Oct. 22, 2014 11:27 AM ET

Summary

- The US could suffer from a low-growth, disinflationary future, similar to Japan after the collapse of the Japanese asset bubble.

- Policies of the Federal Reserve, such as QE, have increased the likelihood of disinflation.

- QE incentivizes short-term investment at the expense of long-term investment.

- Interest rate suppression results in a cycle of subdued returns, lower investment, and lower growth.

- Fed policies that have suppressed interest rates will increase likelihood of future issues with pension funds, resulting in austerity (higher taxes and / or lower benefits).

The United States is in danger of falling into a disinflationary, low-growth trap. It's the same perpetual trap that Japan fell into by the mid 1990s. And the policies of US Federal Reserve Bank are the primary culprit.

In 2008, the Federal Reserve launched its first quantitative easing program in the wake of the US financial crisis. The program initially focused on mortgage-backed securities, but shifted to US treasury bonds by March 2009. QE might have been thought of as an "emergency measure" at the time, but here we are nearly six years later, and the Fed is just now winding down the program. I'm not 100% convinced this is the end, either, as the Fed has gone down this path before in late 2009 and mid 2011, only to restart the program again.

QE's supporters have argued the program is necessary to stimulate a weak economy. QE's fiercest detractors have often argued that the size and scope of QE would result in massive and uncontrollable inflation.

My position differs from both of these common views. Rather than generating inflation, I view QE as disinflationary. Or to be more precise, QE has a near-term inflationary impact on asset prices, but over the long term, it has a disinflationary impact due to its reversionary nature, incentives favoring resource misallocation, and tendency to knock down long-term returns on investment.

Recall Newton's Third Law of Motion:

"When one body exerts a force on a second body, the second body simultaneously exerts a force equal in magnitude and opposite in direction on the first body."We may not be talking about physics, but the principle holds true in economics, as well.

When the Federal Reserve knocks down interest rates, it benefits borrowers, such as large corporations, banks, and real estate investment trusts ["REITs"]. Yet, there is always an "equal and opposite reaction." On the opposite side of the equation are savers, such as pension funds, retirees, endowments, mutual funds, the Social Security Trust Fund, etc.

QE's supporters have attempted to argue that the program "expands the pie" by creating more economic growth, but there's no evidence to support this thesis. What's more likely is that the program sacrifices long-term growth in the name of short-term growth. Moreover, there is a redistributionary aspect, with the borrowers increasing their profits, while the lenders reduce theirs. This is especially true given the zero-bound rate environment, where QE results in lower interest rate spreads.

The impact on savers may not be immediately apparent, for reasons I'll get into later. However, my basic thesis is that by knocking down interest rates, QE reduces the long-term rate of return, disincentivizing future investment. In essence, it promotes short-term investment (with subpar returns), at the expense of long-term growth.

Allocation and Misallocation

To understand why QE creates disinflation, we must first understand the concept of "malinvestment," or that is, the misallocation of resources. QE's main objective is to create economic growth by increasing lending. In order to do this, it attempts to lower costs for borrowers by knocking down the rate of return on alternatives to loans (e.g. treasury bonds).

This is an allocation preference that favors debt-driven growth. However, businesses and individuals that take on debt tend to have certain characteristics.

For a lender, the ideal loan is one where [a] there is greater certainty in cash flows, [b] there is a "creditworthy" borrower with a long-term track record, and [c] there is an asset to seize in case of default. In short, the ideal borrower is a large, mature company with stable cash flows that owns lots of real estate, machinery, or heavy assets with tangible value. The opposite of that would be a young start-up company, with inexperienced leadership, many intangible assets, and lots of uncertainty.

Hence, by favoring debt-driven growth, QE benefits certain assets over others. REITs and restaurants, for instance, benefit more directly from QE than say a biopharmaceutical R&D firm that relies almost exclusively on intangible know-how. That said, QE's tendency to knock down returns on one class of assets will eventually make other classes of investments more attractive, as well. For this reason, it's not a stretch to argue that while QE may have initially benefited hard assets more, the current venture capital boom may also be partly fueled by QE.

