Mar. 12, 2015 8:00 AM ET

By Sumit Roy

It's becoming increasingly likely that WTI will challenge the six-year low set in late January.

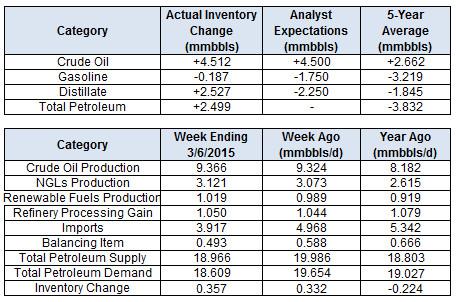

The Department of Energy reported this morning that in the week ending March 6, U.S. crude oil inventories increased by 4.5 million barrels, gasoline inventories decreased by 0.2 million barrels, distillate inventories increased by 2.5 million barrels and total petroleum inventories increased by 2.5 million barrels.

Crude oil was a mixed bag following the release of the latest inventory figures, with Brent rising and WTI falling. However, both benchmarks have declined during the past week, as bloated inventories and ever-rising U.S. production weigh on the market.

BRENT

WTI

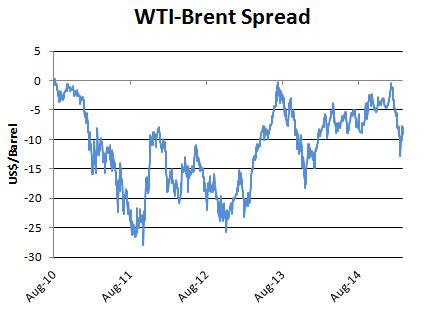

In our view, it's increasingly likely that WTI will retest its cycle just above $43 as U.S. inventories continue to mount. On the other hand, with Brent more than $11 above its cycle low of $45, the European benchmark looks safe for now. It could certainly decline from here, but it would take a very bearish development in the market to push prices for that benchmark to new lows.

Of course, if oil stockpiles continue to surge and storage capacity runs out, all bets may be off and prices could fall precipitously. That's what Ed Morse, head of commodity research at Citigroup, thinks will happen. In an interview with HardAssetsInvestor earlier this week, Morse told us that prices may fall as low as $20 to force shut-ins of production once inventories completely fill.

That's similar to an argument we made late last year. That said, it's very uncertain whether such a scenario will come to pass or whether the market will tighten quickly enough to prevent it. In the very short term, any bullish response will have to come from the demand side, because it's quite clear that supply is not responding yet.

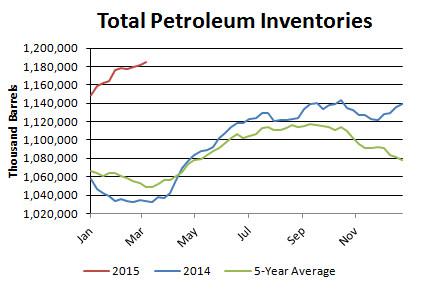

Turning to this week's EIA inventory figures, total petroleum inventories in the U.S. increased by 2.5 mmbbl, against the five-year average of a 3.8 mmbbl decrease. In turn, the inventory surplus increased to 135.3 mmbbl, or 12.9 percent, against the five-year average.

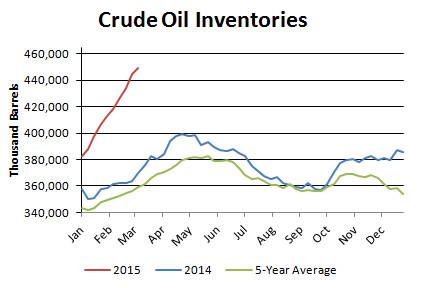

Crude oil inventories rose by 4.5 mmbbl, against the five-year average of a 2.7 mmbbl increase. In turn, the surplus in the crude category widened to 89.7 mmbbl, or 25 percent.

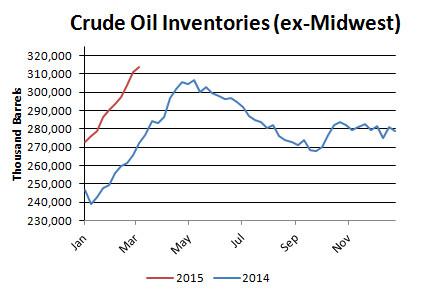

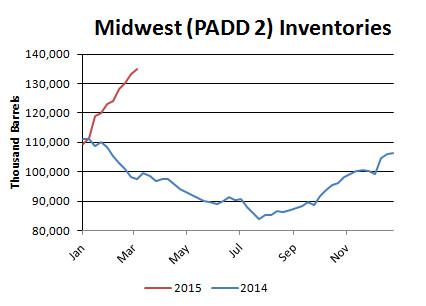

Regionally, inventories inside and outside the Midwest rose.

