Take your pick

The key to stockmarket success is avoiding the worst sectors

Dec 6th 2014

THE collapse in the oil price is a useful reminder for investors that it helps to pick the right industries. As of December 2nd, global energy stocks were down 8.7% on the year, lagging nearly 31 percentage points behind returns in the best-performing sector of the year, health care.

This divergence between sectors is relatively mild by historical standards. In 2013 there was almost a 39-point gap between the best performer, retailing, and the worst performer, materials, a portmanteau category covering miners, chemical manufacturers and the paper and packaging industry. Robert Buckland, an equity strategist at Citigroup, says that big relative moves among sectors tend to be a function of volatility, and 2014 has been a reasonably calm year.

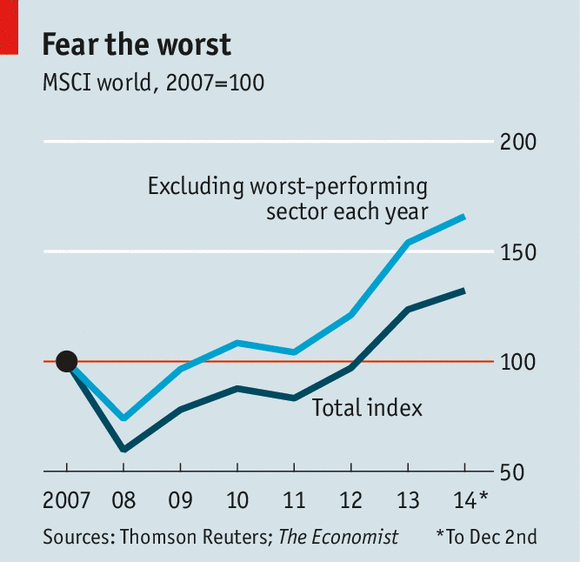

Nevertheless, it pays to avoid the laggards. The Economist’s hypothetical prescient investor, Felicity Foresight, would have earned a return of 66% since the start of 2007, had she simply steered clear of the worst-performing sector each year. That is more than double the 32% return of the MSCI World index over the same period (see chart).

Of course, sectors are not the only important factor. Investors would have done even better if they had got out of equities altogether in 2008. But many managers do not have that option; they run mutual funds that are devoted exclusively to stocks and cannot switch into bonds.

Get your economic calls right and the sectors tend to select themselves, says Chris Watling of Longview Economics, a consultancy. The big themes in recent years have been the financial crisis and the subsequent sluggish performance of first developed, and then developing, economies. That has favoured those sectors which are more defensive in nature. People will always be sick, so health care companies will always have a market (the introduction of Obamacare seems to have been no problem for the sector). The same can be said for consumer staples (a group that includes packaged foods, soft drink manufacturers and, er, tobacco). These two sectors have been the best performers since the start of 2007.

But even investors who correctly anticipated these developments may have been caught out from time to time by huge swings in sentiment. Global financial stocks may be lower than they were at the start of 2007, but they were the best-performing stocks of 2012. The materials grouping has been either the best or the worst sector in four of the last eight years.

Both sectors are volatile by their very nature. Financial stocks (or at least, the banks) are highly indebted; materials firms are very dependent on the economic cycle.

Another sector which has had its moment in the sun (topping the charts in 2010 and 2013) despite its dependence on the health of the economy has been the consumer discretionary group. This includes car manufacturers, entertainment and restaurants, and thus is vulnerable when wallets are being squeezed.

Most fund managers don’t tend to think of themselves as sector selectors, but as stock-pickers. They like to pore over balance sheets, visit factories and spot the best management teams. But sometimes they can drift into making sector-based bets. At the end of 2006, Buttonwood heard Bill Miller, Legg Mason’s star fund manager, recount his top bets for 2007, which included a lot of housebuilding companies. He then loaded up on financial stocks when they started to fall. Both bets went disastrously wrong.

In the late 1990s it was impossible not to be a sector selector. As a fund manager you were either a believer in TMT (technology, media and telecom) stocks or you were not; if the latter, you lost your job and if the former, you lost your clients’ money when the bubble burst. The gap at the time between best and worst performers was over 100 percentage points.

