Covert operations

China’s central bank is wary of easing monetary policy, but that is what the economy needs

Nov 22nd 2014

BEIJING

.

IN BEIJING, a city of grandiose government offices, the central bank stands out for its modesty. Its headquarters are small and dated; plans for a big, gleaming extension have so far come to nothing. Cramped as they are, however, these digs are an apt symbol of the central bank’s restraint.

For nearly four years the People’s Bank of China (PBOC) has classified monetary policy as “prudent”, which is supposedly a neutral stance—not too tight, not too loose. In reality it has been tightening, to cool an overheated property market and slow the alarming accretion of debt. At the same time, the central bank has chipped away at vestiges of central planning with changes to its currency and interest-rate regimes. The PBOC is far from independent, but under Zhou Xiaochuan (pictured), its governor since 2002, it has acquired real clout as it has doggedly pursued its dual objectives of restraint and reform.

These two aims were complementary in 2011, when the central bank first embraced prudence. Nominal growth was still running at 18%, a heady pace even by Chinese standards; slowing breakneck investment was essential. Yet times have changed. The economy is now on track for its weakest year since 1990, sliding below the government’s goal of 7.5% growth; inflation is at a five-year low, nearly two percentage points below the official 3.5% target. The central bank faces mounting calls to lower rates. But advisers say it fears sending the wrong message: by easing, it might signal an end to restraint and, by extension, to reform.

The central bank’s answer to this dilemma has been to loosen monetary policy, but in a covert fashion. It lent the state-owned China Development Bank one trillion yuan ($163 billion), according to rumours that dribbled into local media in June. Some likened it to Chinese-style quantitative easing (QE): the central bank had in effect printed cash to rev up growth. But whereas central banks in developed economies have explained every step of their QE schemes to markets, the PBOC did not even bother to announce its activity.

Then, in September and October, it launched a “medium-term lending facility”, injecting a further whack of cash—769.5 billion yuan, it turns out—into the economy via loans to commercial banks. Rumours spread for weeks before the central bank confirmed them on November 6th. As for the initial trillion-yuan loan, it eventually acknowledged the operation, though declined to say how much it had lent, at what rate or even to which bank.

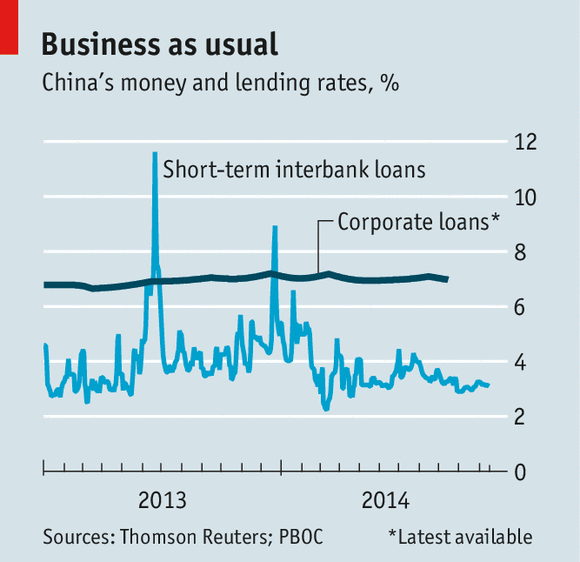

The combined amount of the infusions, if as big as reported, would be huge—equal to more than three months of America’s now-completed QE scheme when it was at its height, or to five months of Japan’s current programme. The impact of China’s easing, however, has been underwhelming. It has not reached the real economy. Short-term interest rates have fallen: a closely watched interbank rate is down by almost two percentage points this year, to 3.2% (see chart). But the rate at which banks lend to businesses, which matters more for growth, has remained stuck at about 7%.

The central bank’s lack of transparency has sown confusion. “The more policy tools you have, the harder it is to predict changes in any one of them,” says Song Yu of Goldman Sachs. A recent Barclays survey ranked the PBOC third-worst of 14 big central banks in terms of communication, behind only Turkey’s and Russia’s.

Even when providing partial confirmation of its covert easing, the PBOC’s message was muddled. The purpose was “to guide banks to lower lending rates”, it said, an apparent indication of an intention to relax policy. But in the next breath it added that the easing was to compensate for a decline in capital inflows, in order to “maintain a neutral, appropriate level of liquidity”—that is, to keep policy unchanged.

The central bank is right to be concerned about debt. Economy-wide debts have soared to 250% of GDP, up by 100 percentage points since 2008. Increases of that magnitude have presaged financial crises in other countries, so tighter policy would seem in order. Yet real interest rates have climbed to more than 8% for industrial companies, since the prices at which they sell their wares are actually declining. That, in turn, makes debts much harder to service than anticipated. Cutting interest rates while enforcing capital rules to prevent banks from issuing a gusher of new loans would be a better way to rein in debt.

The PBOC has talked instead of “fine tuning” monetary policy and making it more “targeted”.

The loan to China Development Bank appears to have been earmarked for public housing, which local governments have struggled to fund. To borrow from the “medium-term facility” banks were said to be obliged to reduce mortgage rates. In other words, having let air out of the property market, the PBOC now seems to be pumping it up again. “The problem is that there’s no clear framework for monetary policy. They are feeling their way through,” says Zhang Bin of the Chinese Academy of Social Sciences. “If you change targets, you should explain why.”

In the background are questions about the future of the long-serving Mr Zhou. He was due to step down in 2013, having reached the official retirement age of 65. When his term was extended, it was seen as an endorsement of his reformist agenda. But a few months ago, word spread in Beijing that he might soon be replaced. Some even suggested that he had pushed too hard to deregulate interest rates.

People familiar with the PBOC say that talk of Mr Zhou’s imminent retirement has since died down. Yet he will eventually depart. His legacy will be extremely positive overall: he has presided over an era of rapid growth, stable inflation and progress in financial reforms. But his final years in office are turning into a bit of a muddle.

0 comments:

Publicar un comentario