Yet, the general trend is the same. QE drives up asset prices, which then reduces the overall rate of return over time. This creates higher risk and makes the economy more vulnerable. While the US housing bubble was fueled more by conventional monetary policy, it was very similar in nature.

Rising Prices, Lower Returns

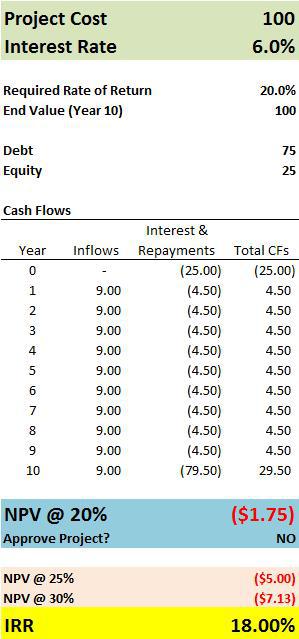

Let's model out a hypothetical scenario to illustrate the basic concept. This hypothetical asset costs $100 million to build, produces $9 million in annual cash flows in perpetuity, and will sell for exactly the same price in 10 years (for simplicity's sake). Our firm has a required rate of return of 20% and the current interest rate is 6%. We'll assume that assets of this variety are normally funded by 75% debt and 25% equity.

With a 6% interest rate and 75% debt financing, our asset will have a slightly negative NPV of $1.75 million. The IRR is around 18%, a bit below our 20% hurdle rate. As a result, we'll choose not the build the asset under these parameters.

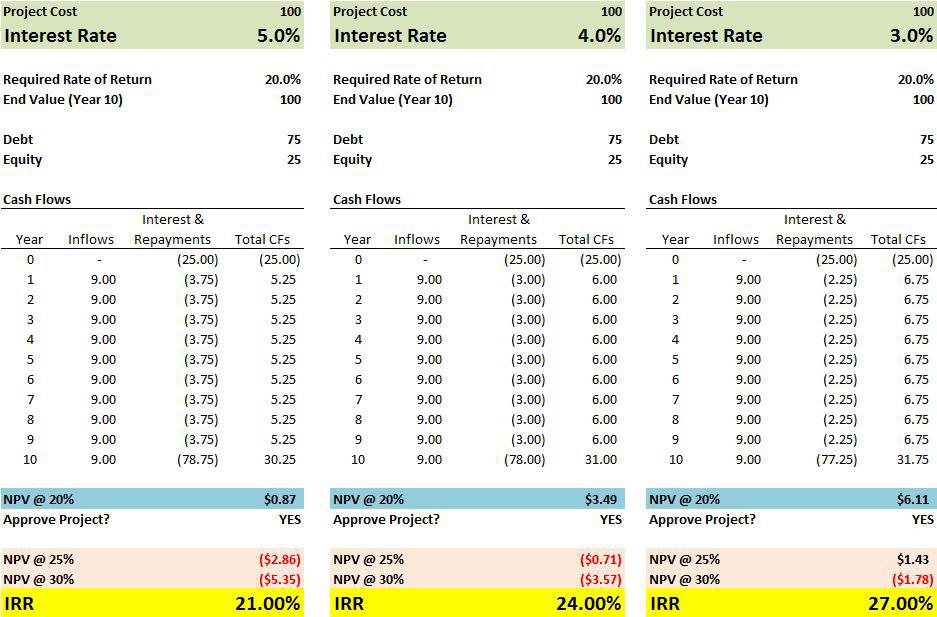

Now, let's assume the Federal Reserve conducts a series of quantitative easing measures that knock down market interest rates, first to 5%, then to 4%, and finally to 3%. With a lower 5% interest rate, the project now has an IRR of 21%, and therefore meets the 20% hurdle rate requirement. Thus, QE changed our decision to build. We can also see the progression as the rate continues to fall. With a 4% interest rate, the IRR increases to 24% and with a 3% interest rate, the IRR jumps all the way to 27%, with an NPV of $6.1 million. Suddenly, an investment that initially looked subpar looks spectacular.