Since then, technology has lost some of its “wild West” aura. At the height of the dotcom boom, companies were being floated with barely any revenues, let alone profits. Investors are still happy to buy loss-making companies in the hope that they will eventually come up with a way of turning user enthusiasm into revenues—take Twitter, for example. But investors have an example of the way that social media websites can be monetised in the form of Facebook. And whereas valuations in the late 1990s were stratospheric, the price-earnings ratio on the global-technology index is currently 22. It is a sign that the tech sector has matured that it has not been the best or worst performer in any of the last eight years; no longer does a manager’s reputation depend on calling it right.

This divergence between sectors is relatively mild by historical standards. In 2013 there was almost a 39-point gap between the best performer, retailing, and the worst performer, materials, a portmanteau category covering miners, chemical manufacturers and the paper and packaging industry. Robert Buckland, an equity strategist at Citigroup, says that big relative moves among sectors tend to be a function of volatility, and 2014 has been a reasonably calm year.

Nevertheless, it pays to avoid the laggards. The Economist’s hypothetical prescient investor, Felicity Foresight, would have earned a return of 66% since the start of 2007, had she simply steered clear of the worst-performing sector each year. That is more than double the 32% return of the MSCI World index over the same period (see chart).

Of course, sectors are not the only important factor. Investors would have done even better if they had got out of equities altogether in 2008. But many managers do not have that option; they run mutual funds that are devoted exclusively to stocks and cannot switch into bonds.

Get your economic calls right and the sectors tend to select themselves, says Chris Watling of Longview Economics, a consultancy. The big themes in recent years have been the financial crisis and the subsequent sluggish performance of first developed, and then developing, economies. That has favoured those sectors which are more defensive in nature. People will always be sick, so health care companies will always have a market (the introduction of Obamacare seems to have been no problem for the sector). The same can be said for consumer staples (a group that includes packaged foods, soft drink manufacturers and, er, tobacco). These two sectors have been the best performers since the start of 2007.

But even investors who correctly anticipated these developments may have been caught out from time to time by huge swings in sentiment. Global financial stocks may be lower than they were at the start of 2007, but they were the best-performing stocks of 2012. The materials grouping has been either the best or the worst sector in four of the last eight years.

Both sectors are volatile by their very nature. Financial stocks (or at least, the banks) are highly indebted; materials firms are very dependent on the economic cycle.

Another sector which has had its moment in the sun (topping the charts in 2010 and 2013) despite its dependence on the health of the economy has been the consumer discretionary group. This includes car manufacturers, entertainment and restaurants, and thus is vulnerable when wallets are being squeezed.

Most fund managers don’t tend to think of themselves as sector selectors, but as stock-pickers. They like to pore over balance sheets, visit factories and spot the best management teams. But sometimes they can drift into making sector-based bets. At the end of 2006, Buttonwood heard Bill Miller, Legg Mason’s star fund manager, recount his top bets for 2007, which included a lot of housebuilding companies. He then loaded up on financial stocks when they started to fall. Both bets went disastrously wrong.

In the late 1990s it was impossible not to be a sector selector. As a fund manager you were either a believer in TMT (technology, media and telecom) stocks or you were not; if the latter, you lost your job and if the former, you lost your clients’ money when the bubble burst. The gap at the time between best and worst performers was over 100 percentage points.

Since then, technology has lost some of its “wild West” aura. At the height of the dotcom boom, companies were being floated with barely any revenues, let alone profits. Investors are still happy to buy loss-making companies in the hope that they will eventually come up with a way of turning user enthusiasm into revenues—take Twitter, for example. But investors have an example of the way that social media websites can be monetised in the form of Facebook. And whereas valuations in the late 1990s were stratospheric, the price-earnings ratio on the global-technology index is currently 22. It is a sign that the tech sector has matured that it has not been the best or worst performer in any of the last eight years; no longer does a manager’s reputation depend on calling it right.

0 comments:

Publicar un comentario