Feb. 18, 2015 6:36 AM ET

Summary

- A good week for a weak commodity.

- An ugly medium-term picture.

- The global economic landscape is not positive.

- Dr. Copper is likely to be a patient.

A good week for a weak commodity

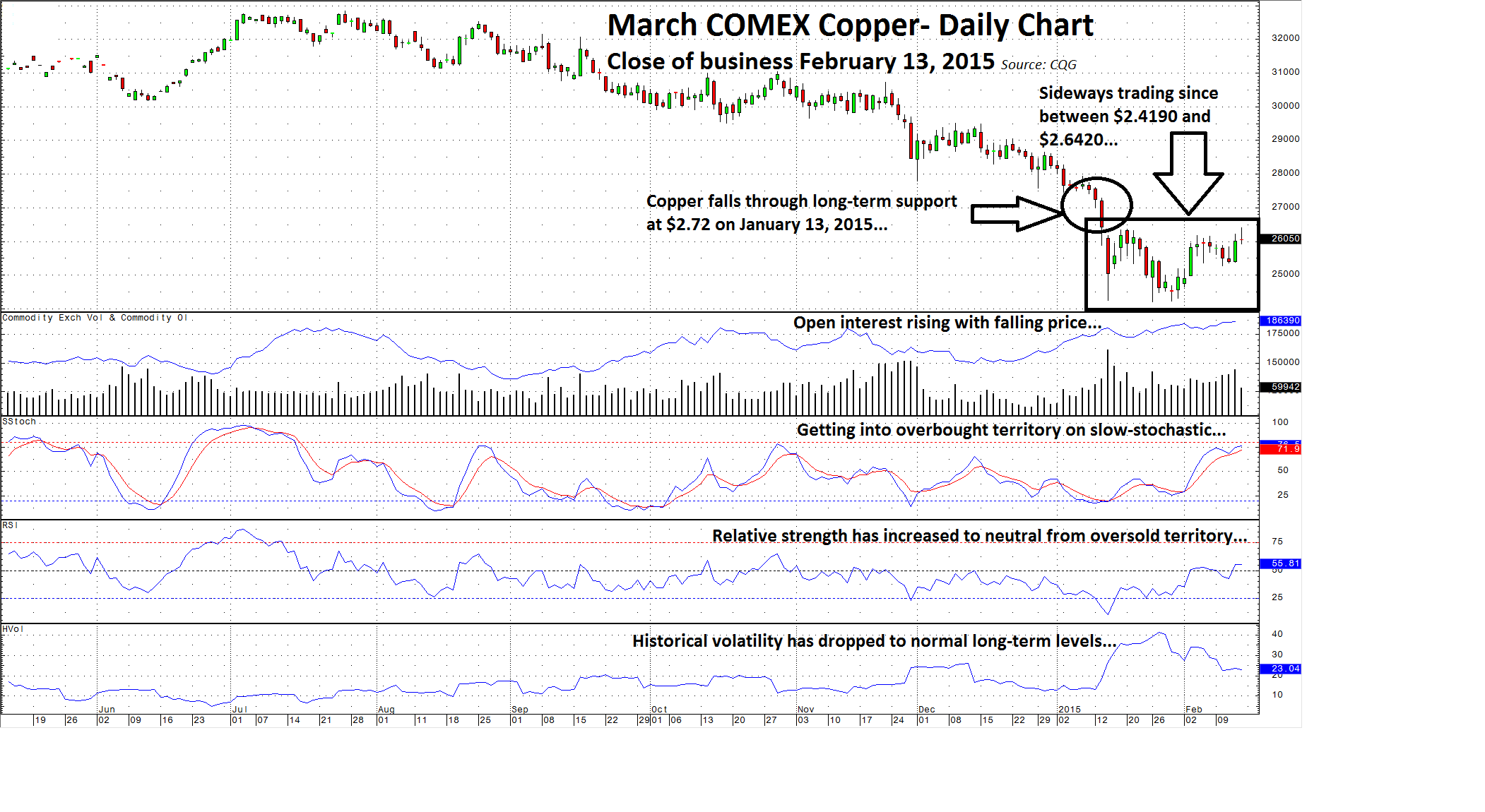

Copper did rally last week; it closed on Friday February 13 at $2.6050 per pound up 1.95 cents on the week.