(click to enlarge)

Is this ideal for the overall economy, though? As returns increase on this asset class, more investors move in and push the returns right back down.

Supply and Demand

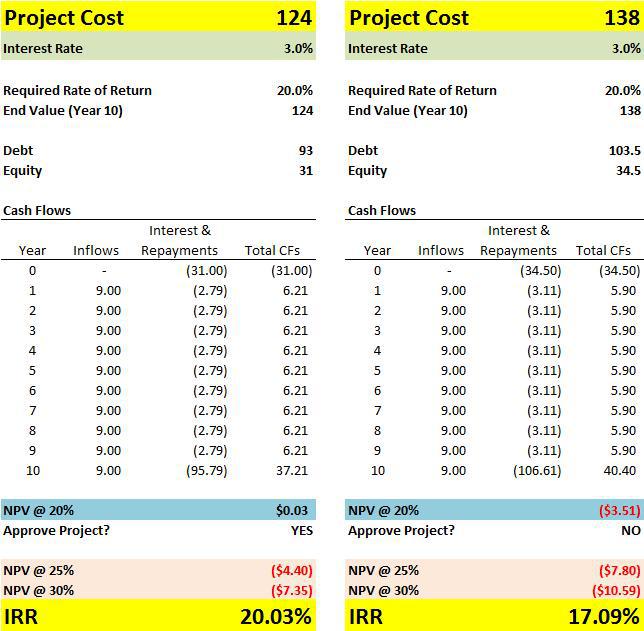

Now that we can earn a 27% IRR (well above the 20% target), a lot more investors want a share of the pie. These investors flood in and knock the IRR back down. This is achieved by bidding up the prices on the underlying assets.

How far will the IRR fall? It should fall back to at least 20% (our original required rate of return), but in reality, it will probably fall even further. Since the Fed has knocked down all interest rates, that means investors will eventually have fewer avenues to make a 20% return, and they'll begin to accept lower returns. Instead of 20%, they might be willing to take 17% (a conservative guess), or maybe even 15% or 12%, as the spread between the safest and riskiest investments begins to shrink.

In our example, in order to knock the IRR back down to 20%, the price of the underlying asset would need to rise 24% to $124 million. If we get more aggressive and knock the IRR down to 17%, the price must rise to $138 million. If we knock the IRR down to 12%, the price should surge 70% to $170 million. Yet, we should note that in all of these examples, the cash flows remained exactly the same. The only difference is that it costs much more to obtain the stream of cash flows.

(click to enlarge)

My examples may even be understating the impact. As interest rates go down and asset prices go up, banks are more likely to allow higher leverage ratios, further jacking up IRRs, which then leads to even higher prices.

This is how bubbles are created!

There are two possible outcomes. Either the market prices fall to push returns back up (i.e. a market correction) or returns continue to stay subdued. The latter outcome is of particular interest, as the Federal Reserve's policies indicate an extreme aversion to a market correction. However, I want to show why "return suppression" is an even bigger problem.

Equal and Opposite Reactions: The Savings Dilemma

Let's focus on the other side of the equation: the savers. In spite of generating lower long-term returns, QE initially looked good for savers since it created a flurry of capital gains from asset price increases.

This created the illusion of growth. However, over the long term, the logical outcome is subdued returns, which worsens the condition of savers. In application, QE does not look that different from a company that invests in a low-return project to boost short-term profitability. The company's earnings surge initially, but due to lack of prudent long-term investment, there's stagnation beyond that.