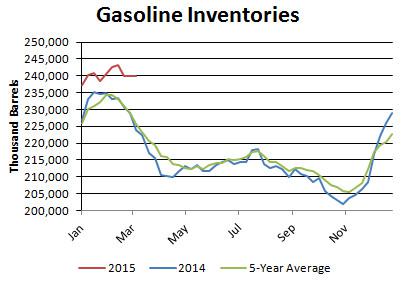

Gasoline inventories fell by 0.2 mmbbl against the five-year average of a 3.2 mmbbl decrease.

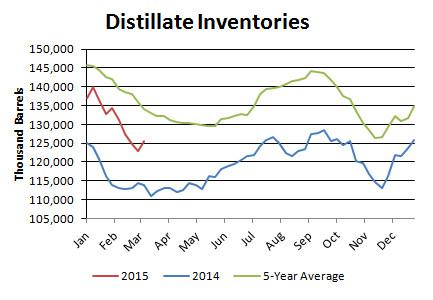

Gasoline inventories now have a surplus of 14.2 mmbbl, or 6.3 percent. Distillate inventories rose by 2.5 mmbbl against the five-year average of a 1.8 mmbbl decrease. In turn, the distillate deficit narrowed to 8.5 mmbbl, or 6.3 percent.

Demand

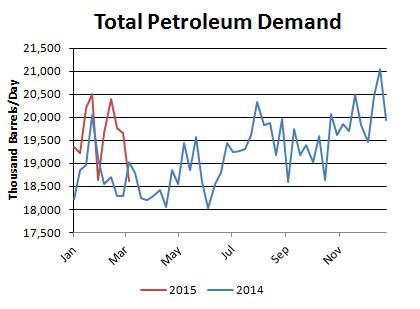

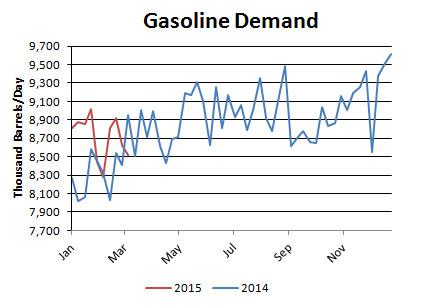

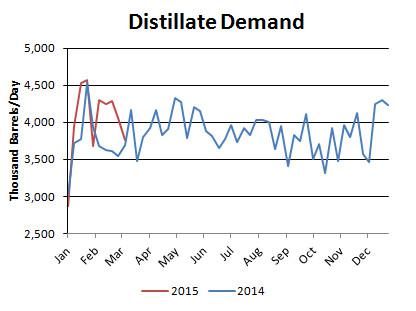

Total petroleum demand in the U.S. dropped to 18.6 mmbbl/d, while gasoline demand fell to 8.5 mmbbl/d and distillate demand fell to 3.8 mmbbl/d. On a four-week rolling basis, total demand was up by 5.5 percent from last year. On that same basis, gasoline demand was up 2.8 percent and distillate demand was up by 12.8 percent.

It's worth noting that these figures may be overstated due to the EIA's methodology for calculating demand.

Imports

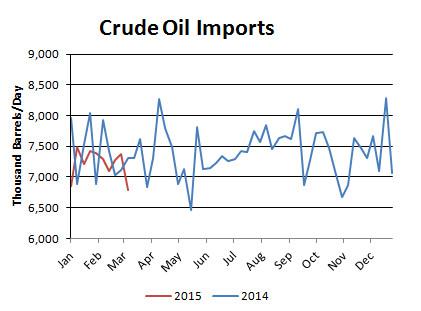

Crude oil imports fell by 0.6 million barrels per day to 6.8 mmbbl/d. On a four-week rolling basis, imports have averaged 1.2 percent below the year-ago level.