(click to enlarge)

Since copper fell through support in January, it has been in a sideways trading range between lows of $2.4190 and highs (made Friday 2/13/15) at $2.6420. Copper continues to trade at the lowest price since the summer of 2009. Open interest, the total number of open long and short positions on COMEX copper futures, has increased as the price fell. Open interest currently stands at 186,022 contracts, which is an increase of just under 16% for 2015. A momentum indicator, the slow stochastic, is currently bullish reflecting the recent price recovery however it has moved into overbought territory. Relative strength for copper is neutral, recovering from oversold territory. After a spike in volatility when the price fell in January, daily historical volatility has dropped back down to 23% from over 40%, which is more reflective of historical norms and closer to monthly historical copper volatility, which currently stands at 17%. There is presently a mixed technical picture for copper, however, while the price has staged a recovery, it has yet to challenge the level from which it broke down and remains more than 10 cents below the $2.72 resistance level. The technical picture for copper is not very bullish nor is the fundamental state of the market at this point.

An ugly medium-term picture

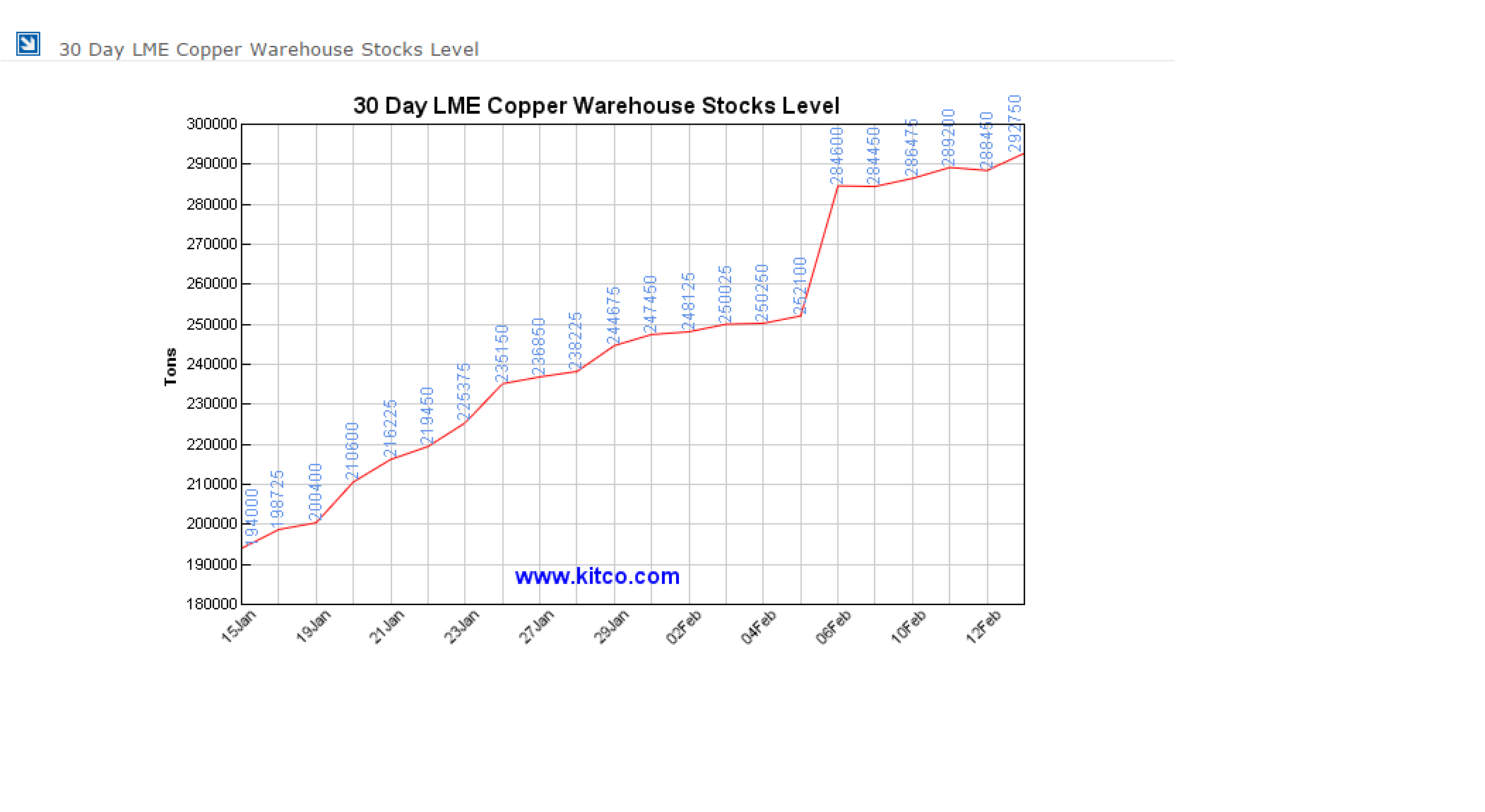

One of the problems facing many industrial commodities these days is rising inventories. We witnessed this in iron ore where increased production led to big inventories; lower prices followed. The same happened in crude oil where huge inventories caused prices to halve over a nine-month period. A quick look at a short-term trend in copper inventories held on the London Metal Exchange (LME) illustrates a similar problem for the red metal.

(click to enlarge)

Over the past 30 days, LME copper stocks have increased from 194,000 metric tons to 295,300 - an increase of over 52% in a month. Granted, some of the metal that has come into the official reported stock numbers was probably sitting in warehouses as off-warrant material but the increase is big enough for us to take notice.

China is the world's number one consumer of copper. Last year growth in China was a disappointment at 7.4%. The Chinese government recently announced a policy, which they call the "new normal." Under this policy, which tempers growth expectations, the government seeks Chinese growth at a sustainable pace. As part of the policy, the government will be stimulating the economy through lower interest rates and investing in the country while at the same time cracking down on corruption. This brings into question the practice of financing copper in China, which has created demand for the red metal in recent years. These financing deals used copper as collateral in order to arbitrage between interest rates in China and the rest of the world. China has cracked down on this practice after discovering that several of the financing deals were fraudulent. This has decreased demand for physical copper in China. At the same time, lower copper prices have affected collateral value in other financing deals forcing the sale of the copper held as collateral. This has increased copper inventories and led to lower prices.