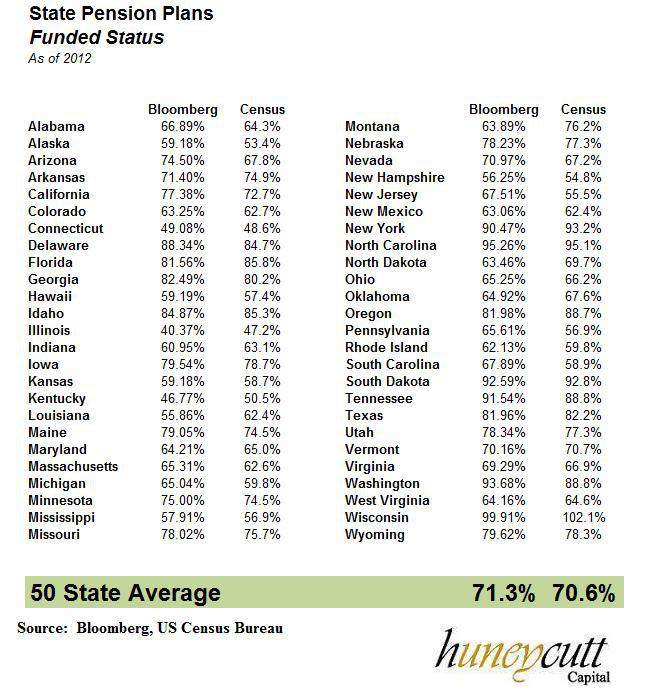

As far as savers go, the state public pension funds are worth examining in particular. This chart below shows the funded status of state public employee pension funds at the end of FY 2012.

Many of these pensions are severely underfunded, in spite of the great stock market environment of the past several years. For instance, Kentucky's funded level was only 46.8% and Illinois was only at 40.4% as of the end of 2012.

(click to enlarge)

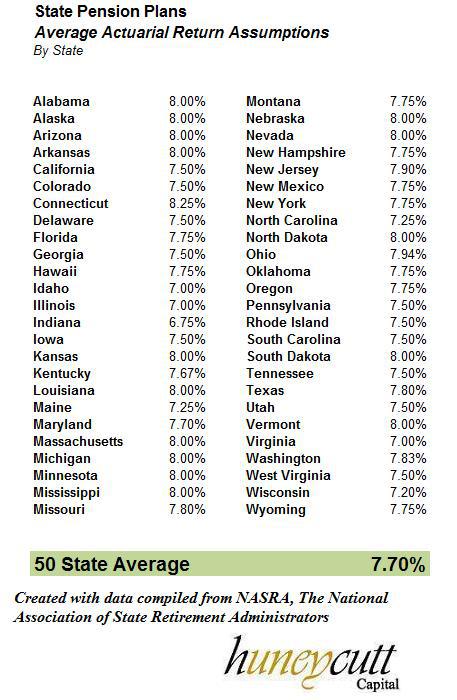

Next, we should take a look at the actuarial assumptions of these pension funds. More often than not, public employee unions have negotiated unrealistic assumptions with friendly politicians. The US average is around 7.7%, with several states coming in at 8%. These returns will become increasingly unrealistic the longer the Federal Reserve continues to suppress interest rates.

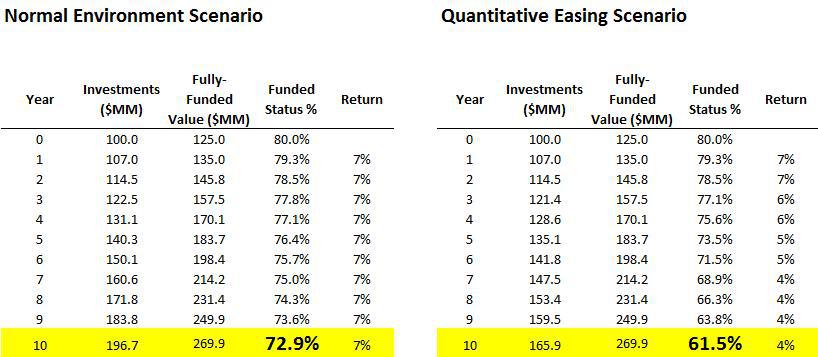

So now let's combine this information and get a sense of how QE may be impacting savers. Let's examine a hypothetical state pension fund that is 80% funded with an 8% actuarial return assumption. Let's assume that even during a normal environment, 7% is much more realistic than 8%. The fund has two options: increase risk to try to get to 8% or accept 7%. In this example, the fund will opt for the safe option. (Though, we should note that many funds get themselves into trouble by opting for the "higher risk" option.)

