Greek Crisis Tests ECB’s Credibility

The central bank must decide if Greek banks should be allowed to use scarce liquidity to roll over their existing holdings of T-bills

By Simon Nixon

Updated March 15, 2015 10:14 p.m. ET

Greek Prime Minister Alexis Tsipras complains that the ECB has a noose around Greece’s neck because it won’t allow Athens to issue more short-term bonds. Photo: European Pressphoto Agency

Greek Prime Minister Alexis Tsipras complains that the ECB has a noose around Greece’s neck because it won’t allow Athens to issue more short-term bonds. Photo: European Pressphoto Agency Yet the banking union involved a far greater transfer of sovereignty than has been widely understood, arguably greater even than the creation of the euro itself. After all, the banking union has handed the European Central Bank, as the eurozone’s new single banking supervisor, powers that directly affect citizens’ property rights and the ability to take decisions with potentially far-reaching fiscal consequences.

Now, just four months after assuming its new powers, the ECB faces an acute test of its credibility in the shape of the latest Greek crisis.

The success of the banking union hinges on the ECB convincing markets that it offers a decisive break with a European past in which national authorities were seen as too susceptible to political pressure, too willing to overlook weak bank balance sheets to shield government balance sheets.

To break this toxic link between banks and sovereigns that has undermined trust in the eurozone financial system, the ECB needs to show that it can take decisions independent of political pressures.

Most analysts agree that the SSM has got off to a promising start. Last year’s asset-quality review and stress test of the balance sheets of the largest eurozone banks was seen as more rigorous than past European efforts. The ECB has also been using its discretionary powers to push banks to improve the quality of their capital, circumventing national opt-outs from the Basel framework that had been baked into European rules.

Recent moves by Spanish lender Banco Santander SA to raise capital, as well as steps to boost the capitalization of small Italian lenders, bear the hallmarks of the new regulator flexing its muscles.

But the Greek crisis has put the ECB in an uncomfortable position. Prime Minister Alexis Tsipras complains that the ECB has a noose around Greece’s neck because it won’t allow Athens to issue more short-term bonds. The ECB has defended its position primarily in terms of monetary policy: It says that allowing Greek banks to buy more T-bills would amount to central-bank financing of the government, prohibited by European treaties.

But as supervisor of the four largest Greek banks, the ECB faces an even more delicate question: Should Greek banks even be allowed to use scarce liquidity to roll over their existing holdings of T-bills?

Officials acknowledge that at a time of such acute stress, banks should ideally be cutting their exposures to illiquid government securities. Yet they also know that ordering banks to do so would have dire consequences for financial stability.

For the moment, the ECB is allowing banks to roll over T-bill exposures. But some officials say that the longer this continues, the greater the risk to the ECB’s credibility as a bank supervisor.

Meanwhile the ECB also faces another critical judgment: Do Greek banks have sufficient capital?

The economic crisis is already taking a clear toll on bank asset quality. Eurobank Ergasias SA, one of Greece’s largest lenders, said last week that its nonperforming loan ratio has already returned to comparable levels to the first half of last year, with arrears picking up on both mortgages and commercial loans.

Default rates will almost certainly worsen if the government starts delaying payment to its own suppliers because of a cash crunch, as seems likely given the lack of progress toward unlocking bailout funds.

Credit conditions are also likely to tighten as a result of the deposit flight since the start of the political crisis in December. Although outflows have stabilized since Athens signed a four-month extension to its current bailout program on Feb. 20, the Greek banks are still reliant on central-bank facilities for €100 billion ($104.96 billion) of funding, equivalent to almost 70% of Greek gross domestic product.

That suggests Greek banks will face a further period of deleveraging as they try to put their funding back on a sound footing.

And if Athens pushes ahead with a proposed new law outlawing foreclosures on some home loans, the banks will be forced to take further bad debt charges to reflect the weaker incentives for homeowners to honor their debts.

True, the four large Greek banks passed the ECB’s stress test last year and so far, any deterioration is within the range of the adverse scenario used in the test, say officials familiar with the situation. But the snag is that a large share of the capital held by Greek banks consists of deferred tax credits, which the ECB has indicated it doesn’t regard as sufficiently loss-absorbing to qualify as true core capital, since its availability depends on the ability of banks to generate profits for decades to come.

Strip out these tax credits and Eurobank’s core-capital ratio fell to about 5% at the end of 2014, notes Citigroup. That is far below the 10% standard for European banks.

