

The monthly chart of the relationship between silver and gold prices highlights the current divergence. As with the platinum-gold spread, the silver-gold ratio is telling us that on a historical basis the price of silver is either too cheap or gold is too expensive at today's prices.

I interpret the divergences in these two inter-commodity spreads as bearish signals for the price of gold. After the recent failed attempt at a rally by gold, technical factors in the gold market validate the bearish view that divergence provides.

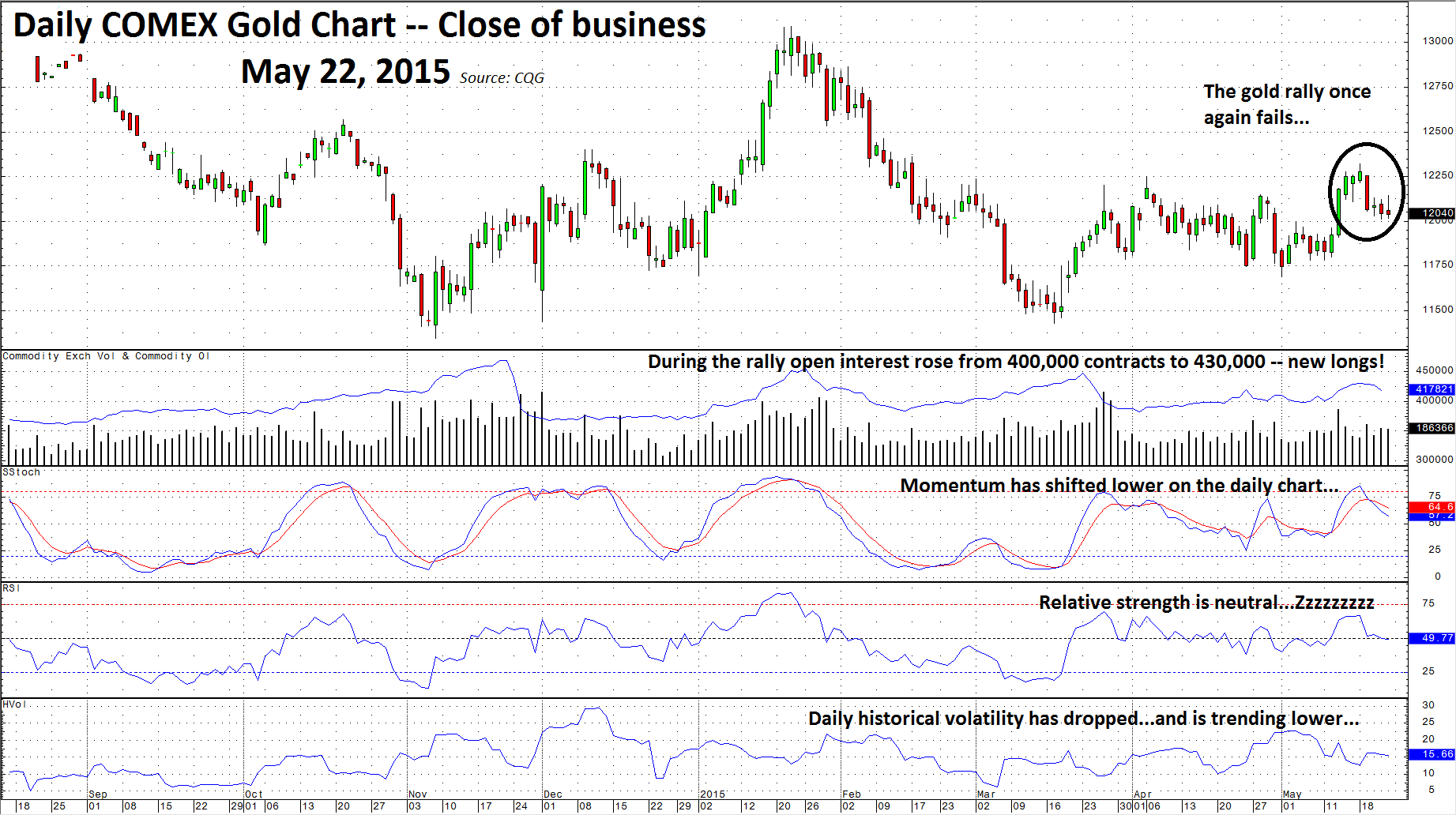

A bearish technical factor

The daily gold chart highlights gold's price failure last week. A number of technical factors could be signaling that lower prices are coming.

(click to enlarge)

As gold rallied from $1168 on May 1 all the way up to new short-term highs on May 18 at $1232, open interest expanded. Open interest is the total number of open long and short positions on the COMEX gold futures market. Open interest is an excellent tool to monitor interest and perception in terms of the price direction of a futures contract. Gold rallied a total of 5.48% during the first half of May and open interest moved from 400,000 to 430,000 contracts -- an increase of 7.5%. Increasing price coupled with increasing open interest is supposed to be a bullish sign for a futures contract. After gold failed on May 19, open interest dropped to 417,000 contracts. This tells me that new long positions were frustrated quickly and bailed out of the market.

Now that gold is back in the middle of the trading range it is quite possible that the rest of the new long positions will throw in the towel and gold will once again fall to the bottom end of the range. Validating that opinion, the slow stochastic, a momentum indicator, has crossed and now indicates a short-term downtrend for the yellow metal. Daily historical volatility in gold is dropping. At the 15.66 level, it appears to be on its way lower, which means less price action in gold for the time being. Finally, the relative strength index in gold is currently at 50 -- a very neutral reading.

Who cares?

There was some brief excitement in the gold market at the beginning of last week. The bulls watched with glee as the price broke out above recent highs and the bears relished in Tuesday's trading action as the bulls put their tails between their legs once again. Since March, gold has frustrated bulls and bears alike on numerous occasions. While devotees of trading gold (both bulls and bears) have anxiously awaited a break in once direction or the other, both have been frustrated with the trading action since March.

The bottom line is that those who bought dips and sold rallies have made some money -- agnostic trading has been the only strategy that has worked in the gold market. The reason, the rest of world does not seem to care much about the gold market these days. Gold is out of vogue with many market participants simply taking a who cares attitude toward the yellow metal. Meanwhile, a clue as to the next move in gold away from the $1200 pivot point may have come last Friday.

Interest rate increases will eventually push gold lower

In a speech in Providence, Rhode Island on Friday, May 22, Federal Reserve Chair Janet Yellen said that if the U.S. economy continues to improve "it will be appropriate at some point this year" to start raising interest rates. Higher rates will be a negative for the price of gold, as the cost of carrying the yellow metal will increase. Over past years, every dovish signal by the Federal Reserve in terms of U.S. interest rates has caused the price of gold to rally. There is no reason that higher interest rates will not have the reverse effect on the price of the precious metal.

Last week's failure of gold to break to the upside is just another chapter in a boring range trading saga for gold. For the gold market, it is just more of the same. When gold does finally break out of this range, it is likely to move lower, there are too many bearish signals flashing to ignore.

0 comments:

Publicar un comentario