The fund will earn 7% for the first two years in our scenario. After that, a central bank will enact quantitative easing that knocks down interest rates. For Years 3 - 4, the fund will earn 6% maintaining the same level of risk. In Years 5-6, that falls to 5%, and for Years 7 - 10, the returns falls to 4%.

Now, let's model that against a "normal scenario" where the fund simply earns 7% the entire time.

The results can be seen in the chart below. At the end of the 10-year period, the "normal environment" fund ends up with $196.7 million in investments versus $165.9 million for the QE scenario, that's a difference of about $30 million. The "normal environment" fund is 72.9% funded at the end of ten years, and the QE scenario fund is only 61.5% funded.

(click to enlarge)

This is a pretty big difference over a 10-year time frame and this exact situation is going on across America right now. Of course, the actual results will be much lumpier than this, and may involve a stock market bubble and subsequent crash at some point.

It's not merely the public employee pension funds suffering. All savers will see subdued long-term returns as a result of QE. However, the state pension funds showcase what's happening on a grand scale. As these pension funds become increasingly underfunded, state governments will be forced to decide whether to cut benefits, raise taxes, or use a combination of the two policies. Tax increases and benefit cuts are both disinflationary, since they reduce private investment and consumer spending.

The overall logic goes like this: QE boosts short-term asset investment and higher prices, but this leads to subdued investment returns over the long term. These subdued returns result in less spending and investment in the future, which reduces future economic growth. Weaker economic growth results in weaker demand for loans, which is disinflationary.

International Concerns

It's worth noting that the policies of the US central bank are only one piece of the puzzle. Even if US policies promote low growth and disinflation, the rest of the world can significantly alter that equation. For instance, if Europe sees high growth, that will likely result in more global trade, which will be good for US growth.

Unfortunately, given the current state of the world, this scenario seems unlikely. The Eurozone looks even more dysfunctional than the US right now. Meanwhile, China continues to show more signs of weakness, which could further drag down global growth.

There are some bright spots around the world, such as East Africa, but it's difficult to imagine that this would be enough to offset the massive issues in Europe, the US, and China. For this reason, while there are some possible external factors that could drive greater US growth, I'm not terribly optimistic about them in the near-term future (i.e. the next 3-5 years). I view the "international environment" to be more likely to promote disinflation in the US.

How the Status Quo Could Change

Certainly, there's a possibility that shifts in policies could change (or exacerbate) the current disinflationary track. Let's focus on a few areas: Fed policy, taxes and spending, and regulation.

Fed policy is the simplest to deal with. While I've argued that the Federal Reserve has suppressed interest rates for a long time, the problem is that they have created a Catch-22. If the Feds raise interest rates, a significant market correction becomes much more likely. This may be beneficial long-term, since it will force returns to move back upwards, but it would also likely create a recession and invoke much short-term pain. Conversely, if the Feds continue down the current track, low returns will continue to harm pensions, resulting in higher taxes, lower spending, and subdued private investment. All of this is to say, I'm not sure that the Fed can "re-engineer" the US economy away from disinflation at this point. They are stuck in a mess of their own creation.

The greater hope for growth comes in the government policy sphere. On the regulatory front, Dodd-Frank reforms could be beneficial to long-term growth. While QE generally incentivizes lending, Dodd-Frank has created a semi-exception to the rule in residential housing. Why is this bad? Because it's another example of policy skewing natural economic decisions. Economically we are saying corporate lending is good, but mortgage lending is bad. This has resulted in a booming corporate environment, but a stagnant residential lending market. For this reason, a reversal or significant reform to Dodd-Frank could help unlock economic value and create greater long-term growth. It unfortunately will not stop the Fed's problematic policies, however, so no guarantees that it wouldn't also create another housing bubble.

