Financing Europe’s small firms

Don’t bank on the banks

Aug 16th 2014

PARIS

.

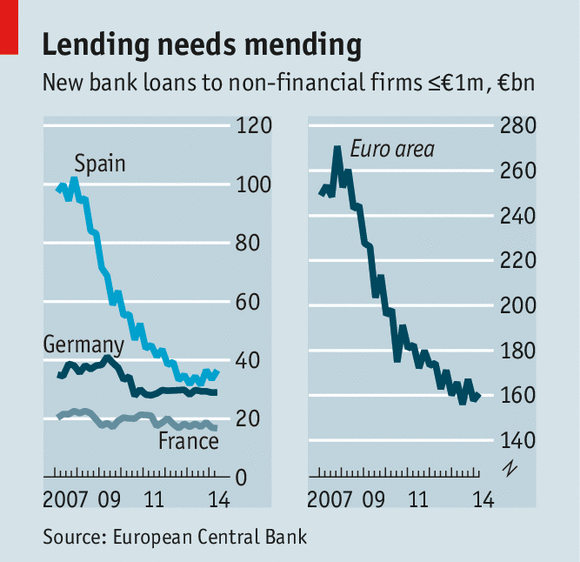

OF THE 54 firms to have listed on Borsa Italiana’s secondary market for smaller firms, 18 have done so this year. The most unusual was Blue Note Milano, a jazz club, pictured above, which last month sold 40% of its shares for €1.4m ($1.9m). In Europe, small and medium-sized enterprises (SMEs) usually ask banks, not markets, for money. But new bank lending to small firms in the euro area plummeted 35% between 2008 and 2013 to €649 billion (see chart). It fell sharply in Britain too.

This matters, and not only to small businesses’ owners and employees. Small firms are the lifeblood of Europe’s economy. Around 99% of all non-financial companies in the European Union are SMEs, that is, firms with fewer than 250 employees and less than €50m in annual turnover.

They account for 58% of value added and 66% of jobs. They are more reliant than big firms on domestic demand and bank lending, and have suffered acutely as both have shrivelled during the euro crisis. No wonder the euro zone’s economy is stagnant. As Nir Klein of the IMF points out in a recent paper, there is a link between the trouble some European countries have had escaping from recession and the prevalence of SMEs in their economies.

Signs are that bank lending may at last be stabilising. In June the volume of new euro-area bank loans of €1m or less (the best proxy for lending to small firms) was flat compared with the same month a year earlier, and it ticked up in Spain, as it had done earlier in Britain. In the three months to June, lending standards eased for all corporate borrowers, including small firms, for the first time since 2007, says the European Central Bank (ECB). Surveys suggest that SME owners are worrying a bit less about access to finance.

But differences are stark. Bigger SMEs have fewer problems than smaller ones. Firms that are part of a supply chain borrow more easily than those that are not.

Germany’s SMEs have been doing quite well, although its economy is now faltering. In France interest rates for good-sized SMEs are low and there is plenty of public-sector support. Small firms in peripheral countries such as Spain remain unhappy about the cost of loans which, some admit, may be a little easier to get these days.

If Europe’s economy ever picks up speed, more SMEs will generate their own resources. But they will also want more external finance to grow, not just survive. Europe’s banks, laden with bad debts and forced by new prudential rules to hold more capital against corporate loans, will remain leery of fiddly, risky loans to SMEs.

Small firms’ woes have not escaped detection. National governments and the EU have come up with one initiative after another to help them. Most seek to lure banks to lend more, through guarantees or cheap funding. That is helpful, but may not prompt banks to lend as much as expected. Many banks say it is not cheap funding they lack but the capital to back the loans they make with it. Undeterred, the ECB plans to make another €400 billion available to them from September.

