Jan. 25, 2015 1:36 AM ET

Summary

- This week we have begun to see signs of risk-on in the broad market, and the safety trade into gold is weakening.

- The upcoming Greek election on Sunday, and to a lesser extent the Federal Reserve meeting on 27/28 Jan, may result in some gold price volatility.

- I believe we are very close to at least a local top in the gold price, and expect a decline to start within the next week.

This week gold did not make huge swings, opening at $1280 and finishing at $1294, and with not much in between. Whilst I can see us achieving a small further gain early on in the week, I maintain that we are close to at least a local top, and potentially the start of a decline to new lows.

Although the last 7 days have been quiet, there have been some big changes to positioning within the market, and announcements made regarding Central Bank policy.

Let's review some of the items mentioned last week:

Is The Safety Trade Over?

Last week I talked about upcoming decisions being made by the ECB and the potential for a 1T EUR Quantitative Easing programme, with a view to the effects this would likely have on currency and by extension upon gold (NYSEARCA:GLD). My feeling was that any move by the ECB to start buying bonds would weaken the Euro further, prompt the Dollar to rise, and put pressure on gold bulls.

On Wednesday we had a soft announcement by two ECB board members hinting to the press that they would indeed start a round of QE at €50B per month, and in a move no doubt designed to add a little cherry to the top of the equity rally cake, Mario Draghi announced on Thursday that the ECB would buy not €50B but €60B of bonds each month starting from March this year through September 2016.

The European equity markets had been rallying for days prior to the shock announcement that the whole world knew was coming, but of course they rallied further on the news, and we are now seeing signs of risk-on behaviour across the board.

Volatility within equity markets due to changes in central bank policy seems to be receding - I say seems because when the announcement was made, initially there was a pronounced nervousness displayed by the US indices to join the rally party, and I remain unsure about the prospects of a sustained forthcoming rally in the S&P500.

The question we now need to answer is whether the safety trade is over and buyers of gold will dry up.

Prior to the official announcement, gold broke support and dropped to $1279, but then quickly rallied back up to $1308 as the S&P500 (NYSEARCA:SPY) bobbed up and down looking for clear direction. However, when the equity markets really got going, gold fell to $1284 but finished the week at $1294 for a gain of just over 1%.

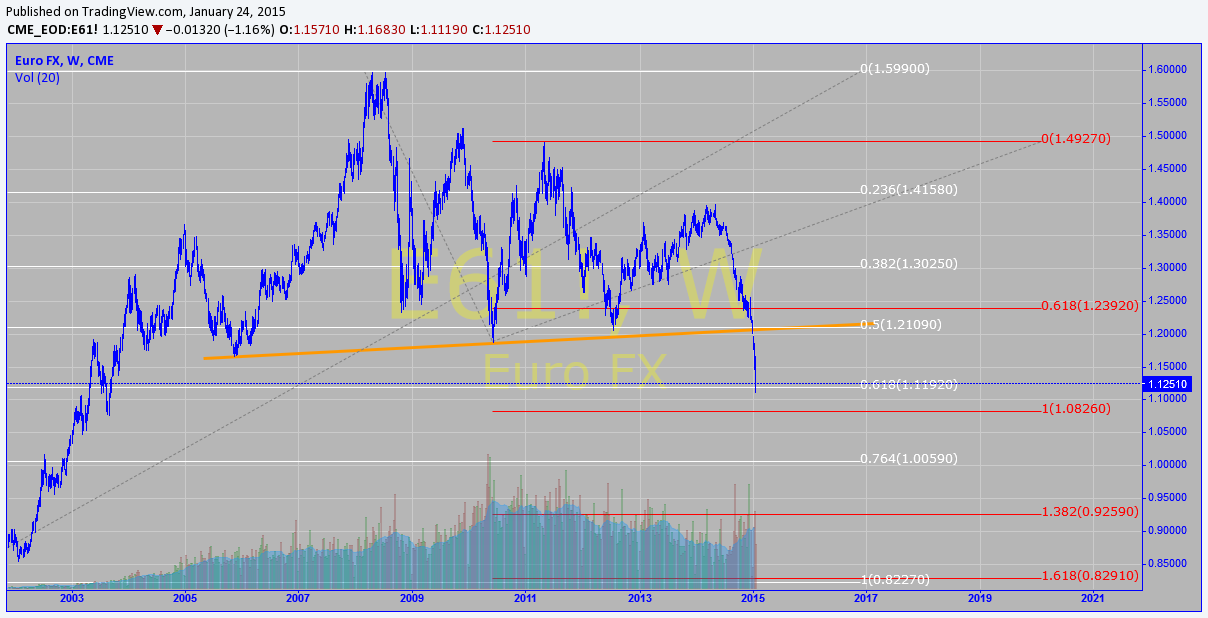

As expected the Euro dropped, but fell further and faster than the week before, briefly piercing the 1.1192 level given in my last article which suggests the level won't hold in the future. This is looking more and more like a slow motion train wreck each time I go to check the chart:

(click to enlarge)

I keep hearing people say they expect a bounce soon and are looking to buy, but I would caution them not to catch this particular knife - in my opinion the Euro is going much lower much quicker than people seem to realise.