Therefore, each time copper spikes lower, the potential for collateral liquidation increases. Given rising LME stocks, a slowdown and in some cases unwind of copper financing deals in China and a generally lethargic global economy, the medium-term picture for the red metal remains ugly.

The global economic landscape is not positive

Lower growth in China, the world's largest consumer of copper, continues to weigh heavily on the metal. Add to that deflationary pressures in Europe and the picture gets even bleaker.

While the United States is a bright spot in the global economic landscape, the industrial demand for copper on a global basis is likely to continue to suffer. While interest rates will remain low in Europe due to the recently instituted policy of quantitative easing and rates may move lower in China, copper continues to be a dollar-based commodity. As such, the prospect for higher short-term U.S. interest rates is yet another negative for the red metal.

Lower energy prices will cut the overall production cost for copper. However, major producers are likely to sell more metal as the price moves lower in order to secure market share and keep cash flow levels stable. Codelco, the Chilean company that is the world's largest copper producer, recently announced it is planning to reduce costs by $1 billion in 2015. The company plans to trim costs by renegotiating energy expenditures due to lower oil prices and by boosting copper production by 35,000 tons this year. Codelco's CEO Nelson Pizarro recently told reporters that the slump in the price of copper is not dampening their expansion plans. By 2018, the company plans to invest $22 billion in its mining operations. Codelco produces roughly 10% of the world's annual copper supply, and to maintain market share, they need to expand operations and replace mines with dwindling ore grades with new ones in order to stabilize and increase annual output. Other top copper producers including BHP Billiton (NYSE:BHP) (NYSE:BBL), Rio Tinto (NYSE:RIO), Glencore (OTCPK:GLNCY) and others are all investing in new copper mining projects around the globe in order to boost production. These low-cost producers are likely to sell more copper the lower prices fall to maintain market share and force high-cost producers out of the game.

Dr. Copper is likely to be a patient

While copper is struggling to crawl back up to the price level it broke down from last month, the fundamental picture continues to look bearish. A combination of factors is likely to weigh on the price of the red metal in coming months. Continued global deflationary pressures, lower growth in China, a crackdown on financing deals using the metal, lower production costs and producers willing to sell more metal at lower prices is not bullish for the red metal.

Right now, it seems that the global economy is the doctor and copper is the patient, the prognosis is not positive for the medium term. I expect the price of copper to continue to fall in 2015; my initial target is the $2 per pound level. There is more red ink in store for the red metal this year

0 comments:

Publicar un comentario