Dec. 19, 2014 4:00 PM ET

Summary

- Weak oil prices can be attributable to a strong dollar, to weakening demand expectations and to oversupply.

- Of the three drivers, the impact of supply growth is predominant.

- A recovery in prices is dependent on either demand pickup or on unanticipated supply cutbacks.

Here is an (inconvenient) fact: the Joe Friday character from the "Dragnet" radio and TV series never actually made the request for "just the facts, ma'am". That's too bad, because in the current febrile circumstances of the oil market, investors need to remind themselves of the facts, rather than wading through the morass of interpretations peddled by the chattering classes.

There are three fundamental reasons for weak oil prices:

- a dollar effect,

- weakening demand, and

- accelerating supply.

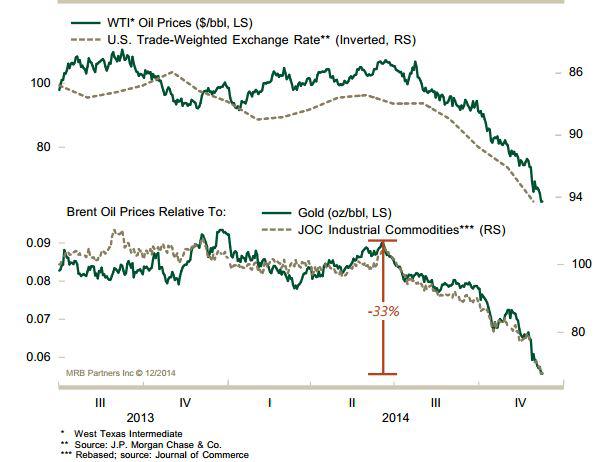

The strength of the dollar plays a significant role in the weakness of oil prices. Crude oil is denominated in dollars. The trade-weighted dollar has appreciated by some 12% since the summer, which implies that this factor alone accounts for a fifth of the decline in oil prices. When pricing oil in terms of gold, or a basket of industrial commodities, it has fallen in value by a third since the summer. Net-net: somewhere between 20% and 40% of the decline in oil price can be attributed to shifts in currency and relative prices.

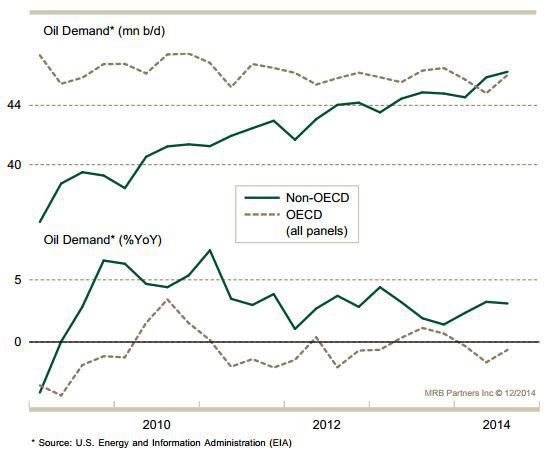

The second contributing factor to weak oil prices is demand. Not actual, observable demand, but rather expectations of demand. When it comes to the actual consumption of oil, there is nothing in the data that would justify the price waterfall. In fact, oil demand in both OECD and non-OECD economies has perked up in the past couple of months (which is partly a seasonal effect). Note that demand from the non-OECD part of the world now exceeds demand from the industrialized economies.

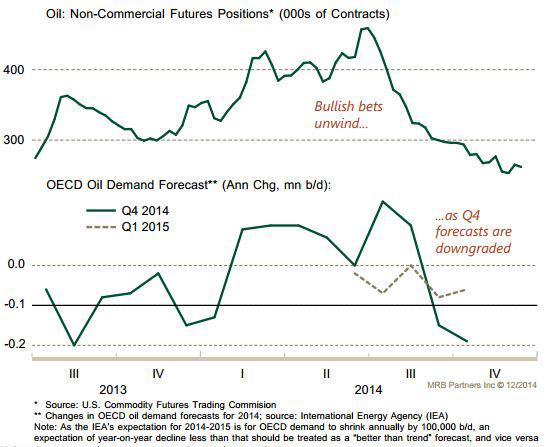

It is only when looking at demand expectations that there is an obvious link to prices and market behavior, although even here there is an important caveat to be considered. Q4 demand expectations for the OECD (which is the most volatile component of demand and which therefore has the greatest impact on pricing) started being downgraded rapidly as of September, and this coincided with a clear downturn in speculative positioning in oil futures.