On the back of the drop in the Euro the US Dollar rose and put some pressure on the gold price, but this only became evident when US markets started to rally hard, indicating that the safety play is more about equity market performance than dollar movement.

Whilst I am not discounting the potential for further gold volatility on Fed day this coming week, in the main I feel we now have only one last hurdle to jump which is of course the Greek elections this Sunday.

As I write this article (Saturday) Reuters is reporting a lead in the polls for Syriza, and stating they look odds on for a win. I believe this could result in a short term spike up in the gold price, before gold completes this rally and begins to decline, and I will personally be using this Sunday night spike (if it comes), and/or movement on Fed day, to add to my short positions.

Will the Dollar Pull Back Soon and Ease Pressure on Gold?

This is another assertion I am hearing a lot, whereby folks seem not to believe in the veracity of this rapid rise in the US Dollar, and expect it to collapse any moment now. I can understand this attitude to some extent, as the Daily Sentiment Indices point to an unhealthy number of US Dollar bulls and the trade has become massively over-crowded, but trade is not the only consideration here.

In previous articles I touched upon the dollar being the safe haven of choice, and those watching their domestic currencies decline would seek shelter in a currency that is strengthening against their own.

Additionally, the US bond and equity markets have far outperformed their rivals overseas and this makes them more attractive to foreign investors, so a greater percentage of capital is buying dollar denominated assets rather than those available in their own countries.

All of this is absolutely true and I expect the trend to carry on, but there is another reason for dollar strength. When the Fed lowered interest rates, the US Dollar became attractive to those wishing to issue debt, as to many it would mean having to pay less interest than if the bond was issued in their own domestic currency. Depending on where you get your statistics from, non-domestic USD debt is quoted as being anywhere between 6 and 9 Trillion dollars.

Obviously, if the bond is dollar denominated, repayments have to be made in dollars also. Those issuers who have failed to use the money in an activity that generates dollar income will be converting their own currency into the dollar to make these repayments. If the dollar weakens it means they convert less of their own currency; if the dollar strengthens they effectively pay more.

This makes them net short the dollar overall i.e. the more the dollar strengthens, the more expensive the debt gets to keep servicing, and the more they lose on the deal. I believe this situation, coupled with all the other reasons people have for buying dollars or dollar denominated assets, is the real reason that demand for dollars is growing at an exponential rate and will continue to do so.

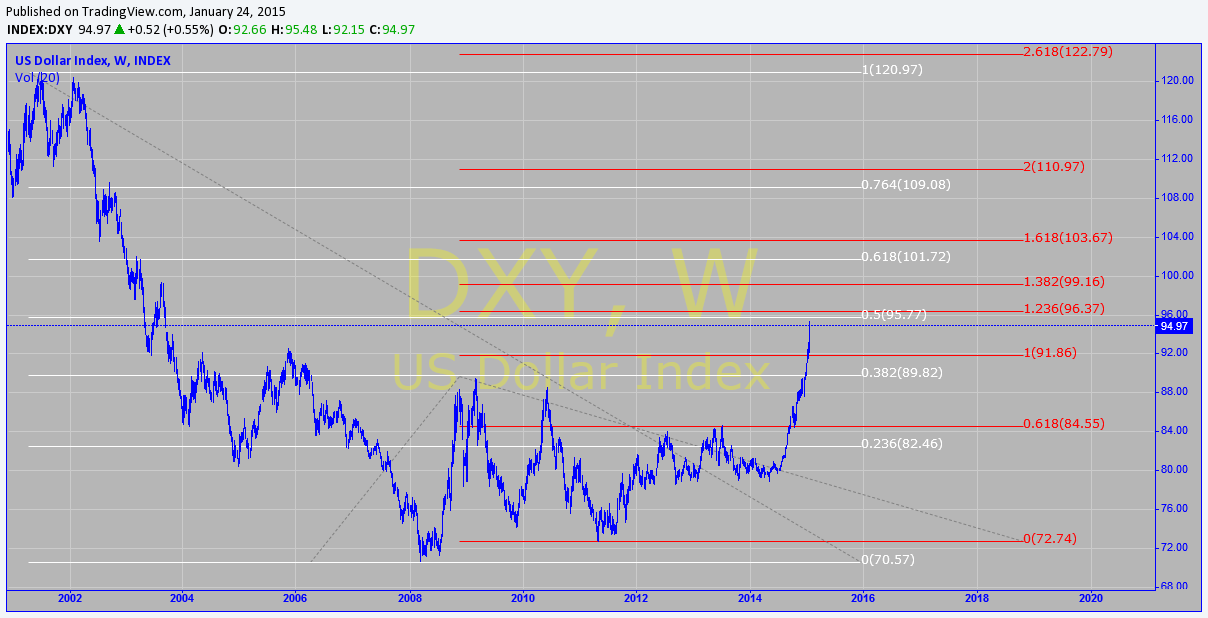

This is evidenced on the chart below, which in normal circumstances would have at least pulled back a little to work off overbought technical readings, but just keeps moving higher:

(click to enlarge)

As with those thinking of buying the Euro, I would caution people not to try shorting the Dollar.

