Liquid diet

Recent market turbulence may be only a foretaste

Oct 25th 2014

.

SOLDIERING has been described as long periods of boredom punctuated by moments of sheer terror. Financial markets seem to be developing the same pattern.

The boredom stems from massive central-bank intervention in markets. As long as investors remain convinced that central banks are in control of events, and can adjust monetary policy to avoid recession and inflation, volatility will be low for most of the time. In these quiet periods, the dominant trend will be momentum—investors buying the assets that have most recently risen in price. By September, for example, investors were heavily exposed to peripheral European bonds (the debt of Greece and Spain, for example) and to cyclical stocks (those that perform best when the economy is doing well).

But when the trend changes, prices may move very sharply, as the terrified herd stampedes out of what can be illiquid markets. In the last four weeks, defensive stocks have outperformed cyclicals by one of the greatest margins in history, according to BlackRock, a fund-management group.

There was another good illustration of the herd mentality on October 15th, when the yield on ten-year Treasury bonds fell by a third of a percentage point in a matter of minutes. That was an extraordinarily abrupt drop for one of the most liquid markets in the world, especially since there was no news of sufficient importance to justify it.

The likeliest explanation is that investors, specifically hedge funds that had been speculating with borrowed money, had been caught by surprise by bond-market strength, and were desperately trying to cut their losses. Many of those investors may have previously taken the view that the American economy was recovering, that the Federal Reserve’s purchases of government bonds were ceasing, and thus that the only way for Treasury bond prices to go was down (making yields go up). They had duly bet on falling prices; when the trade went wrong, such investors had to reverse their bets rapidly.

Some offer a similar explanation for the sharp sell-off in the stockmarket. Hedge funds have suffered big losses in recent weeks—from the collapse of the AbbVie/Shire merger (which caused the latter’s share price to plunge), for example. That may have caused some of them to trim their holdings of riskier assets; shares tend to be more liquid than corporate bonds and were thus the easiest things to sell.

In other words, illiquidity in one market can cause problems for others. Something similar happened in August 2007, when hedge funds that were suffering losses on subprime-mortgage securities raised cash by selling equities.

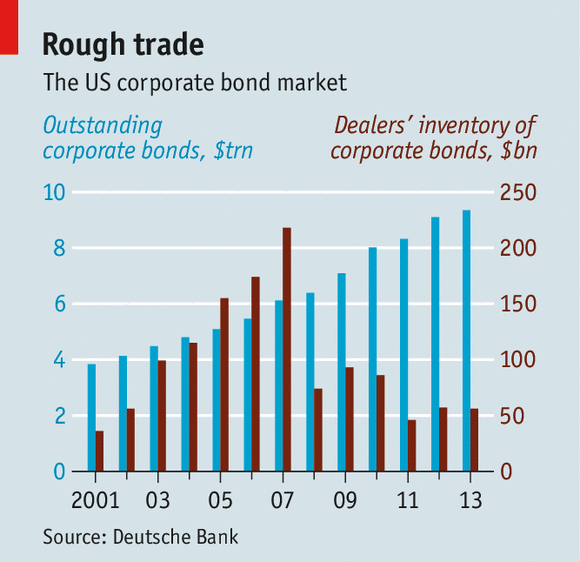

The obvious source of illiquidity-linked weakness is the corporate-bond market. Due to new regulatory restrictions and capital rules that make bond-trading less profitable, banks have cut back their inventories to the level of 2002, even though the value of bonds outstanding has doubled since then (see chart).

That is a problem when trading surges, as it did between October 10th and 16th, when volumes rose by 67%. “Credit is not a continuously priced market,” says Richard Ryan of M&G Investments, a fund manager. “When a bond price falls from 100 to 90, it won’t do so smoothly, but in big drops.”

The riskiest part of the bond market—junk, or high-yield, bonds—was already falling in price before mid-October. At the end of June, 96% of such bonds were trading above their issue price; by October 21st, only 77% were. That is not because corporate finances have deteriorated notably in the interim.

At the end of September, the default rate on high-yield bonds was just 2.1%, according to Moody’s, a rating agency, compared with an historical average of 4.7%. Nor does the slight deterioration in the economic outlook seem like adequate justification for the shift. Investors were simply taking profits.

So the recent market turbulence may only be a foretaste of what will happen if the world economy deteriorates more significantly, or if central banks decide to tighten monetary policy quickly. Of course, that thought may make central banks even more reluctant to push up interest rates than they are already. Financial markets may thus calm down again in the short term.

But the illiquidity problem will still be there when the next crisis occurs. In a sense, it is a problem caused by regulators; they wanted banks to be less exposed to the vicissitudes of markets. But you cannot make risk disappear altogether; you can only shift it to another place.

Get ready for more moments of sheer market terror.

0 comments:

Publicar un comentario