However, note that demand expectations for the first quarter did not materially change during this time. Net-net: to the extent that demand expectations played a role in bringing down price, this is no longer the case now.

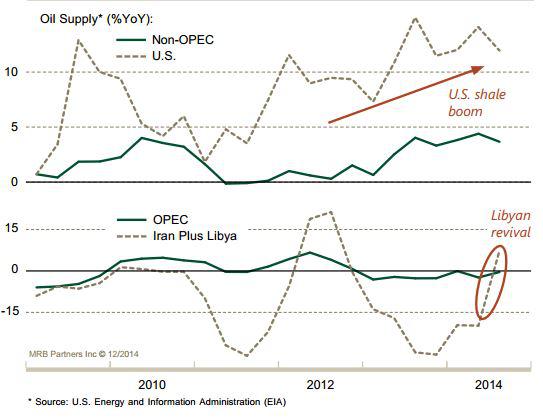

The third, and dominant driver, of current oil prices comes from the supply side. Supply has been growing rapidly, and there is little in the short-term that will threaten that. The strongest component of supply growth is the U.S. shale patch, and in general terms, non-OPEC output is leading the charge. But OPEC is not yielding ground, maintaining its overall output despite the geopolitical events that have in recent years kept significant portions of Libyan and Iranian crude off the market.

Libya's surprise summer return to the market, in the midst of a vicious civil war, was the straw that broke the camel's back, and tipped oil prices over the waterfall.

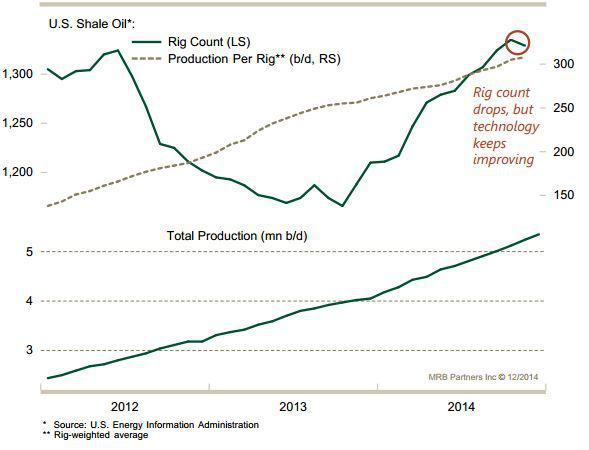

As all investors will by now have realized, U.S. shale oil is price sensitive. With current prices below average breakevens, this should be expected to have an impact on investment in the sector. And indeed, drilling activity dipped in November for the first time in two and a half years. But cutting the rig count does not mean cutting output, even though the production profile for each well is very short. Technology is rapidly evolving, so output per well is driving output ever higher, even with lower rig counts.

Net-net: Non-OPEC supply growth will eventually taper off, led by U.S. shale and reinforced by weaker output from other high-cost oil producing regions. But this effect takes time before it will have a meaningful impact in mopping up excess supply and stabilizing price.

What could change? Running through the logic of what drove prices down, a reversal in any of these factors would clearly support a price bounce. Furthermore, with oil so clearly oversold, any such shift in fundamentals would likely be reinforced by short-covering.

Could the dollar weaken? This seems unlikely in the run-up to a likely Fed rate hike in mid-2015, while other major central banks are still in ultra-accommodative mode.

Could demand expectations improve? This has a decent chance of occurring, at least in the U.S. economy, where retail gasoline prices are most closely aligned to crude oil prices. Watch indicators such as auto sales, miles traveled and overall personal consumption expenditure for clues of accelerating oil demand in the U.S.

Could supply drop? As suggested already, this is more of a long-term backdrop, as far as concerns U.S. shale oil. However, there are a host of unanticipated and largely geopolitical events that could contribute to removing excess supply. Three of the most prominent are:

- Libyan supply is inherently unpredictable and could collapse at any moment according to military developments on the ground.

- Venezuela is plagued by electricity shortages and the ruling party is literally at war with itself: some kind of political or infrastructure-driven disruption in output is highly likely.

- Geopolitical conditions in Saudi Arabia are a tinder box and a restive population and constrained budget represent the potential fuel for social unrest. The Saudi king is ill, the succession is fraught with complexity, the possibility of attacks by jihadist elements is ever present. Newsflow could trigger headlines that are supportive of oil prices at any moment.

0 comments:

Publicar un comentario