Buffering

New rules hemming in banks will make it easier to let them fail—with luck

Nov 15th 2014

WHEN big banks totter, taxpayers usually foot the bill. Given the chaos that would follow an outright failure—bank runs, frozen payment systems and so on—bail-outs have long been the least-bad option for governments. That might end under plans unveiled on November 10th by the Financial Stability Board (FSB), a group of international regulators, that should make it easier for banks to fail without recourse to the public purse.

Under the proposed new rule, the biggest banks will have to hold buffers, or “total loss-absorbing capacity” (TLAC), equivalent to 16-20% of their assets (the loans and investments they make)—vastly more than in the run-up to 2007. The bigger cushion comes in two main forms. First, banks must hold more equity (the money shareholders put into the business) relative to their assets. Second, bondholders, who put up much of the money banks go on to lend, will now be expected to shoulder losses after shareholders are wiped out.

The principle of “bailing in” creditors is welcome. Though in theory many of them should have been hit in 2007-09, in practice imposing losses on them proved legally difficult and so seemed foolhardy to attempt in the midst of a crisis. Now, bonds are counted towards TLAC only if they explicitly bear losses when things go wrong. One such instrument, known as contingent-convertible bonds, or “cocos”, is counted as debt in good times but automatically turns into equity if capital ratios drop below a certain level.

The TLAC rule, which comes into force in 2019, will apply only to 27 “systemically important” global banks such as HSBC and Citigroup. Smaller lenders are exempted, as are bigger ones in emerging markets. But they are widely expected to face similar rules soon.

Mark Carney, the governor of the Bank of England who also chairs the FSB, has made clear TLAC is not designed to prevent individual banks going out of business. The aim is to limit the potential reverberations, making a bank failure more akin to that of an airline or a carmaker, say: painful, complicated, but ultimately not a threat to the wider economy.

That in turn should remove the implicit subsidy big banks have unfairly enjoyed. Because creditors have long assumed the banks were “too big to fail”, they also assumed they would be repaid even if things turned sour. The upshot was that big banks borrowed at rates that were in effect subsidised by taxpayers. Removing that subsidy will dent bank profits—and rightly so.

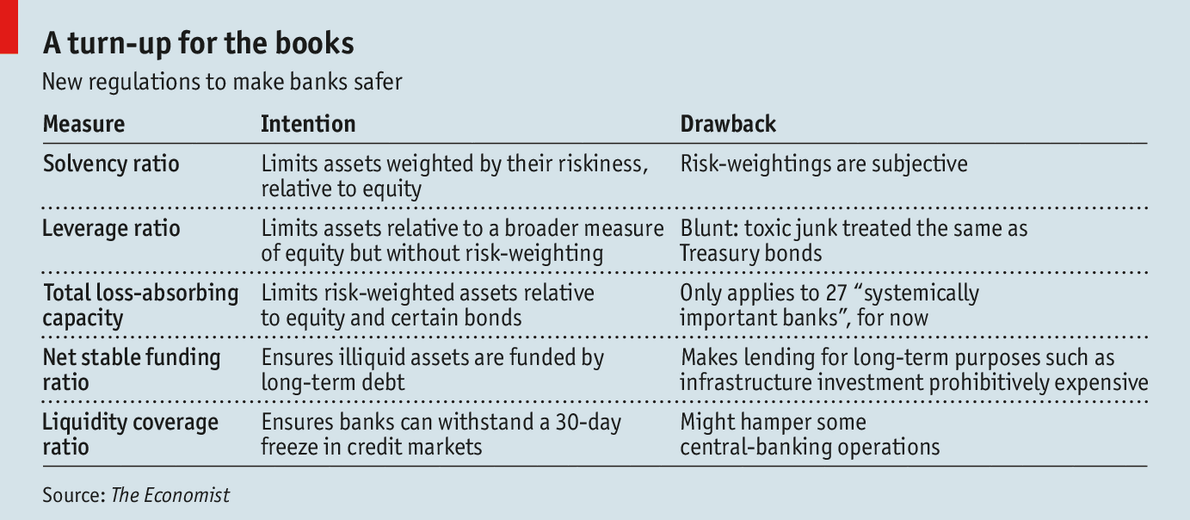

The TLAC proposals push in the same direction as four previous initiatives designed to make banks sturdier (see table). Bankers complain of a Rubik’s cube of rules: improve one ratio and you may find that another one deteriorates. They also fret that all this new rule-making is scaring away the investors whose money is needed to raise capital to the required level.

.

In theory, TLAC should be the last big global rule on capital. But regulators are still busy devising a system to ensure banks can be “resolved”, or wound down, should they go bust. Even if banks have lots of capital, they will remain too big to fail if they are too complicated to close. Much work remains to be done there: in August American officials rejected the “living wills” of 11 big banks, which were supposed to show how they could be shut down without causing undue disruption. Some will need to adopt new, simpler structures which in turn may require them to raise yet more equity.

Whether “too big to fail” is indeed over will only become clear during the next crisis. Imposing losses on investors such as pension funds or small-time punters is politically tricky. A recent bank failure in Portugal, Espírito Santo, resulted in a state-backed rescue which spared many bondholders. Hopefully next time will be different.

0 comments:

Publicar un comentario