Feb. 4, 2015 8:22 PM ET

As much as €1.5 trillion ($1.7 trillion) of euro area debt maturing in more than a year now pays a negative yield, according to J.P. Morgan. That compares to none whatsoever a year ago.

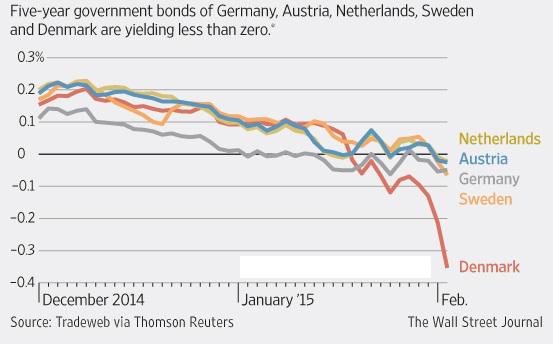

German government bonds offer negative yields on maturities up to six years, according to Tradeweb, along with those in Denmark. For five years, the Netherlands, Austria, Sweden and Finland are in the club. For four years, add France and Belgium. In Switzerland, bonds out to a whopping 13 years in length have negative yields.Approximately €220 billion in bank reserves are subject to negative deposit rates as well (this is actually less than it once used to be, as banks have moved excess reserves from the deposit facility to the current account facility at the ECB, which at least yields zero instead of the 20 basis point penalty rate applied to the deposit facility).

Source: moneyweek.com.

Source: moneyweek.com.In the meantime, the corporate bond market is also beginning to be infected by negative yield syndrome, while some covered bonds have traded at negative yields since September already, as Bloomberg reports:

Credit markets are being so distorted by the European Central Bank's record stimulus that investors are poised to pay for the privilege of parking their cash with Nestle SA.It should be noted that this is not only the ECB's doing. The SNB has lowered its three-month LIBOR target rate channel to a range from minus 0.25 to minus 1.25 percent (i.e., an average of minus 75 basis points), which may be of greater relevance to the market price of Nestle's debt.

The Swiss chocolate maker's securities, which have the third-highest credit ranking at Aa2, may be among the first corporate bonds to trade with a negative yield, according to Bank of America Corp.'s London-based strategist Barnaby Martin. Covered bonds, which are bank securities backed by loans, started trading with yields below zero at the end of September. (emphasis added)

Covered bonds are widely regarded as almost as safe as government bonds. This is due to the fact that issuers as a rule have to over-collateralize these bonds and look after the assets used as cover -- i.e., to replace any assets that become non-performing with performing assets.

Moreover, while assets in cover pools remain on the balance sheets of issuers, they are segregated in the event of an insolvency (regulations vary a bit from country to country, but this is the gist of them).

A sample of five-year government bond yields in Europe trading at negative yields to maturity:

Source: WSJ

Originary Interest vs. Bond Yields

As we have previously mentioned, the natural, or originary interest rate can never turn negative; this is so because time preference is an inviolable and universally valid category of human action. It is logically inconceivable for future goods not to be valued at a discount against present goods of the same type. Note that this has nothing to do with money -- the phenomenon of interest is at its root a non-monetary phenomenon. It simply concerns the valuation of future vs. present goods. As a reminder, here is a pertinent quote by Ludwig von Mises from Human Action:

Originary interest is not a price determined on the market by the interplay of the demand for and the supply of capital or capital goods. Its height does not depend on the extent of this demand and supply. It is rather the rate of originary interest that determines both the demand for and the supply of capital and capital goods. It determines how much of the available supply of goods is to be devoted to consumption in the immediate future and how much to provision for remoter periods of the future.

People do not save and accumulate capital because there is interest. Interest is neither the impetus to saving nor the reward or the compensation granted for abstaining from immediate consumption. It is the ratio in the mutual valuation of present goods as against future goods.

The loan market does not determine the rate of interest. It adjusts the rate of interest on loans to the rate of originary interest as manifested in the discount of future goods. Originary interest is a category of human action. It is operative in any valuation of external things and can never disappear.

If one day the state of affairs were to return which was actual at the close of the first millennium of the Christian era when people believed that the ultimate end of all earthly things mas impending, man would stop providing for future secular wants. The factors of production would in their eyes become useless and worthless. The discount of future goods as against present goods would not vanish. It would, on the contrary, increase beyond all measure.

On the other hand, the fading away of originary interest would mean that people do not care at all for want-satisfaction in nearer periods of the future. It would mean that they prefer to an apple available today, tomorrow, in one year or in ten years, two apples available in a thousand or ten thousand years.

We cannot even think of a world in which originary interest would not exist as an inexorable element in every kind of action. Whether there is or is not division of labor and social cooperation and whether society is organized on the basis of private or of public control of the means of production, originary interest is always present. (emphasis added)One example that shows why this must be so is the fact that the prices paid for productive land are finite. A piece of land producing an unchanging rent every year could not possibly have a finite price if there were no originary interest by which its future services are discounted; it would be impossible to value it. If originary interest were to disappear, land would only be bartered for other pieces of land, but would no longer be exchanged for anything else, including money.