Refinery Activity

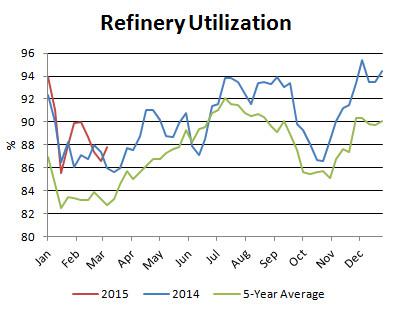

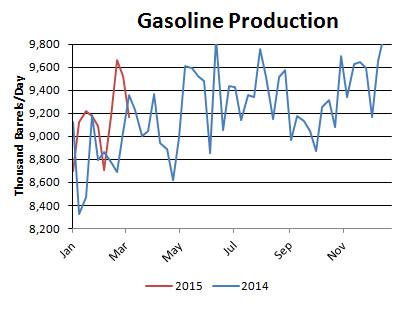

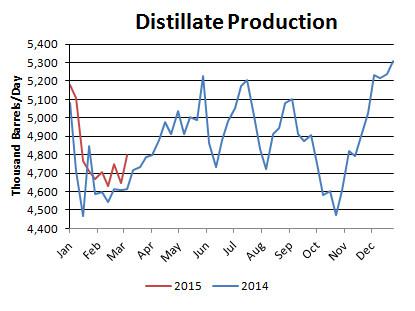

Refinery utilization ticked up from 86.6 percent to 87.8 percent. Utilization is above the year-ago level and above the five-year average. Gasoline production fell to 9.2 mmbbl/d, while distillate production rose to 4.8 mmbbl/d.

Miscellaneous

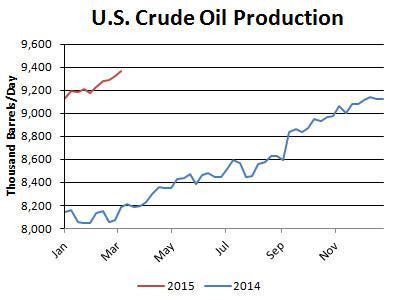

U.S. crude oil production increased to 9.37 mmbbl/d, a new multidecade high. Output has been rising swiftly due to surging production in unconventional oil plays. Since the start of the year, output has averaged 1.1 mmbbl/d, or 14 percent, above the same period a year ago.

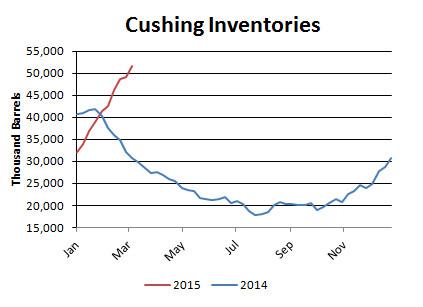

Inventories at the Nymex delivery point in Cushing, Oklahoma, rose by 2.3 million barrels to 51.5 million barrels, or 60.7 percent of the EIA's estimate of capacity. Overall, Midwest inventories rose by 1.6 million barrels to 134.9 million barrels, or 81.2 percent of estimated storage capacity.

Front-month WTI calendar spreads remained in contango at +$1.78.

Front-month Brent calendar spreads remained in contango at +$0.48.

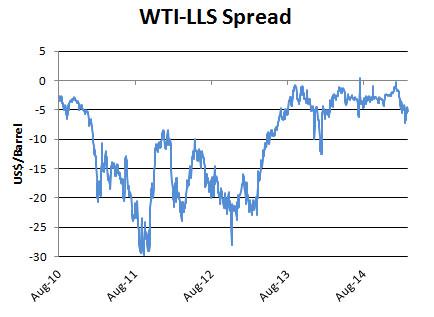

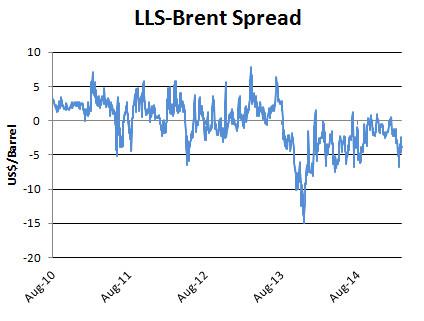

West Texas Intermediate's discount to Brent decreased week-over-week from -$9.77 to -$9.05. WTI's discount to Louisiana Light decreased week-over-week from -$6.35 to -$5.25.

The Baker Hughes oil rig count decreased by 64 to 922 rigs last week.

Baker Hughes Oil Rig Count

0 comments:

Publicar un comentario