The curse of the top dog

Apple’s low price-earnings ratio reflects understandable scepticism

Mar 7th 2015

.

APPLE’S growth record is staggering. The company’s share price has risen more than 300-fold since flotation. It recently became the first company in history to reach a market capitalisation of $700 billion, giving it a bigger value then the entire stock exchanges of Mexico, Russia or Saudi Arabia. In the first quarter of its current financial year, Apple generated more than $30 billion of cash. At that rate, it could pay off Greece’s entire debt burden within three years.

While sales of both the iPod and iPad have been slipping, more than 1% of the global population bought an iPhone in the latest quarter. Overall, sales were 30% higher than in the same quarter a year earlier. The next big hope is the Apple Watch, which may be unveiled on March 9th.

Back in the late 1990s, when the dotcom boom was in full swing, you would have expected a company growing that fast to have traded on a price-earnings ratio of 100, or at least 70-80. But at the start of March, based on earnings forecasts of $8.50 for the current year, Apple’s p/e ratio is just 15. That is the kind of rating given to a run-of-the-mill stock, not a turbocharged growth star.

This may reflect scepticism about whether the company can replace the iPhone with a hot new product: the watch may not do the trick. But investors may also be recognising an old problem.

Companies cannot grow for ever at the kind of pace Apple has been managing.

In his book “The Second Curve”, Charles Handy, a management guru, recounts seeing a graph in the office of IBM showing American GDP on one line and the company’s revenues on another. The latter were eventually projected to overtake the former. Mr Handy assumed the graph was a joke, but the Big Blue executives were serious. Nothing is more dangerous than the tendency to extrapolate from a recent trend.

At some point, a company will so dominate its market that further growth becomes impossible.

The executives may become complacent and fail to recognise the threat of new products and services. Think of how Nokia dominated the market for mobile phones, only to be caught out by the rise of first BlackBerry and then Apple and Samsung. It takes an enormous amount of willpower to respond to an evolving market by cannibalising your own product; few executives have been able to manage it.

Another option is for a big company to use its cash or shares to diversify into other sectors, but history suggests this approach has only a limited chance of success. The management usually spends too much money on the acquisitions and too much time trying to integrate the new businesses into the merged group. Even GE, the only survivor from the original list of companies comprising the Dow Jones Industrial Average back in 1896 (sadly, National Lead and Tennessee Coal & Iron are no longer with us), has made mistakes in its diversification strategy. Remember Kidder Peabody, the investment bank that it was forced to sell in the mid-1990s after large losses in bond trading.

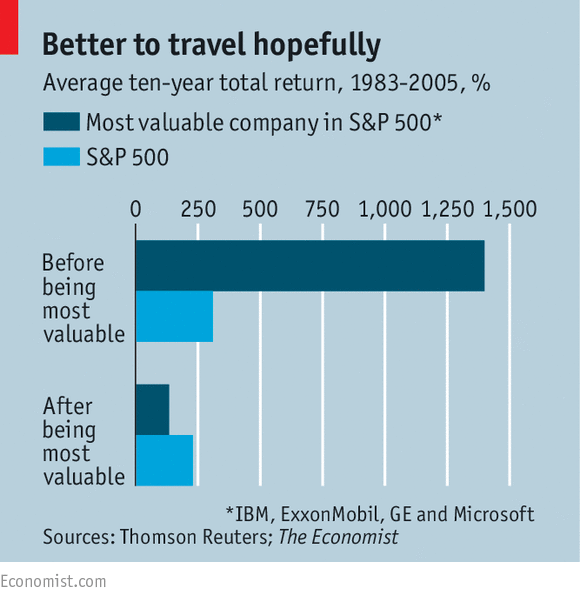

There seems to be an innate tendency for market giants to underperform (see chart). Between 1983 and 2005, the title of largest company in the S&P 500 switched between IBM, Exxon Mobil, GE and Microsoft. In the ten years before each became top dog, these stocks achieved an average return of 1,282%, compared with a return of 302% for the S&P 500 over the same period. But in the ten years after they reached the peak, the average return of the top dogs was just 125%, compared with 199% for the S&P 500.

The simplest explanation is that companies become “hot stocks” because of a combination of rapid growth in profits and a widely admired business model. This prompts investors to award the company a premium rating, pushing up its market value. By that stage, the company is vulnerable to disappointment: either its profits growth will falter or doubts will appear about its long-term potential. Profit forecasts will be reduced, or the multiple investors are willing to pay for those profits will fall.

Since Apple does not command that high a rating at the moment, investors are clearly dubious about its long-term growth prospects. After all, just to maintain its recent sales pace, it will have to sell 3 billion iPhones over the next ten years. And if the stock were to replicate the average 125% total return of previous top dogs, its market value would have to reach $1.4 trillion by 2025. Perhaps everyone will be wearing Apple watches and driving Apple cars by then. But history, and the stockmarket, suggest not.

0 comments:

Publicar un comentario