The other obvious area that could change the status quo is taxes and spending. This can go many ways. We could see pro-growth reforms, such as a lower corporate tax, and a streamlined income tax code. These reforms would likely stimulate long-term growth. We could also see larger budget deficits, which create inflation. I won't go into details on this, except to say that we've seen declining budget deficits over the past few years due to a few trends:

(1) The stimulus act of 2009 created a temporary surge in spending but has since been tapered,

(2) Small Federal spending cuts (e.g. the sequester),

(3) Higher Federal taxes on payroll, income, capital gains, and healthcare,

(4) Cyclical factors have resulted in increased profitability, therefore increasing tax revenues

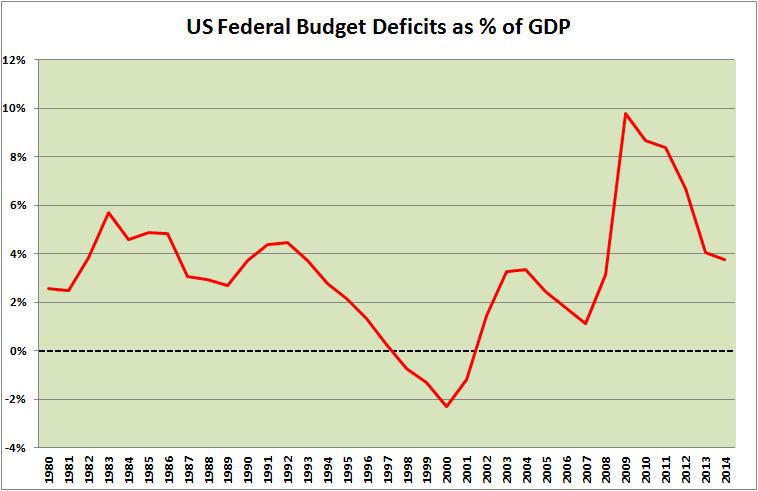

These factors have combined to knock the US Federal budget deficit from 10% of GDP in 2009 to 3.5% of GDP in 2014. A reversal of this could fuel more significant inflation. Conversely, a continued trend towards a balanced budget would be disinflationary, unless accompanied by pro-growth reforms. I mention this neither to say it's good nor bad, merely to say it is.

(click to enlarge)

Overall, I think it's unlikely that the Federal government changes its current course. We probably won't see any major shifts in tax or regulatory policy over the next few years. The Federal Reserve is a little less predictable, but given the current ideology there, I suspect that we will continue down the current track of ZIRP and monetary "stimulus" any time there's the slightest hint that the economy is seeing lower growth. In sum, the status quo is likely to continue for at least 2-3 more years.

Investment Takeaways

While this article may seem to present a lot of gloomy information, I would say don't lose hope.

The key is to make rational investment decisions. Many investors have done quite well in Japan in spite of the poor investment environment of the past two decades. Even if the US is headed for perpetual low growth, there will still be many good investments out there. Patience is required, however.

My biggest point of advice is to never lose sight of risk and reward. With a surging stock market, it's easy to convince one's self that "all is rosy," rather than realizing that prices are being driven by factors other than business fundamentals. The best investments have low downside risk and good upside reward potential. Higher prices imply higher risk. Good investments have existed in every market environment, including the tech bubble of 2000, and even the 2007 market. However, they are much more difficult to find in those types of inflated markets.

Keep away from high-flying stocks with insane multiples. This includes the Zillows (NASDAQ:Z), Teslas (NASDAQ:TSLA), and Netflixes (NASDAQ:NFLX) of the world. Even if these are good / great companies, the valuations are simply insane, and this has become common with a lot of tech stocks. This may be indirectly related to QE.

Keep a little extra cash on the side. Don't go overboard and hold 100% cash, but holding 10%, 20%, or 30% cash in your portfolio is completely reasonable right now given the macro risks. That way, if we get a significant correction, you'll have a good deal of extra cash to deploy to find stocks at more attractive valuations.

While it's possible that the Federal Reserve and the Federal government could reverse course, I do not envision it happening soon. For this reason, I see it as more likely that the disinflationary environment continues, with interest rates slowly falling, and the Dollar gaining strength. Be both cautious and opportunistic. Look for attractive investment ideas, but have a mindset of focusing more on capital preservation.

0 comments:

Publicar un comentario