Money is also being poured directly into SMEs by public-sector banks and funds. SMEs are nudged towards raising money from non-bank sources through tax breaks and help with listing costs. To make it easier for potential backers, governments are beginning to regulate crowdfunding platforms and central banks to ponder the Banque de France’s credit register, which lets lenders assess the creditworthiness of thousands of firms great and small. The ECB is building a cross-border databank for the same purpose.

On this newly fertile soil a thousand private-sector flowers are blooming. Stock exchanges are urging SMEs to issue equity and debt. There has also been a proliferation of new business-angel networks, venture capitalists, private-debt funds and crowdfunding platforms of increasing scale and variety. Small firms that can are tapping them.

Viadeo, an online professional network, listed in July in Paris, one of a bumper crop of SMEs welcomed this year by Euronext, the operator of five European stock exchanges. BlaBlaCar, a French firm that makes a popular car-sharing app, raised €100m in venture funding in July. The same month a group of small Italian water utilities pooled debt they had issued to create a security to be sold to big financial institutions. In Britain, some SMEs are offering “mini-bonds”—in effect, lumping together lots of small, unsecured loans from retail investors. At the humbler end of the spectrum, Ant Tomlinson borrowed enough through a crowdfunding platform to finish a new office for his British web-design firm. In Italy a maker of 3D printers went the same route.

The question is whether such alternatives—and there are many more—can ever achieve the scale to replace the share of conventional bank lending that may be gone for good. They constituted perhaps 10-15% of small firms’ external financing in 2013, reckons John Ott of Bain & Company, a consulting firm. For many, these are avenues to be encouraged but not relied on, and open mainly to bigger or higher-growth SMEs. The real task is finding ways to spur the bank lending that the smallest businesses prefer.

Insurance firms provide one option. They take in more than €1 trillion in premiums each year. Much of that is invested in government bonds, but insurers are attracted to the higher returns and greater diversification that SME lending offers. As with the banks, new rules will force them to hold more capital than before against corporate loans. But the biggest obstacle is the fiddly and expensive business of finding would-be borrowers and assessing their finances. Insurers would rather rely on banks’ expertise for this.

Some insurers are buying SME loans off banks or helping to finance them. Others would like to buy tradable securities backed by pools of loans issued by banks.

Spinning off a chunk of their assets in this way would let banks clear space on their balance-sheets for new lending. But securitisation is associated by regulators with the financial meltdown in 2008, even though the SME-backed version in Europe performed well. Under proposed new rules, banks or insurers that buy such securities must hold more capital against them than they would against other long-term loans. Unless the rules change, securitised SME loans may struggle to be both lucrative enough for insurers to covet and cheap enough for small firms to afford.

OF THE 54 firms to have listed on Borsa Italiana’s secondary market for smaller firms, 18 have done so this year. The most unusual was Blue Note Milano, a jazz club, pictured above, which last month sold 40% of its shares for €1.4m ($1.9m). In Europe, small and medium-sized enterprises (SMEs) usually ask banks, not markets, for money. But new bank lending to small firms in the euro area plummeted 35% between 2008 and 2013 to €649 billion (see chart). It fell sharply in Britain too.

This matters, and not only to small businesses’ owners and employees. Small firms are the lifeblood of Europe’s economy. Around 99% of all non-financial companies in the European Union are SMEs, that is, firms with fewer than 250 employees and less than €50m in annual turnover.

They account for 58% of value added and 66% of jobs. They are more reliant than big firms on domestic demand and bank lending, and have suffered acutely as both have shrivelled during the euro crisis. No wonder the euro zone’s economy is stagnant. As Nir Klein of the IMF points out in a recent paper, there is a link between the trouble some European countries have had escaping from recession and the prevalence of SMEs in their economies.

Signs are that bank lending may at last be stabilising. In June the volume of new euro-area bank loans of €1m or less (the best proxy for lending to small firms) was flat compared with the same month a year earlier, and it ticked up in Spain, as it had done earlier in Britain. In the three months to June, lending standards eased for all corporate borrowers, including small firms, for the first time since 2007, says the European Central Bank (ECB). Surveys suggest that SME owners are worrying a bit less about access to finance.