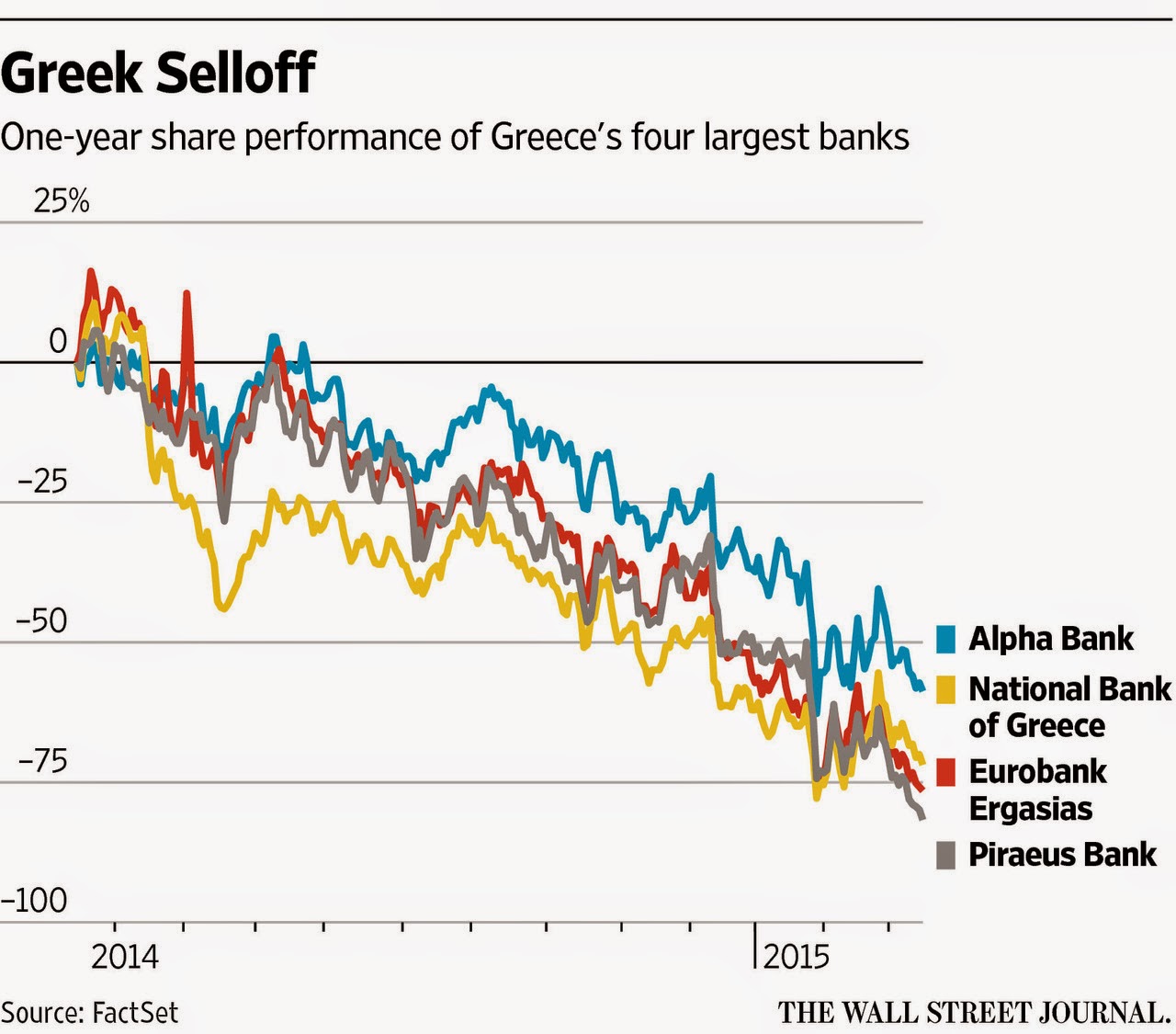

Not surprisingly, Greek bank stocks have lost up to 80% of their value in the past year and now trade at deeply distressed multiples.

Some central bankers believe that substantial capital injections into Greek banks may already be necessary. Yet the only plausible source of capital today is money earmarked for bank recapitalizations held by the Hellenic Financial Stabilization Fund. To access these funds, the banks would need the approval of the European Stability Mechanism, which in turn would require that Greece comply with its bailout program.

If HFSF funds weren’t available, any bank deemed to be inadequately capitalized would have to be resolved in line with the EU’s tough new bail-in rules, which could lead to losses for some depositors.

Of course, technocratic officials are reluctant to take decisions with such profound political implications. But the ECB also has an obligation to discharge its responsibilities independently and in accordance with eurozone laws.

The longer the impasse between Athens and its creditors continues, the greater the pressure on the ECB to act to safeguard its own credibility. After all, that was the point of the banking union.

0 comments:

Publicar un comentario