How come then that numerous bonds are now trading at negative yields? There are several reasons for this. Central bank manipulation of interest rates is just one factor. We may assume that market participants are according a negative price premium (i.e., inflation premium) to bond yields at present, but that by itself can also not explain negative yields-to-maturity, as there is always the option of holding cash instead. In fact, superficially it seems a lot more sensible to hold cash rather than bonds with a negative yield, since one's purchasing power is certain to increase if there is indeed an economy-wide decline in prices.

Still, there must be reasons why people buy and hold bonds sporting negative yields. Some of these are technical, and some are connected with confidence issues and/or speculation.

Technically, there is for one thing the fact that banks don't have to reserve capital for assets they hold in the form of government bonds (which according to banking regulations, are considered "risk free"). Banks are also holding inventories of bonds for the purpose of using them as collateral in repo transactions. Since government bonds are considered "risk free," they are the type of collateral that is subject to the smallest haircuts in such transactions, which makes them desirable for this purpose. There are also market players such as insurance companies, that are practically forced by regulations to hold sizable portfolios of government bonds. These laws and regulations can be considered part and parcel of a "financial repression" scheme.

Then there are speculators who buy bonds at negative yields because they expect the trend to become even more pronounced. If e.g. a bond's yield-to-maturity falls from minus 10 to minus 30 basis points, they will make a capital gain. This is essentially the greater fool theory of bond buying, and it probably plays a not inconsiderable role in today's markets.

Germany's two-year government bond yield stands nearly at minus 20 basis points:

(click to enlarge)

However, a major motive driving the buying of bonds with negative yields is undoubtedly also a continuing lack of confidence in the banking system. Since it has not become common yet to charge holders of current accounts (as a rule, they still sport a small, but positive yield of 5 to 10 basis points), it would be more sensible to hold cash deposits instead of government bonds.

However, one would then be exposed to the counterparty risk associated with the bank.

The EU's new bank recovery and resolution directive mandates that before government support is extended to ailing banks, all other avenues must be exhausted first - and deposit holders are legally regarded as creditors of banks. This is actually a legal absurdity, but in a fractionally reserved system, banks no longer have merely a safekeeping function for funds entrusted to them that are ostensibly available on demand. Instead, they use them for the pyramiding of credit (and the consequent creation of additional deposit money from thin air).

These risks are especially pronounced for large depositors, as events in Cyprus have shown. Since holding cash currency is impracticable for large depositors (and would also involve costs), they rather buy government debt and accept negative yields in exchange for peace of mind. In principle there is of course nothing wrong with depositors being exposed to risk if they are voluntarily putting their funds into accounts with fractionally reserved banks. There is no reason why should taxpayers should bail them out. Anyway, the fact that governments are seen as safer debtors than banks is no doubt a major reason why some large investors prefer negative yielding government bonds (as well as covered bonds with their special safety features) over bank deposits.

Negative Yields and Gold

A friend recently asked us, "why not just buy gold"? Obviously, not every institutional investor can just buy gold, as many are prevented from doing so either due to government regulations or the stipulations of their investment mandate. Some however can, and individual investors definitely can do so. With government bond yields falling increasingly into negative territory, the opportunity cost of holding gold becomes negligible, as only storage and insurance costs remain to be considered.

The fact that investors are beginning to buy gold as an alternative asset that is not exposed to the banking system and not subject to any counterparty risk, is illustrated by the developing gold bull market in non-dollar currencies. Below is an updated chart of gold in euro and yen terms. Although a short term correction is now underway (as we recently pointed out, gold has become "overbought" in these currencies), the new trend can be clearly discerned:

Gold in terms of euro and yen:

(click to enlarge)

In Switzerland, there was also an uptrend in the CHF denominated gold price underway, which was interrupted by the SNB's decision to remove its currency peg. However, the trend has since then resumed. Also shown below is gold in terms of the Australian dollar. In terms of "commodity currencies" (meaning: the fiat currencies of countries that are large exporters of commodities) like the Australian and Canadian dollar, gold is rallying smartly as well, as the central banks of these countries have also embarked on rate cutting sprees. At least they still have minuscule rates that can be cut a bit, contrary to the ECB with its laughable 5 basis points main repo rate.

Gold in CHF and Australian dollars; the CHF gold rally was briefly interrupted by the de-pegging of the currency:

(click to enlarge)

Surely there are also other reasons why gold demand has increased, such as the uncertainty surrounding Greece after the election, the fact that confidence in central banks has been dented somewhat by the SNB's surprise move and the evident slowdown in global economic growth. It is impossible to tell which of these factors has played the biggest role in gold's recent rally, but we suspect that some $4 trillion in government debt globally now trades at negative yields is a quite significant factor.

Conclusión

The market distortions caused by central bank interventions and the lingering distrust of the banking system (especially in Europe) should be of concern to small investors as well. Regardless of near term price gyrations, gold provides excellent insurance for potential worst case scenarios. There is no guarantee whatsoever that government bonds will be forever regarded as "risk free" by market participants, on the contrary. The sovereign debt crisis in the euro area already showed that one cannot rely on that.

So is now a good time to buy gold? We would argue a good time to buy is whenever there seems to be little trouble on the horizon; once trouble becomes obvious to all, the price of insurance will no longer be cheap.

(Charts taken from BigCharts, WSJ, StockCharts.)

0 comments:

Publicar un comentario