While there may be small corrections in store, I expect these to be shallow and brief before climbing further, eventually testing the 120 level and conceivably breaking higher.

With the kind of strength I am expecting in the US Dollar, and the fact that the safety trade appears to be over, I find it hard to believe that gold will continue to rise at the same time.

Should there be further Central Bank shocks we may get short covering rallies in gold to get the bulls all fired up, but I think the overall trend is still down, and that gold will eventually make new lows as a result.

Data Points

For those wishing to see an explanation of some of the data points we are about to cover, please click here.

GOFO

There is currently no backwardation in place at present, and this is despite the rally gold has achieved in a relatively short space of time. It indicates that there remains ample physical supply on the market and suggests that the rally was fuelled by speculative buyers of paper contracts, rather than a bigger entity buying more than normal levels of the actual metal.

When the SNB shocked the market, and equity markets were on the downturn, it triggered a run to safety and gold was a recipient. If a government had wanted to shore up their own currency with an extra purchase of gold, it is likely we would have seen negative GOFO rates at least temporarily.

My own opinion is that the calls purchased that drove the price of gold higher are in the weaker type hands, and any subsequent decline in the price will trigger selling.The Commitment of Traders report seems to agree.

COT

I have been waiting all week to see the results of Friday's COT report. Like many who commented on last week's article, I expected to see a huge change in positioning based upon the volatility we experienced. I don't think people will be disappointed, well perhaps the bulls may be:

| COMMERCIAL | LARGE SPEC | SMALL SPEC | |||

| LONG | SHORT | LONG | SHORT | LONG | SHORT |

| 120,946 | 298,756 | 223,257 | 60,802 | 43,445 | 28,090 |

| CHANGE | CHANGE | CHANGE | CHANGE | CHANGE | CHANGE |

| -8,490 | +31,644 | +30,298 | -1,931 | +4,461 | -3,444 |

As we can see from the table above, rather than lightening up on their short contracts and getting more long as many expected, for the 4th week running the Commercials increased their net short position, this time to the tune of 40,000+ contracts - the biggest one week change I can remember in some time.

The last time the Commercial category had this number of short contracts on their books, we were one week away from the top at $1395 in mid-March 2014. Gold subsequently declined to the lowest point to date in this bear market (our $1132 November low) over the next 8 months.

Last week I noted that the commercial positioning leads me to believe that they see lower lows on the horizon for gold, and the numbers this week reinforce that statement. Do you really think the historically most successful trader category would be positioned as such if they believed gold to have bottomed at $1132?

Certainly we can rally higher over the next month or so, but all in all I am happy to maintain the view that we are not yet ready to start the next phase of the bull market, and will eventually see lower gold prices.

Miners

Both the gold mining majors (NYSEARCA:GDX) and the juniors (NYSEARCA:GDXJ) made losses overall last week despite the net gain for gold. As noted in previous articles, this is not unusual as stocks tend to lead the commodity, and gold mining shares often start their declines prior to the decline in gold.

If we do get a further spike up in gold early this week, we may find GDX rises a little higher, but I would be surprised to see it break the 23.50 level, and there is a relatively good chance it has topped already.

For GDXJ the equivalent level is 31.75 but with the juniors I feel that it is more likely they have topped and started their decline. Their underperformance of late is a growing sign that people are not prepared to take the same level of risk as they perhaps might with the majors, and is further evidence that we may be seeing a local top in gold sometime soon.

Some of the industry heavyweights are very close to long term resistance with this rally we have seen in January, and unless they can breakout above resistance it is likely that GDX will stall without their participation.

Considering everything written above, I am relatively sure we will be seeing a decline in the mining ETFs this week.

Gold Chart

Gold is very close to resistance here, and although I think it has a decent chance of going a little higher, I would be surprised to see it break the July 2014 $1345 high. Fibonacci resistance starts at $1313, moving up to $1340, and we have trendline resistance currently at $1328.

(click to enlarge)

Thus far we have nothing clearly indicating a local top has been achieved, but we have now gone as high as $1308 which is very close to our first fib target, so I cannot rule it out completely. It is not an easy call, as with the Greek election on Sunday we may see that panic spike higher to complete the move, and then start our decline.

Once we do have a confirmed top in place, I believe we will head to $1231 reasonably quickly.

The form of the decline will dictate whether or not we go higher after that. A corrective decline could see us holding support and rallying up as high as $1430 to complete wave 4, whereas an impulsive decline would indicate wave 4 is complete and could see us heading to test the November low, and possibly make new lows. As usual I will update thoughts and charts in the comments section throughout the week.

I wish everyone Good Luck in their post-Greek election trading!

0 comments:

Publicar un comentario