The economy

How long will the expansion last?

Weighing the evidence

Aug 16th 2014

WASHINGTON, DC

.

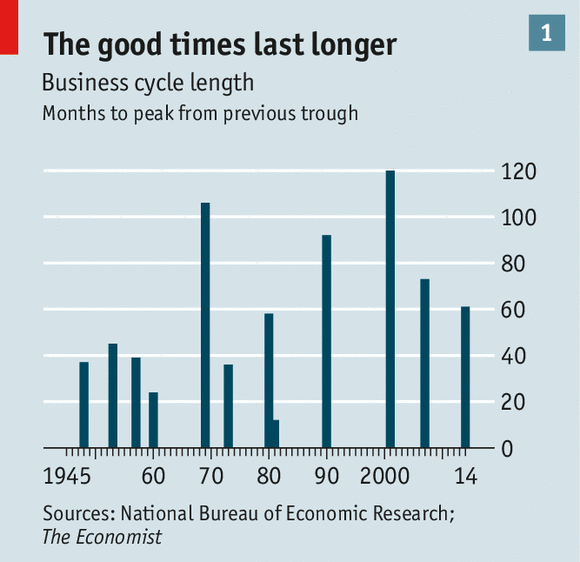

NEWS that America’s economy grew at a brisk annualised rate of 4% in the second quarter was greeted with relief. After a puzzling first-quarter contraction, growth has returned, though the recovery remains the weakest since the second world war. As of June, the expansion is now five years old, longer than the post-war average of 58 months (see chart 1).

The next recession could in theory be around the corner. But unlike people, business expansions don’t die of old age: they are killed by an unpredictable shock, says Bob Hall, an economist at Stanford University and chairman of the academic panel that dates American business cycles: “The next recession will come out of the blue, just like all of its predecessors.”

Recessions have become rarer in recent decades. The three expansions preceding the 2008 crisis lasted on average for 95 months. For that, economists credit structural factors such as companies’ better control of stocks, and modest inflation. The latter is especially important because as the late Rudi Dornbusch, an economist, once said, post-war expansions didn’t die in their beds; they were murdered by the Federal Reserve. The economy would run out of spare capacity, profits deteriorated, prices and wages rose and the Fed hiked interest rates, precipitating a recession.

If that pattern holds, the current expansion should have plenty of life left in it. Inflation is actually lower than the Fed’s target of 2%. The huge hit sustained during the crisis has a positive side: it has given the economy plenty of running room. JPMorgan reckons that adding a percentage point to the output gap at the start of an expansion adds two quarters to its lifespan. (The output gap is the difference between actual output and the maximum an economy can produce without sparking inflation.)

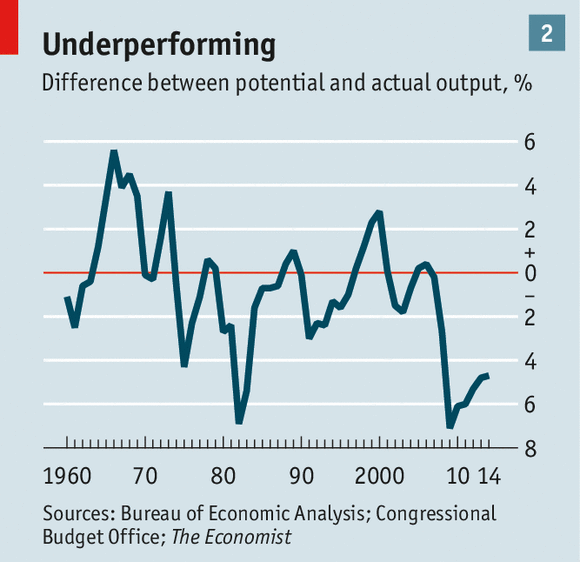

This suggests the current expansion has at least two more years to run; the economy is still operating some 5% below its potential (see chart 2). Better yet, the previous three expansions have ended around three years after unemployment fell to its “natural” rate, likely between 5% and 5.5%. By that yardstick, JPMorgan reckons the expansion could last until 2018, which would make it one of the longest on record.