But differences are stark. Bigger SMEs have fewer problems than smaller ones. Firms that are part of a supply chain borrow more easily than those that are not.

Germany’s SMEs have been doing quite well, although its economy is now faltering. In France interest rates for good-sized SMEs are low and there is plenty of public-sector support. Small firms in peripheral countries such as Spain remain unhappy about the cost of loans which, some admit, may be a little easier to get these days.

If Europe’s economy ever picks up speed, more SMEs will generate their own resources. But they will also want more external finance to grow, not just survive. Europe’s banks, laden with bad debts and forced by new prudential rules to hold more capital against corporate loans, will remain leery of fiddly, risky loans to SMEs.

Small firms’ woes have not escaped detection. National governments and the EU have come up with one initiative after another to help them. Most seek to lure banks to lend more, through guarantees or cheap funding. That is helpful, but may not prompt banks to lend as much as expected. Many banks say it is not cheap funding they lack but the capital to back the loans they make with it. Undeterred, the ECB plans to make another €400 billion available to them from September.

Money is also being poured directly into SMEs by public-sector banks and funds. SMEs are nudged towards raising money from non-bank sources through tax breaks and help with listing costs. To make it easier for potential backers, governments are beginning to regulate crowdfunding platforms and central banks to ponder the Banque de France’s credit register, which lets lenders assess the creditworthiness of thousands of firms great and small. The ECB is building a cross-border databank for the same purpose.

On this newly fertile soil a thousand private-sector flowers are blooming. Stock exchanges are urging SMEs to issue equity and debt. There has also been a proliferation of new business-angel networks, venture capitalists, private-debt funds and crowdfunding platforms of increasing scale and variety. Small firms that can are tapping them.

Viadeo, an online professional network, listed in July in Paris, one of a bumper crop of SMEs welcomed this year by Euronext, the operator of five European stock exchanges. BlaBlaCar, a French firm that makes a popular car-sharing app, raised €100m in venture funding in July. The same month a group of small Italian water utilities pooled debt they had issued to create a security to be sold to big financial institutions. In Britain, some SMEs are offering “mini-bonds”—in effect, lumping together lots of small, unsecured loans from retail investors. At the humbler end of the spectrum, Ant Tomlinson borrowed enough through a crowdfunding platform to finish a new office for his British web-design firm. In Italy a maker of 3D printers went the same route.

The question is whether such alternatives—and there are many more—can ever achieve the scale to replace the share of conventional bank lending that may be gone for good. They constituted perhaps 10-15% of small firms’ external financing in 2013, reckons John Ott of Bain & Company, a consulting firm. For many, these are avenues to be encouraged but not relied on, and open mainly to bigger or higher-growth SMEs. The real task is finding ways to spur the bank lending that the smallest businesses prefer.

Insurance firms provide one option. They take in more than €1 trillion in premiums each year. Much of that is invested in government bonds, but insurers are attracted to the higher returns and greater diversification that SME lending offers. As with the banks, new rules will force them to hold more capital than before against corporate loans. But the biggest obstacle is the fiddly and expensive business of finding would-be borrowers and assessing their finances. Insurers would rather rely on banks’ expertise for this.

Some insurers are buying SME loans off banks or helping to finance them. Others would like to buy tradable securities backed by pools of loans issued by banks.

Spinning off a chunk of their assets in this way would let banks clear space on their balance-sheets for new lending. But securitisation is associated by regulators with the financial meltdown in 2008, even though the SME-backed version in Europe performed well. Under proposed new rules, banks or insurers that buy such securities must hold more capital against them than they would against other long-term loans. Unless the rules change, securitised SME loans may struggle to be both lucrative enough for insurers to covet and cheap enough for small firms to afford.

0 comments:

Publicar un comentario