But that may understate the actual risk of recession, for two reasons. One is that the output gap may be smaller than thought. Lewis Alexander of Nomura Securities, a bank, says labour markets are behaving as if the gap has almost disappeared. In June, the proportion of jobs that went unfilled jumped to 3.3%, matching the high of the previous expansion.

Second, interest rates have been stuck at zero since the recovery began because of sluggish growth and low inflation. Even if the Fed starts to tighten next year, as expected, rates will spend most of this expansion closer to zero than at any time since the 1930s. That leaves the Fed precious little firepower to respond to another shock.

Thus, previous cycles may be a poor guide to how long the current one lasts. Olivier Blanchard of the IMF thinks the economy now fluctuates between “normal” periods when it behaves as it has during past cycles, and “abnormal” periods when it meets the constraint of zero interest rates and weakens suddenly. “Before the crisis, we assumed we would stay away from those” constraints, he says. “Now we know that, once in a while, we shall get into that region and we have to be ready for it.”

NEWS that America’s economy grew at a brisk annualised rate of 4% in the second quarter was greeted with relief. After a puzzling first-quarter contraction, growth has returned, though the recovery remains the weakest since the second world war. As of June, the expansion is now five years old, longer than the post-war average of 58 months (see chart 1).

The next recession could in theory be around the corner. But unlike people, business expansions don’t die of old age: they are killed by an unpredictable shock, says Bob Hall, an economist at Stanford University and chairman of the academic panel that dates American business cycles: “The next recession will come out of the blue, just like all of its predecessors.”

Recessions have become rarer in recent decades. The three expansions preceding the 2008 crisis lasted on average for 95 months. For that, economists credit structural factors such as companies’ better control of stocks, and modest inflation. The latter is especially important because as the late Rudi Dornbusch, an economist, once said, post-war expansions didn’t die in their beds; they were murdered by the Federal Reserve. The economy would run out of spare capacity, profits deteriorated, prices and wages rose and the Fed hiked interest rates, precipitating a recession.

If that pattern holds, the current expansion should have plenty of life left in it. Inflation is actually lower than the Fed’s target of 2%. The huge hit sustained during the crisis has a positive side: it has given the economy plenty of running room. JPMorgan reckons that adding a percentage point to the output gap at the start of an expansion adds two quarters to its lifespan. (The output gap is the difference between actual output and the maximum an economy can produce without sparking inflation.)

This suggests the current expansion has at least two more years to run; the economy is still operating some 5% below its potential (see chart 2). Better yet, the previous three expansions have ended around three years after unemployment fell to its “natural” rate, likely between 5% and 5.5%. By that yardstick, JPMorgan reckons the expansion could last until 2018, which would make it one of the longest on record.

But that may understate the actual risk of recession, for two reasons. One is that the output gap may be smaller than thought. Lewis Alexander of Nomura Securities, a bank, says labour markets are behaving as if the gap has almost disappeared. In June, the proportion of jobs that went unfilled jumped to 3.3%, matching the high of the previous expansion.

Second, interest rates have been stuck at zero since the recovery began because of sluggish growth and low inflation. Even if the Fed starts to tighten next year, as expected, rates will spend most of this expansion closer to zero than at any time since the 1930s. That leaves the Fed precious little firepower to respond to another shock.

Thus, previous cycles may be a poor guide to how long the current one lasts. Olivier Blanchard of the IMF thinks the economy now fluctuates between “normal” periods when it behaves as it has during past cycles, and “abnormal” periods when it meets the constraint of zero interest rates and weakens suddenly. “Before the crisis, we assumed we would stay away from those” constraints, he says. “Now we know that, once in a while, we shall get into that region and we have to be ready for it.”

0 comments:

Publicar un comentario